PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062306

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062306

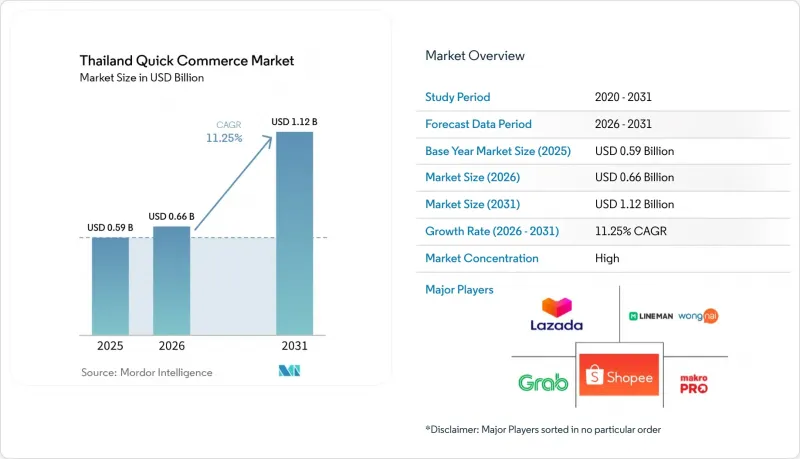

Thailand Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the thailand quick commerce market size was valued at USD 0.59 billion in 2025 and estimated to grow from USD 0.66 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 11.25% during the forecast period (2026-2031).

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), and Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Quick Commerce Market Trends and Insights

Rapid Smartphone Penetration and High Mobile Broadband Coverage

The Thailand quick commerce market rests on a mobile-first ordering base that is already broad and stable. Thailand recorded 4G population coverage at 98% and active mobile broadband subscriptions at 122 per 100 inhabitants, which gives platforms the connectivity depth needed for app-led ordering and live dispatch. The GSMA Mobile Connectivity Index 2025 also placed Thailand among the stronger upper-middle performers in Southeast Asia on infrastructure and consumer readiness, which supports wider use of app-based retail services. This level of network quality matters because quick commerce relies on location tracking, instant order confirmation, and continuous rider communication during every trip. The same connectivity also lets rider fleets operate as connected logistics nodes, which improves route reassignment and favors larger platforms with stronger dispatch systems.

Growing Urban Millennial and Gen Z Consumer Base In Bangkok and Tier II Cities

The Thailand quick commerce market is also benefiting from a younger urban customer base that uses digital services as part of everyday spending. LINE MAN Wongnai served more than 10 million monthly users and listed more than 700,000 restaurants across all 77 provinces, which shows how deeply app-based ordering is already embedded in consumer behavior. Shopee Thailand stated in April 2026 that it was expanding faster delivery options, including a premium 1-hour tier, which points to willingness among younger users to pay more for speed in selected use cases. That matters for the Thailand quick commerce market because speed premiums are easier to monetize when users already treat apps as their default buying channel for daily needs. It also increases the value of multi-service ecosystems, where grocery, food delivery, payments, and financial products can reinforce each other inside the same app environment.

Margin Pressure From Extensive Rider Incentive Programs

The Thailand quick commerce market faces its clearest near-term pressure in rider incentives and last-mile costs. Bangkok Post reported that rider incentive costs exceeded 35% of ticket value during peak hours for Bangkok-based operators, which shows how quickly margins can narrow when platforms compete for rider availability. In April 2026, Kerry Express, Flash Express, and J&T Express raised shipping fees by THB 3 (USD 0.08) per shipment, citing higher fuel costs and a move away from subsidized pricing. This changes the cost base for the Thai quick-commerce market because low-fee delivery has supported basket conversion even when order values are small. Platforms with subscriptions, stronger route optimization, or in-house rider networks are better placed to absorb this pressure than operators that still depend on high promotional spending.

Other drivers and restraints analyzed in the detailed report include:

- Rising Investor Interest in Dark-Store Infrastructure Buildouts

- Partnership Momentum Between Convenience Chains and Delivery Apps

- Intensifying Regulatory Scrutiny on Gig-Worker Welfare

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and Staples retained a 53.48% share of the Thailand quick commerce market in 2025, which made it the largest product category by a clear margin. This lead came from habitual daily and weekly replenishment behavior, which aligns with dark-store stocking and repeat-order planning. LINE MAN Wongnai's 2025 year-end data showed strong recurring food demand, while Grab also reported very high ordering volumes for core daily-consumption items, which supports the role of routine consumption in maintaining high order frequency. The category also benefits from convenience-store integration, as store-based fulfillment makes it easier to serve frequent baskets without bearing the full inventory costs of a dedicated dark-store network.

Fresh Produce and Dairy, Snacks and Beverages, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and other smaller lines all add to basket expansion and category diversification. Shopee Thailand's 2026 move into fresh flower delivery via ShopeeFood riders shows that platforms are expanding the quick-delivery catalog to include purchases that were not historically part of the same-day grocery trip. Personal Care and OTC Pharma is forecast to grow at an 11.56% CAGR through 2031, the fastest pace across product categories, as speed and convenience matter more for health-adjacent buying decisions. The Thailand quick commerce industry also gains from the overlap between grocery and health-related fulfillment, because both can benefit from stronger cold handling, tighter inventory control, and denser local delivery coverage. This gives the Thailand quick commerce market a practical route to category expansion without needing a completely separate operating model for each new product line.

List of Companies Covered in this Report:

- Grab Holdings Ltd.

- LINE MAN Wongnai (Thailand) Co., Ltd.

- Shopee Thailand Ltd.

- CP All Public Company Limited (7-Eleven Now)

- Central Retail Corporation Public Company Limited (Tops Quick)

- Ek-Chai Distribution System Co., Ltd. (Lotus's Smart Quick)

- Big C Supercenter Public Company Limited

- Tops Online

- TikTok Shop Thailand

- Lazada Group S.A. (Lazada Express Quick Commerce)

- Siam Makro Public Company Limited (Makro Quick)

- Kerry Express (Thailand) Public Company Limited

- SCGJWD Logistics Public Company Limited (JWD Express)

- Freshket Co., Ltd.

- Fresh Living Co., Ltd. (Fresh Living Mart)

- Veloce Logistics Co., Ltd.

- Lalamove EasyVan (Thailand) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Smartphone Penetration and High Mobile Broadband Coverage

- 4.2.2 Growing Urban Millennial and Gen Z Consumer Base in Bangkok and Tier II Cities

- 4.2.3 Rising Investor Interest in Dark-Store Infrastructure Build-Outs

- 4.2.4 Partnership Momentum Between Convenience Chains and Delivery Apps

- 4.2.5 Expansion of Instant Payment Rails Enabling Micro-Ticket Transactions

- 4.2.6 Surge in Corporate -Lunch-Hour-Basket Orders from CBD Offices

- 4.3 Market Restraints

- 4.3.1 Margin Pressure From Extensive Rider Incentive Programs

- 4.3.2 Intensifying Regulatory Scrutiny on Gig-Worker Welfare

- 4.3.3 High Per-Order Logistics Cost Outside Bangkok Metropolitan Region

- 4.3.4 Limited Cold-Chain Capacity for Fresh Produce in Tier III Cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Grab Holdings Ltd.

- 6.4.2 LINE MAN Wongnai (Thailand) Co., Ltd.

- 6.4.3 Shopee Thailand Ltd.

- 6.4.4 CP All Public Company Limited (7-Eleven Now)

- 6.4.5 Central Retail Corporation Public Company Limited (Tops Quick)

- 6.4.6 Ek-Chai Distribution System Co., Ltd. (Lotus's Smart Quick)

- 6.4.7 Big C Supercenter Public Company Limited

- 6.4.8 Tops Online

- 6.4.9 TikTok Shop Thailand

- 6.4.10 Lazada Group S.A. (Lazada Express Quick Commerce)

- 6.4.11 Siam Makro Public Company Limited (Makro Quick)

- 6.4.12 Kerry Express (Thailand) Public Company Limited

- 6.4.13 SCGJWD Logistics Public Company Limited (JWD Express)

- 6.4.14 Freshket Co., Ltd.

- 6.4.15 Fresh Living Co., Ltd. (Fresh Living Mart)

- 6.4.16 Veloce Logistics Co., Ltd.

- 6.4.17 Lalamove EasyVan (Thailand) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment