PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065565

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065565

Enterprise Resource Planning Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

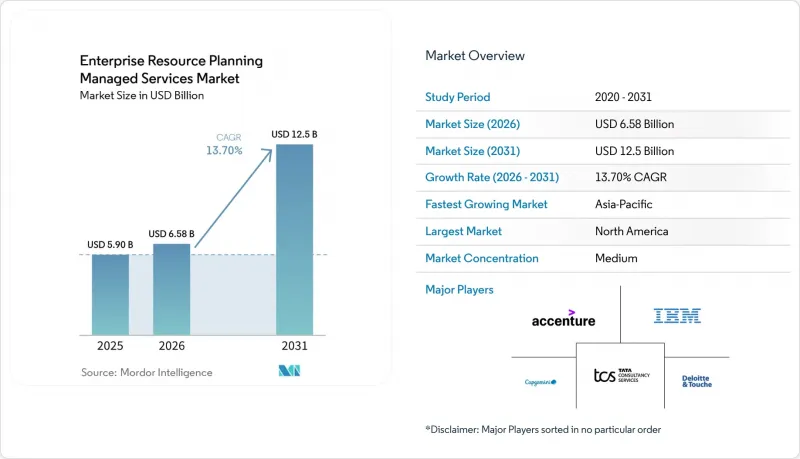

According to Mordor Intelligence, the eRP managed services market size is projected to be USD 5.90 billion in 2025, USD 6.58 billion in 2026, and reach USD 12.50 billion by 2031, growing at a CAGR of 13.7% from 2026 to 2031.

This report is Segmented by Deployment Model (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Industry Vertical (Manufacturing, Retail and Consumer Goods, Healthcare, Banking, Financial Services and Insurance (BFSI), IT and Telecom, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Managed Services Market Trends and Insights

Growing Adoption of Cloud-Based ERP Solutions

More than 70% of enterprises now operate at least one core ERP module in the cloud, and 75% of new buyers favor cloud-native architectures over on-premises deployments. Hyperscaler partnerships bundle ERP subscriptions with infrastructure credits and AI services, as demonstrated by SAP's RISE offering on IBM Power Virtual Server, while Oracle Cloud Infrastructure revenue surged 52% in fiscal 2025 on the back of ERP migrations. Sovereign-cloud mandates in China and the European Union drive multi-region, legally isolated ERP instances that still enable cross-border analytics through federated data models. Consumption-based pricing and 90-day deployment frameworks, such as Unit4's Success4U, are unlocking the mid-market, forcing service providers without deep hyperscaler alliances or compliance-ready delivery models to cede share.

Increasing Need to Reduce IT Infrastructure Costs

Subscription-driven managed services are replacing fixed infrastructure outlays, converting data-center depreciation into operating expense and trimming total IT spend by up to 30% in documented cases such as IBM's 150,000-user internal migration to SAP S/4HANA Cloud. Government buyers are following suit: the U.S. Defense Logistics Agency issued a USD 903 million, seven-year contract that shifts budget-predictability risk to service providers while mandating 99.9% availability and FedRAMP IL4 compliance. Small and medium enterprises alone will direct more than USD 90 billion to managed IT services through 2026, lured by fixed-fee models that eliminate the need for in-house ERP teams. The countertrend is a rising unit cost for multi-cloud-certified ERP specialists, compelling providers to invest in reskilling and AI delivery platforms to protect margins.

Data Security and Privacy Concerns in Outsourced Environments

The July 2024 Smart ERP Solutions breach exposed 79,000 personal records and triggered EUR 480,000 (USD 540,000) in GDPR fines, plus nearly EUR 840,000 (USD 945,000) in lost business, illustrating how a single incident can erase multiple years of managed-service fees. Zero-day exploits in SAP NetWeaver prompted clients to adopt 24x7 managed security services with continuous penetration testing and zero-trust architectures. Public-sector solicitations now stipulate sovereign-cloud deployment, government-owned encryption keys, and U.S.-citizen staffing, raising the compliance bar for providers. Vendors lacking ISO 27001 certification or cyber-insurance will struggle to pass procurement gates in regulated verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Data Analytics

- Growing Complexity of ERP Landscapes Due to Multi-Vendor Ecosystems

- High Switching Costs and Vendor Lock-In

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions accounted for 54.8% of the ERP managed services market in 2025 and are on track to expand at a 12.9% CAGR through 2031. Oracle Cloud Infrastructure's FY 2025 revenue surge, SAP's RISE migrations, and Alibaba Cloud sovereign deployments in China confirm that subscription pricing, automatic updates, and hyperscaler AI services are now decisive purchase criteria. While on-premises deployments linger in defense and critical-infrastructure sectors that require air-gapped security, even those buyers are layering cloud-based analytics on top of core financial systems. Hybrid configurations blending public cloud for innovation workloads with private or sovereign cloud for regulated data are steadily growing, demanding orchestration skills that only a subset of providers possess.

Margins in legacy on-premises arrangements are pinched as vendors funnel Research and Development to cloud-native functionality, pushing customers toward migration. Meanwhile, managed service practices that combine compliance tooling, modular upgrades, and gain-share economics are capturing wallet share from traditional application management contracts. As a result, the ERP managed services market is tilting decisively toward cloud-centric frameworks, and providers without hyperscaler certifications risk obsolescence.

Geography Analysis

North America generated 34.1% of global revenue in 2025, anchored by federal modernization programs and well-established outcome-based procurement frameworks. The Defense Logistics Agency's USD 903 million contract and Estee Lauder's USD 500 million partnership with Accenture typify multi-year deals that integrate AI automation and sovereign-cloud compliance. Strong capital pools and mature vendor ecosystems sustain growth, even as labor shortages drive up the cost of certified ERP talent.

Asia-Pacific is the fastest-growing region, with a 13.6% CAGR, driven by China's Xinchuang mandates, India's mass deployment of Microsoft Copilot licenses, and Japan's shift from legacy ECC systems to S/4HANA. The ERP managed services market in China alone reached USD 3.40 billion in 2025, with domestic vendors Yonyou and Kingdee capturing the bulk of state-owned enterprise spend, while multinational corporations rely on SAP via Alibaba Cloud sovereign instances. India's tier-1 integrators are exporting low-cost, AI-enabled support tooling worldwide, turning the subcontinent into the labor fulcrum of global delivery.

Europe shows slower topline growth but acute talent scarcity, with S/4HANA specialists now taking 90 days to recruit. Mandatory e-invoicing in France by September 2026 and Digital Product Passport requirements in energy utilities create compliance-driven demand spikes. South America, the Middle East, and Africa remain nascent but opportunity-rich, particularly where localization templates for tax, payroll, and customs are scarce. Providers that can orchestrate multi-country rollouts with continuous compliance updates will unlock first-mover advantages across these emerging regions.

- Accenture plc

- International Business Machines Corporation

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Infosys Limited

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- HCL Technologies Limited

- NTT DATA Corporation

- DXC Technology Company

- Atos SE

- Fujitsu Limited

- Tech Mahindra Limited

- CGI Inc.

- SAP SE

- Oracle Corporation

- Syntax Systems GmbH and Co. KG

- Rimini Street, Inc.

- Navisite LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based ERP Solutions

- 4.2.2 Increasing Need to Reduce IT Infrastructure Costs

- 4.2.3 Rising Demand for Real-Time Data Analytics

- 4.2.4 Growing Complexity of ERP Landscapes Due to Multi-Vendor Ecosystems

- 4.2.5 Emergence of AI-Driven Autonomous ERP Operations

- 4.2.6 Vendor Push for Outcome-Based Managed Service Contracts

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns in Outsourced Environments

- 4.3.2 High Switching Costs and Vendor Lock-In

- 4.3.3 Shortage of Domain-Specific ERP Talent in Service Providers

- 4.3.4 Rising Scrutiny of Scope 3 Emissions from Outsourced IT Operations

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 Retail and Consumer Goods

- 5.3.3 Healthcare

- 5.3.4 Banking, Financial Services and Insurance (BFSI)

- 5.3.5 Information Technology and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Energy and Utilities

- 5.3.8 Transportation and Logistics

- 5.3.9 Other Industry Verticals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Turkey

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 International Business Machines Corporation

- 6.4.3 Deloitte Touche Tohmatsu Limited

- 6.4.4 Capgemini SE

- 6.4.5 Infosys Limited

- 6.4.6 Cognizant Technology Solutions Corporation

- 6.4.7 Tata Consultancy Services Limited

- 6.4.8 Wipro Limited

- 6.4.9 HCL Technologies Limited

- 6.4.10 NTT DATA Corporation

- 6.4.11 DXC Technology Company

- 6.4.12 Atos SE

- 6.4.13 Fujitsu Limited

- 6.4.14 Tech Mahindra Limited

- 6.4.15 CGI Inc.

- 6.4.16 SAP SE

- 6.4.17 Oracle Corporation

- 6.4.18 Syntax Systems GmbH and Co. KG

- 6.4.19 Rimini Street, Inc.

- 6.4.20 Navisite LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment