PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063405

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063405

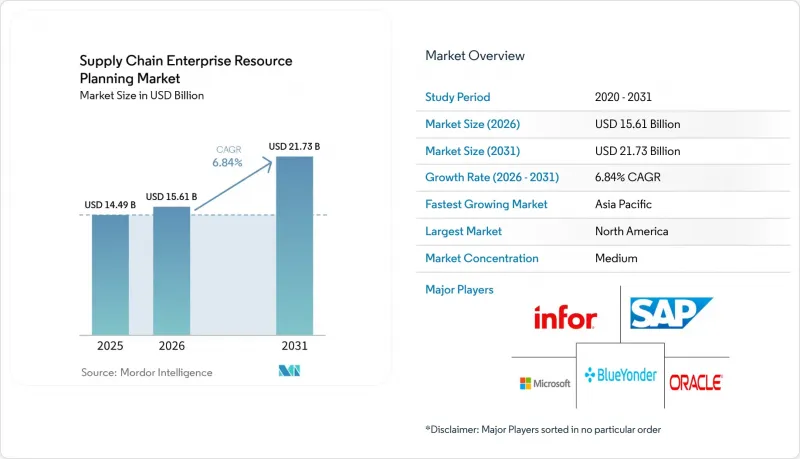

Supply Chain Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the supply chain enterprise resource planning market size was valued at USD 14.49 billion in 2025 and estimated to grow from USD 15.61 billion in 2026 to reach USD 21.73 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), End-User Industry (Manufacturing, Consumer Goods, Healthcare and Pharmaceuticals, Food and Beverage, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Supply Chain Enterprise Resource Planning Market Trends and Insights

Cloud-First Migration of Tier-1 ERP Suites

Tier-1 vendors target aggressive cloud-adoption milestones, promising continuous feature delivery, elastic simulation capacity, and easier integration with third-party logistics. Migrations typically lower the five-year total cost of ownership by a moderate share, yet hidden data cleansing and process re-engineering work often extends project timelines. Vendors bundle automated migration toolkits and fixed-price packages to reduce friction, while customers increasingly insist on outcome-based contracts tied to go-live milestones. Additionally, the shift to cloud-based solutions is driving innovation in service delivery models. The supply chain ERP market vendors are leveraging artificial intelligence and machine learning to enhance predictive analytics, enabling businesses to make data-driven decisions more effectively. This trend is particularly evident in industries like manufacturing and retail, where real-time insights are critical for optimizing operations. As a result, companies are increasingly viewing cloud adoption not just as a cost-saving measure but as a strategic investment to gain a competitive edge.

AI-Enabled Predictive Supply Chain Planning

Machine-learning algorithms now ingest unstructured weather feeds, supplier emails, and social sentiment to fine-tune demand forecasts and proactively reroute shipments. Embedded copilots reduce manual data entry by up to a moderate share and enable enterprises to maintain leaner safety stock without eroding service levels. Reliability still hinges on harmonized historical data, giving an additional push toward unified, cloud-native environments. As a result, businesses are increasingly prioritizing investments in advanced analytics to enhance operational efficiency and decision-making.

Cyber-Security and Data-Sovereignty Compliance Costs

Jurisdictions such as the EU, China, and India demand in-country data storage and impose stiff penalties for violations. Multinationals, therefore, maintain region-specific ERP instances, thereby increasing infrastructure costs and complicating master data synchronization. Zero-trust security, multi-factor authentication, and anomaly detection add 10-15% to annual subscription fees, a burden felt most acutely by mid-market firms. Additionally, compliance with these regulations often requires significant investment in IT infrastructure upgrades to meet local standards. This trend, in the supply chain ERP market, is driving demand for specialized consulting services to navigate the complexities of regional compliance requirements.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Composable and Modular Architectures

- Near-Shoring and Resilience Programs

- Shortage of ERP-Skilled Supply-Chain Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services slice of the supply chain enterprise resource planning market is expanding at a 7.24% CAGR, eclipsing software growth as projects require intensive data cleansing, integration, and change management. Implementation and managed-service contracts increasingly hinge on performance outcomes such as order-to-cash cycle days. Software still generated 63.71% of value in 2025, buoyed by subscription revenue from tier-1 suites and algorithmic planning add-ons that underpin modern supply networks. Continuous-improvement retainers now keep consultants embedded long after go-live, turning services into an annuity stream. Meanwhile, software providers blur category lines by bundling basic support and hosting, prompting buyers to evaluate true cost across both line items. Open-source challengers leverage all-inclusive pricing to cut total ownership costs and woo small and medium enterprises.

As the market evolves, enterprises increasingly prioritize agility and scalability in their ERP solutions to adapt to dynamic supply chain demands. Vendors are responding by integrating advanced analytics and AI-driven insights to enhance decision-making capabilities. Additionally, the shift toward modular ERP systems allows businesses to adopt functionalities incrementally, reducing upfront costs and implementation risks. This trend is particularly appealing to mid-market firms, which often face budget constraints but require robust solutions to remain competitive. The growing emphasis on sustainability and compliance further drives innovation, with ERP providers embedding features to track carbon footprints and ensure regulatory adherence.

Cloud installations accounted for 58.83% of 2025 revenue and are accelerating by 7.44% through 2031, propelled by hyperscaler discounts and elastic capacity for simulation workloads. Hybrid structures persist in defense, utilities, and public-sector contexts where sensitive ledgers remain on-premise while collaboration modules live in the cloud. On-premise adoption is declining, but endures where air-gapped security trumps scalability. Edge-caching appliances and regional data centers mitigate latency and residency hurdles, broadening cloud appeal in bandwidth-constrained territories. Subscription models also distribute cash outlays more evenly, an advantage for manufacturers juggling capital budgets. As a result, cloud footprints are expected to exceed 70% of new deployments well before the forecast horizon, further reshaping vendor economics.

Additionally, the integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) into cloud-based ERP systems is driving operational efficiencies across industries. These technologies enable real-time data analysis, predictive insights, and automated decision-making, which are critical for businesses aiming to stay competitive in dynamic markets. Furthermore, the growing emphasis on sustainability is pushing organizations to adopt cloud solutions that optimize energy consumption and reduce carbon footprints. Vendors are increasingly offering green cloud services, aligning with corporate environmental, social, and governance (ESG) goals, which is expected to further accelerate cloud adoption during the forecast period.

Geography Analysis

North America remains the single largest regional contributor, with a 36.18% share in 2025, anchored by the United States' drive toward AI-augmented planning and nearshore manufacturing. Canadian producers adopt ERP systems to meet export rules-of-origin documentation requirements, while Mexican maquiladoras upgrade systems to manage dual-sourcing models spanning domestic and U.S. suppliers. Widespread 5G connectivity and hyperscaler data-center density enable real-time control-tower dashboards, shrinking response times to supply disruptions.

Asia-Pacific posts the most dynamic growth trajectory with a CAGR of 7.84% over the forecast period. India's compliance-ready templates automate goods and services tax reporting, encouraging even mid-market firms to migrate away from spreadsheets. Japanese conglomerates are phasing out on-premises systems as domestic cloud vendors guarantee low-latency availability zones. In China, state-led substitution campaigns steer enterprises toward locally maintained ERP copies that pass stringent cybersecurity reviews, without sacrificing integration with global supply networks.

Europe balances regulatory compliance with sustainability leadership. The ViDA e-invoicing roll-out enables borderless data exchange across the region, while the Digital Product Passport requires manufacturers to trace their carbon footprint from raw extraction through end-of-life recycling. German automotive suppliers pilot blockchain-backed certificates of origin built directly into ERP line items. Nordic retailers incorporate circular-economy returns data, enabling refurbish and resale programs. Eastern European plants leverage EU cohesion funds to digitalize factories, adding incremental demand for modular suites. South America, the Middle East, and Africa are smaller markets but are steadily growing as governments invest in digital infrastructure and local enterprises aim to compete with multinational subsidiaries. Brazil's ERP adoption surpassed 33% in 2025, with further growth expected as the government digitizes tax compliance processes.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- IFS AB

- QAD, Inc.

- Plex Systms, Inc.

- The Sage Group Plc

- SYSPRO (Proprietary) Ltd

- Acumatica, Inc.

- Unit4 N.V.

- Workday, Inc.

- Blue Yonder Group, Inc.

- Kinaxis Inc.

- E2open Parent Holdings, Inc.

- Manhattan Associates, Inc.

- Ramco Systems Ltd

- Odoo SA

- Aptean, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Migration of Tier-1 ERP Suites

- 4.2.2 AI-Enabled Predictive Supply Chain Planning

- 4.2.3 Rise of Composable and Modular ERP Architectures

- 4.2.4 Near-shoring and Supply Chain Resilience Programs

- 4.2.5 Sustainability and Scope-3 Carbon-Tracking Mandates

- 4.2.6 Generative-AI Agents Automating Procure-to-Pay

- 4.3 Market Restraints

- 4.3.1 Generative-AI Agents Automating Procure-to-Pay

- 4.3.2 Cyber-Security and Data-Sovereignty Compliance Costs

- 4.3.3 Shortage of ERP-Skilled Supply-Chain Talent

- 4.3.4 Vendor Lock-In and Long-Term Total-Cost Concerns

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By End-User Industry

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-commerce

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Food and Beverage

- 5.3.5 Consumer Goods

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 IFS AB

- 6.4.7 QAD, Inc.

- 6.4.8 Plex Systms, Inc.

- 6.4.9 The Sage Group Plc

- 6.4.10 SYSPRO (Proprietary) Ltd

- 6.4.11 Acumatica, Inc.

- 6.4.12 Unit4 N.V.

- 6.4.13 Workday, Inc.

- 6.4.14 Blue Yonder Group, Inc.

- 6.4.15 Kinaxis Inc.

- 6.4.16 E2open Parent Holdings, Inc.

- 6.4.17 Manhattan Associates, Inc.

- 6.4.18 Ramco Systems Ltd

- 6.4.19 Odoo SA

- 6.4.20 Aptean, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment