PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062411

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062411

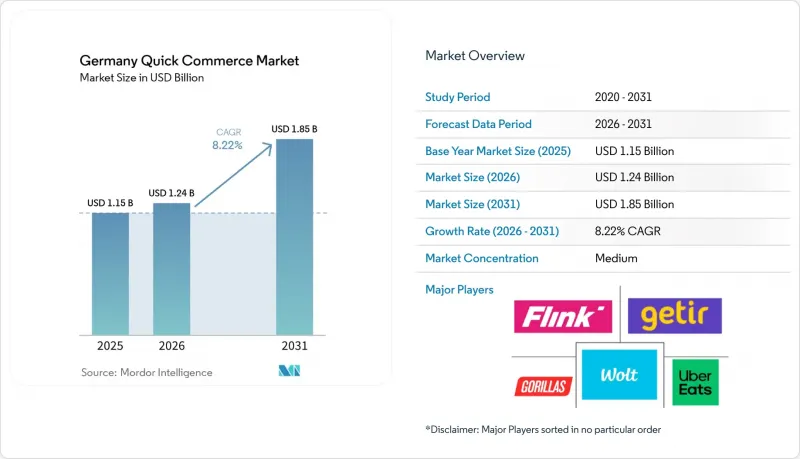

Germany Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany quick commerce market size is expected to increase from USD 1.15 billion in 2025 to USD 1.24 billion in 2026 and reach USD 1.85 billion by 2031, growing at a CAGR of 8.22% over 2026-2031.

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Pet Care, and Flowers and Gifts), Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, 31-60 Minutes, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Quick Commerce Market Trends and Insights

Rising Demand For Convenience Among Dual-Income Households

Dual-income households remain the most dependable demand base for the Germany quick commerce market. Germany's Federal Statistical Office reported that couples with children spent an average of EUR 658 (USD 703), per month on food, beverages, and tobacco in 2025 when both partners were in paid employment, which was materially above the national household average. That spending profile matters because these households are not using delivery only for occasional convenience, they are shifting recurring household tasks into paid services. The same pattern is stronger in larger urban households, where time pressure is higher and daily routines are more compressed. This produces more frequent orders, steadier basket formation, and better utilization of neighborhood fulfillment assets. As the Germany quick commerce market becomes more disciplined, operators with dense urban coverage are better placed to convert this repeat demand into more stable unit economics.

Growing Urban Millennial And Gen Z Population In Major Cities

Millennial and Gen Z consumers are reshaping the order mix in the Germany quick commerce market. The user base in these age groups is more comfortable with app-based grocery shopping and more willing to treat fast delivery as a routine purchase channel rather than an occasional service. Their demand is also broader than the early grocery-only model, because younger users increasingly add beauty, household, pet, and small electronics purchases to the same platform journey. That widens the revenue opportunity without requiring the same increase in delivery infrastructure. The importance of this shift is not only higher order frequency, but also better cross-category monetization from the same customer base. In practical terms, this makes younger urban customers central to category expansion and to the next stage of Germany quick commerce market growth.

High Last-Mile Logistics Costs Eroding Unit Economics

Last-mile delivery remains the most persistent operating challenge in the Germany quick commerce market. HHL Leipzig Graduate School of Management research cited by Handelsdaten showed average quick commerce delivery costs of EUR 6.80 (USD 7.96) per order against average revenues of EUR 5.18 (USD 6.06), leaving an operational loss of EUR 1.63 (USD 1.17) per drop before warehousing and marketing costs are added. The regulatory backdrop is also becoming more expensive, because the EU Platform Work Directive entered into force in December 2024 and Germany must transpose it into national law by December 2, 2026, which raises the risk of full payroll obligations for riders. Wolt's earlier shift to a hybrid labor model in Germany increased fixed labor costs by 17%, which illustrates how quickly delivery economics can tighten when labor rules change. The real constraint is not only wages, but also order density, because operators still need 500 to 1,000 daily orders per dark store to approach profitability. That threshold can be reached in central Berlin, but it is harder to sustain in Tier II and Tier III cities where demand is more dispersed.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Venture Capital And Corporate Funding For Quick Commerce

- Strategic Partnerships Between Quick Commerce Platforms And Supermarket Chains

- Intensifying Regulatory Scrutiny On Dark Stores In Residential Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and Staples held 52.61% share of the Germany quick commerce market size in 2025, which confirmed that daily household replenishment remained the main reason consumers used these services. The category supports repeat ordering and relatively predictable basket formation, which makes it the most manageable starting point for dark store assortment planning. Fresh Produce and Dairy remains the key adjacent category because operators need fresh baskets to deepen household reliance on the platform. Picnic's Oberhausen fulfillment center, opened in August 2025 with EUR 150 million (USD 160.5 million), in investment, uses 1,500 autonomous robots across 3 temperature zones from -18°C to +20°C and can process up to 33,000 orders per day, which showed that fresh grocery fulfillment at scale is operationally achievable. Electronics and Accessories is forecast to grow at the fastest 8.54% CAGR from 2026 to 2031, which points to a broader use case developing inside the Germany quick commerce industry.

Snacks and Beverages, Personal Care and OTC Pharma, and Home and Cleaning Supplies continue to sit in the middle of the mix because they fit short-notice replenishment needs and usually travel well through existing last-mile networks. Pet Care, Flowers and Gifts, and Other Product Categories remain smaller, but they matter because they raise basket value and improve order economics without requiring the same cold-chain complexity. Wolt's nationwide partnership with Fressnapf in 2026 showed how platforms are using specialist retail brands to widen the product mix and keep customers inside the same app environment. Across the Germany quick commerce industry, the category shift is less about abandoning grocery and more about layering higher-value discretionary purchases onto an already established convenience habit.

List of Companies Covered in this Report:

- Flink SE

- Getir Germany GmbH

- Rohlik Group GmbH / Knuspr

- Wolt Enterprises Deutschland GmbH

- Uber Eats Germany GmbH

- Amazon.com Inc.

- REWE Group

- Delivery Hero SE

- DoorDash Inc.

- Picknick GmbH

- Bringmeister GmbH

- Edeka Zentrale Stiftung & Co. KG

- Lidl Stiftung & Co. KG

- Aldi Einkauf SE & Co. oHG

- Kaufland Dienstleistung GmbH & Co. KG

- Flaschenpost SE

- Stuart Delivery GmbH

- Bolt Technology OU

- Freshflow GmbH

- Homeride

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Convenience Among Dual-Income Households

- 4.2.2 Growing Urban Millennial and Gen Z Population in Major Cities

- 4.2.3 Increasing Venture Capital and Corporate Funding for Quick Commerce

- 4.2.4 Strategic Partnerships Between Quick Commerce Platforms and Supermarket Chains

- 4.2.5 Municipal Subsidies for Electric Cargo Bikes That Reduce Delivery Costs

- 4.2.6 Adoption of AI-Driven Micro-Fulfillment Centers to Optimize Order Picking

- 4.3 Market Restraints

- 4.3.1 High Last-Mile Logistics Costs Eroding Unit Economics

- 4.3.2 Intensifying Regulatory Scrutiny on Dark Stores in Residential Areas

- 4.3.3 Rising Competition From Supermarket Click-and-Collect Models

- 4.3.4 Limited Cold-Chain Capacity for Fresh Produce in Micro Fulfillment Hubs

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Flink SE

- 6.4.2 Getir Germany GmbH

- 6.4.3 Rohlik Group GmbH / Knuspr

- 6.4.4 Wolt Enterprises Deutschland GmbH

- 6.4.5 Uber Eats Germany GmbH

- 6.4.6 Amazon.com Inc.

- 6.4.7 REWE Group

- 6.4.8 Delivery Hero SE

- 6.4.9 DoorDash Inc.

- 6.4.10 Picknick GmbH

- 6.4.11 Bringmeister GmbH

- 6.4.12 Edeka Zentrale Stiftung & Co. KG

- 6.4.13 Lidl Stiftung & Co. KG

- 6.4.14 Aldi Einkauf SE & Co. oHG

- 6.4.15 Kaufland Dienstleistung GmbH & Co. KG

- 6.4.16 Flaschenpost SE

- 6.4.17 Stuart Delivery GmbH

- 6.4.18 Bolt Technology OU

- 6.4.19 Freshflow GmbH

- 6.4.20 Homeride

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment