PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062408

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062408

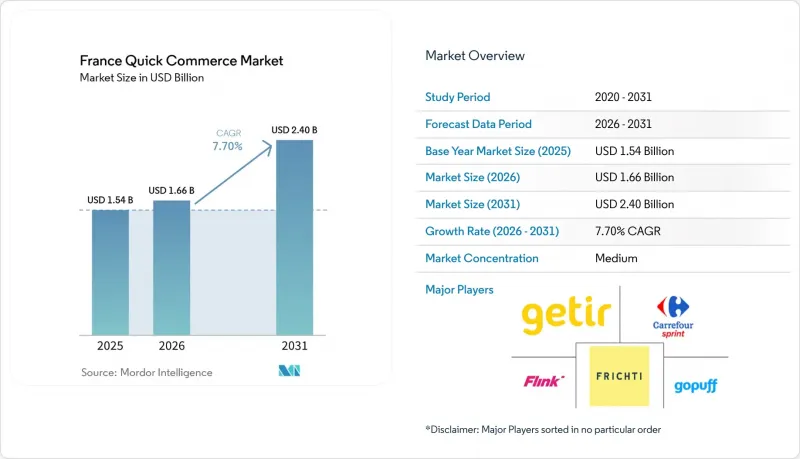

France Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the france quick commerce market size is expected to increase from USD 1.54 billion in 2025 to USD 1.66 billion in 2026 and reach USD 2.40 billion by 2031, growing at a CAGR of 7.7% over 2026-2031.

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Pet Care, and Flowers and Gifts), and Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

France Quick Commerce Market Trends and Insights

Growing Consumer Demand For Ultrafast Delivery Convenience

Time-pressed households in dense French cities increasingly choose speed over price when purchasing everyday goods, an effect reinforced by mobile wallet adoption that exceeds 82% among 16-24-year-olds. DPD's 2025 Barometre showed 37% of shoppers abandon online baskets if delivery windows appear lengthy, validating the value that rapid fulfillment adds to the France quick commerce market. Uber Eats now reaches 530-plus agglomerations, proving that demand for near-instant delivery is no longer restricted to Paris-Lyon-Marseille but extends into midsized towns where courier density can still support sub-30-minute service.

Expansion Of Dark Store Networks Across Major French Cities

After a regulatory reset in 2023 classified dark stores as warehouses, retailers began integrating micro-fulfillment zones within existing stores to comply with zoning while preserving speed. Carrefour's Sprint format and Monoprix's 200-store Uber Eats network illustrate how compliant dark-store-in-store models sustain the France quick commerce market without fresh real-estate outlays. Picnic's planned Q4 2026 launch in Lyon further confirms that disciplined dark-store deployment remains viable when aligned with municipal plans and anchored in positive unit economics.

Persistent Profitability Challenges Due To High Last-Mile Costs

Courier wages averaging EUR 17 (USD 19) per hour translate into USD 4.80-7.68 per drop when riders only complete three deliveries hourly. With typical delivery fees sitting below USD 2.30, most operators run sustained losses, and four venture-funded entrants shut down between 2023-2024. Survivors now impose higher order minimums and stretch windows to 2 hours to batch drops, yet profitability outside dense metros remains elusive, limiting expansion of the France quick commerce market.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of AI-Driven Demand Forecasting To Reduce Spoilage

- Rising Partnerships Between Quick Commerce And Traditional Retailers

- Intensifying Municipal Restrictions On Urban Micro-Warehouses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and Staples held 57.61% revenue in 2025, acting as the trip-builder for cross-selling higher-margin items that lift the overall French quick commerce market size at the basket level. Fresh Produce and Dairy contributes rising turnover as consumers shift from weekly stock-ups to daily top-ups for perishables, leveraging the channel's same-day freshness. Snacks and Beverages thrive on impulse demand, while Personal Care and OTC Pharma benefit from the willingness to pay premiums to avoid late-night pharmacy trips. Electronics, Flowers and Gifts, and other niche categories command smaller shares but deliver superior margins because customers value immediate gratification.

Pet Care is forecast to grow at a 7.96% CAGR, the strongest of any category, driven by subscription models for recurrent deliveries and rising preference for premium local pet food. Zooplus' February 2026 purchase of JMT pushed combined turnover over USD 169 million and underscored consolidation momentum. The France quick commerce market share attributable to Pet Care is set to widen as owners increasingly treat pets as family and accept higher delivery fees for reliable just-in-time supply.

List of Companies Covered in this Report:

- Kwez

- Picky

- Florajet

- LAMOU PARIS

- Carrefour SA

- Frichti SAS

- Uber Eats France SAS

- Deliveroo France SAS

- Just Eat Takeaway.com N.V. (France)

- La Belle Vie SAS

- Amazon France Logistique SAS

- Casino Guichard-Perrachon SA

- Monoprix SAS

- Auchan Retail France SA

- E. Leclerc (SCA Ouest)

- Intermarche (Les Mousquetaires)

- Picnic International B.V. (France)

- Cajoo SAS

- Franprix Holding SAS

- Stuart Delivery SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Growing Consumer Demand for Ultrafast Delivery Convenience

- 4.3.2 Expansion of Dark Store Networks Across Major French Cities

- 4.3.3 Integration of AI-Driven Demand Forecasting to Reduce Spoilage

- 4.3.4 Rising Partnerships Between Quick Commerce and Traditional Retailers

- 4.3.5 Regulatory Incentives for Electric Cargo Bike Adoption in Urban Logistics

- 4.3.6 Increasing Penetration of Mobile Wallet Payments Among Gen Z Consumers

- 4.4 Market Restraints

- 4.4.1 Persistent Profitability Challenges Due to High Last-Mile Costs

- 4.4.2 Intensifying Municipal Restrictions on Urban Micro-Warehouses

- 4.4.3 Shortage of Qualified Delivery Riders in Smaller Cities

- 4.4.4 Consumer Price Sensitivity Amid Inflationary Pressures

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

- 5.3 By City Tier

- 5.3.1 Tier I Metros

- 5.3.2 Tier II Cities

- 5.3.3 Tier III and Below

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kwez

- 6.4.2 Picky

- 6.4.3 Florajet

- 6.4.4 LAMOU PARIS

- 6.4.5 Carrefour SA

- 6.4.6 Frichti SAS

- 6.4.7 Uber Eats France SAS

- 6.4.8 Deliveroo France SAS

- 6.4.9 Just Eat Takeaway.com N.V. (France)

- 6.4.10 La Belle Vie SAS

- 6.4.11 Amazon France Logistique SAS

- 6.4.12 Casino Guichard-Perrachon SA

- 6.4.13 Monoprix SAS

- 6.4.14 Auchan Retail France SA

- 6.4.15 E. Leclerc (SCA Ouest)

- 6.4.16 Intermarche (Les Mousquetaires)

- 6.4.17 Picnic International B.V. (France)

- 6.4.18 Cajoo SAS

- 6.4.19 Franprix Holding SAS

- 6.4.20 Stuart Delivery SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment