PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062406

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062406

Singapore Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

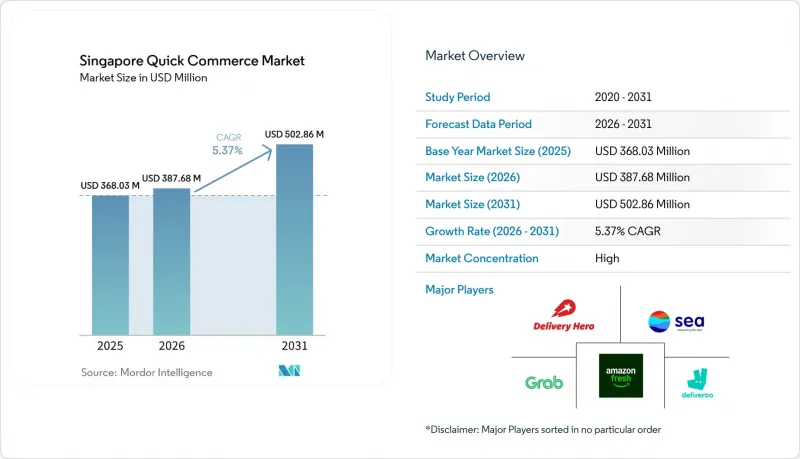

According to Mordor Intelligence, the singapore quick commerce market size was valued at USD 368.03 million in 2025 and is estimated to grow from USD 387.68 million in 2026 to reach USD 502.86 million by 2031, at a CAGR of 5.34% during the forecast period (2026-2031).

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Flowers and Gifts), and Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Quick Commerce Market Trends and Insights

Proliferation Of Smartphone-Enabled On-Demand Culture

Singapore records smartphone penetration near 165%, and mobile checkouts represent 85% of all e-commerce purchases. Such ubiquity has schooled households to treat instant fulfillment as default service, compressing the margin of error for delivery reliability. Surveys show 80% of residents expect same-day delivery and 61% want receipt within three hours, while half of Deliveroo users now order groceries, retail items, or gifts in addition to meals. Digital wallets covering 39% of e-commerce payments enable one-tap checkout, converting browsing impulses into incremental orders that lift frequency for the Singapore quick commerce market. Platforms that marry frictionless payment with predictive reorder prompts secure an outsized share of high-frequency baskets such as snacks or personal care.

Expansion Of Dark Store Networks Across Singapore

Micro-fulfillment nodes closed to foot traffic are mushrooming across dense residential pockets to shrink last-mile distances. Foodpanda's Pandamart outlets in Kallang and Yio Chu Kang stock 5,000-plus SKUs and use AI to stage goods within two-kilometer radii, cutting average drop-times to below 25 minutes and reducing rider idle minutes by double digits. Lazada's RedMart Now, launched in February 2026, leverages zoned facilities that bypass legacy store replenishment, promising 30-minute delivery in south-central and western districts. Singapore's planners accelerate the trend by rezoning large brownfield sites such as Bukit Timah Turf City into mixed-use precincts where ground-level logistics can coexist with housing. Real-estate costs still loom large, but operators mitigate rents through higher order density, subscription programs, and automated picking that boost throughput per square foot, helping sustain profitable expansion of the Singapore quick commerce market.

High Real-Estate And Labor Costs Eroding Margins

Industrial land in core logistics precincts commands premium leases that strain unit margins for micro-fulfillment operators. Sheng Siong spent SGD 520 million (USD 384.8 million) to relocate its automated warehouse to Sungei Kadut, illustrating the heavy capital now required merely to secure suitable floor area. Delivery riders earn SGD 8-12 (USD 5.92-8.88) per hour, and November 2025 safety rules mandate rest breaks and speed caps that trim deliveries per shift by up to 15%. Ultra-dense dark stores must book 150-200 daily orders just to break even under these cost conditions. The Singapore quick commerce market therefore tilts toward players with either multichannel scale or third-party logistics alliances that dilute fixed expenses across larger revenue pools.

Other drivers and restraints analyzed in the detailed report include:

- Strategic Investments By Super Apps And E-Commerce Giants

- Government Support For Cashless Payments And Digitalization

- Stringent Urban Traffic Regulations Limiting Delivery Windows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and Staples secured 53.61% of the Singapore quick commerce market in 2025, buoyed by frequent top-up purchasing patterns and a reliable inventory cycle that turns stock 15-20 times annually. The Deliveroo-Sheng Siong exclusive partnership placed more than 5,000 SKUs online with 24-hour access, proving that legacy grocers can lift reach without cannibalizing footfall. Fresh Produce and Dairy, though smaller, shows the highest momentum at a 5.88% CAGR through 2031; capacity gains stem from Ninja Van's cold-chain fleet and from Pandamart XL sites that expanded chilled lines by 30%. Non-food niches offer margin upsides, OnePhone's one-hour phone replacement service and ElectronicsCrazy's three-hour urgent delivery monetize willingness to pay for speed on high-value, low-weight items. Pharmacies such as Glovida broaden the category mix by shipping over-the-counter products under Health Sciences Authority oversight, deepening consumer trust. Operators that integrate ambient, chilled, and frozen zones within a single facility can meet full-basket needs, increasing wallet share inside the Singapore quick commerce market size for multipurpose missions.

The breadth-versus-depth trade-off remains critical. Grocery ensures volume, perishables demand temperature precision, and impulse categories widen margins. Platforms mastering predictive slotting across these temperature bands elevate service reliability and become default household suppliers. Those lagging in cold-chain rigor or SKU breadth risk relegation to occasional-use status, limiting their share of the Singapore quick commerce market size.

List of Companies Covered in this Report:

- Grab Holdings Inc.

- Delivery Hero SE (foodpanda)

- Deliveroo plc

- Sea Ltd.

- Amazon.com Inc.

- Lazada Group S.A.

- FairPrice Group

- Sheng Siong Group Ltd.

- DFI Retail Group Holdings Ltd. (7-Eleven)

- Pick & GO Pte. Ltd.

- AirAsia Digital Sdn. Bhd. (airasia food)

- ZTP Herbal Tea Pte. Ltd.

- WhyQ Pte. Ltd.

- Honestbee Pte. Ltd.

- J&T Express (Singapore) Pte. Ltd.

- Ninjavan Pte. Ltd.

- Lalamove Singapore Pte. Ltd.

- Ryde Technologies Pte. Ltd.

- HappyFresh (Singapore) Pte. Ltd.

- Foodology Delivery Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Smartphone-Enabled On-Demand Culture

- 4.2.2 Expansion of Dark Store Networks Across Singapore

- 4.2.3 Strategic Investments by Super Apps and E-Commerce Giants

- 4.2.4 Government Support for Cashless Payments and Digitalization

- 4.2.5 Emergence of AI-Driven Predictive Inventory Management

- 4.2.6 Cross-Border Micro-Fulfillment Hubs Serving Johor-Singapore Corridor

- 4.3 Market Restraints

- 4.3.1 High Real-Estate and Labor Costs Eroding Margins

- 4.3.2 Stringent Urban Traffic Regulations Limiting Delivery Windows

- 4.3.3 Volatility in Venture Funding for Hyperlocal Startups

- 4.3.4 Consumer Fatigue Toward Delivery App Promotions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Grab Holdings Inc.

- 6.4.2 Delivery Hero SE (foodpanda)

- 6.4.3 Deliveroo plc

- 6.4.4 Sea Ltd.

- 6.4.5 Amazon.com Inc.

- 6.4.6 Lazada Group S.A.

- 6.4.7 FairPrice Group

- 6.4.8 Sheng Siong Group Ltd.

- 6.4.9 DFI Retail Group Holdings Ltd. (7-Eleven)

- 6.4.10 Pick & GO Pte. Ltd.

- 6.4.11 AirAsia Digital Sdn. Bhd. (airasia food)

- 6.4.12 ZTP Herbal Tea Pte. Ltd.

- 6.4.13 WhyQ Pte. Ltd.

- 6.4.14 Honestbee Pte. Ltd.

- 6.4.15 J&T Express (Singapore) Pte. Ltd.

- 6.4.16 Ninjavan Pte. Ltd.

- 6.4.17 Lalamove Singapore Pte. Ltd.

- 6.4.18 Ryde Technologies Pte. Ltd.

- 6.4.19 HappyFresh (Singapore) Pte. Ltd.

- 6.4.20 Foodology Delivery Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment