PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062400

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062400

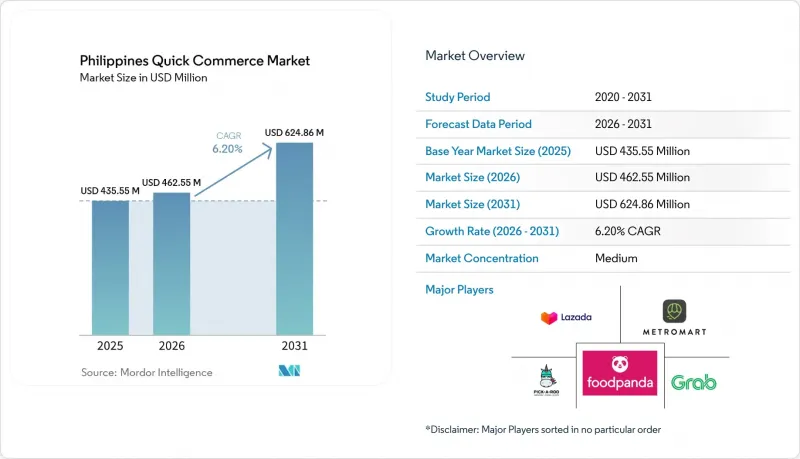

Philippines Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the philippines quick commerce market size was valued at USD 435.55 million in 2025 and USD 462.55 million in 2026, and is projected to reach USD 624.86 million by 2031, at a CAGR of 6.20% from 2026 to 2031.

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), and Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Quick Commerce Market Trends and Insights

Rapid Urbanization of Metro Manila and Cebu Boosting Demand

Metro Manila reached 14,001,751 residents in the 2024 census, reinforcing its position as the country's densest demand center for fast delivery services. The Manila urban agglomeration reached 24.7 million people in 2025, and the Philippine urban population crossed 55.8% of the national total, which keeps demand concentrated in corridors where fast fulfillment is easier to sustain. In the Philippines quick commerce market, this concentration improves dark-store economics because shorter catchment radii can serve more households with the same rider base. The same urban pattern also supports higher order frequency because apartment residents and professional households rely more heavily on convenience-led top-up purchases. Cebu adds a second strong urban node for the Philippines quick commerce market because leading operators already treat it as a core city for scale rather than a peripheral expansion market.

Growing Penetration of Digital Wallets and Cashless Payments

Digital payments accounted for 57.4% of total monthly retail transaction volume and 59.0% of retail transaction value in the Philippines in 2024, indicating the country moved beyond the government's target band. InstaPay and PESONet processed PHP 24.7 trillion (USD 431 billion) in 2025, up 42% from PHP 17.42 trillion (USD 306.5 billion) in 2024. QR Ph person-to-merchant transaction volume rose 1,315.9% year over year, indicating that QR-based checkout is now part of regular retail behavior rather than a niche channel. In the Philippines quick commerce market, this means payment adoption is no longer the main barrier in urban households, and order frequency has become a more important lever for gross merchandise value growth.GCash had 94 million registered users as of Q1 2025 and processed more than 18 million daily transactions, while e-wallets accounted for 39% of digital transactions in 2025, surpassing cards.

High Last-Mile Logistics Costs In Congested Cities

Philippine logistics costs consumed 27.5% of GDP in 2025, the highest ratio in ASEAN, and logistics-related expenses accounted for 27% of firms' sales revenue. Last-mile delivery already accounts for more than 50% of total shipping costs in the Asia Pacific, so congestion in Metro Manila makes that cost burden even harder to absorb for quick-delivery models. In the Philippines quick commerce market, this squeezes margins most heavily in the 11-30 Minutes tier because it is fast enough to promise convenience but not dense enough to fully neutralize urban traffic penalties. Local traffic rules and delivery window controls also increase riders' idle time, which increases per-order costs in dense city corridors. The Luzon Economic Corridor may improve wider logistics efficiency over time, but it is less likely to solve intra-city last-mile pressure in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Dark-Store Networks by Key Players

- Rising Disposable Income Among Gen Z and Millennials

- Limited Cold-Chain Infrastructure For Fresh Produce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and Staples held 53.48% of the Philippines quick commerce market share in 2025, making essential goods the main habit-forming category across delivery platforms. Filipino households still rely heavily on neighborhood retail for daily essentials, and this behavior has been moving onto digital platforms in metro corridors where convenience and repeat purchasing are strongest. In the Philippines quick commerce industry, this makes Grocery and Staples the core traffic driver because it supports frequent replenishment rather than occasional browsing. Fresh Produce and Dairy remained a high-intent segment, but operators still faced sourcing and handling pressure that reduced price flexibility against wet markets and traditional stores.

Pet Care is projected to grow at a 6.56% CAGR from 2026 to 2031, the fastest pace among product categories in the Philippines quick commerce market. Urban Gen Z and Millennial households are driving this rise because pet ownership is growing in dense residential areas where convenience-led purchasing is already strong. A December 2025 collaboration between Packworks and Ateneo de Manila University found that AI-driven demand forecasting lifted daily GMV by 46% and total sales by 17% across 300-plus sari-sari stores, with Pet Care among the categories most responsive to precision reordering. Home and Cleaning Supplies has also shown steady bundling with Grocery and Staples orders, which means operators that improve SKU-level forecasting can lift profitability even in categories that currently carry thinner margins.

List of Companies Covered in this Report:

- Grab Holdings Inc.

- Delivery Hero SE

- MetroMart Technologies Inc.

- Pick.A.Roo (Hatch Tech Solutions Inc.)

- GoCart (Robinsons Retail Holdings Inc.)

- Lazada Group

- Shopee Pte Ltd.

- SM Investments Corporation

- AllDay Marts Inc.

- Puregold Price Club Inc.

- SariSuki Fulfillment Inc.

- Alfamart Trading Philippines Inc.

- 7-Eleven Philippines

- MerryMart Consumer Corp.

- CloudEats Philippines Inc.

- WalterMart Community Mall

- JG Summit Olefins Corp.

- Dali Discount AG Philippines

- TikTok Shop Philippines

- UnionBank of the Philippines

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanization of Metro Manila and Cebu Boosting Demand

- 4.2.2 Growing Penetration of Digital Wallets and Cashless Payments

- 4.2.3 Expansion of Dark-Store Networks by Key Players

- 4.2.4 Rising Disposable Income Among Gen Z and Millennials

- 4.2.5 Introduction of AI-Powered Demand Forecasting for Micro-Fulfillment

- 4.2.6 Emergence of "Sari-Sari Store" Aggregator Partnerships

- 4.3 Market Restraints

- 4.3.1 High Last-Mile Logistics Costs in Congested Cities

- 4.3.2 Limited Cold-Chain Infrastructure for Fresh Produce

- 4.3.3 Stringent City-Level Traffic Regulations and Window Hours

- 4.3.4 Consumer Trust Issues Around Order Accuracy in Tier III Towns

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.7.1 Porter's Five Forces Analysis

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitute Services

- 4.7.6 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Grab Holdings Inc.

- 6.4.2 Delivery Hero SE

- 6.4.3 MetroMart Technologies Inc.

- 6.4.4 Pick.A.Roo (Hatch Tech Solutions Inc.)

- 6.4.5 GoCart (Robinsons Retail Holdings Inc.)

- 6.4.6 Lazada Group

- 6.4.7 Shopee Pte Ltd.

- 6.4.8 SM Investments Corporation

- 6.4.9 AllDay Marts Inc.

- 6.4.10 Puregold Price Club Inc.

- 6.4.11 SariSuki Fulfillment Inc.

- 6.4.12 Alfamart Trading Philippines Inc.

- 6.4.13 7-Eleven Philippines

- 6.4.14 MerryMart Consumer Corp.

- 6.4.15 CloudEats Philippines Inc.

- 6.4.16 WalterMart Community Mall

- 6.4.17 JG Summit Olefins Corp.

- 6.4.18 Dali Discount AG Philippines

- 6.4.19 TikTok Shop Philippines

- 6.4.20 UnionBank of the Philippines

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment