PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065553

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065553

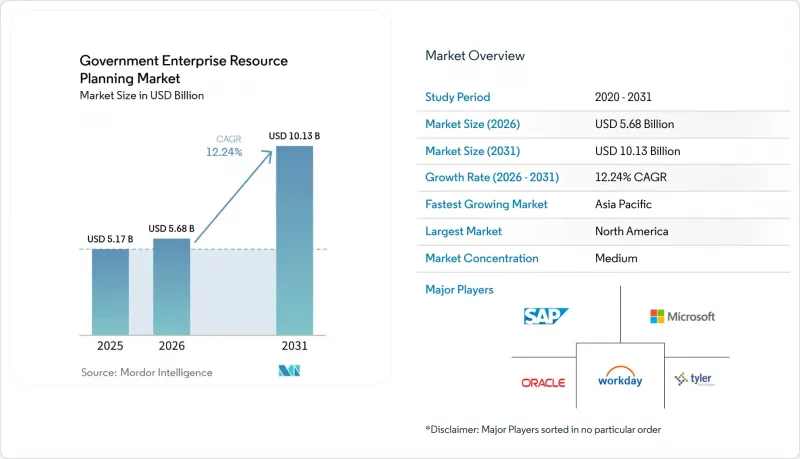

Government Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the government eRP market size is expected to increase from USD 5.17 billion in 2025 to USD 5.68 billion in 2026 and reach USD 10.13 billion by 2031, growing at a CAGR of 12.24% over 2026-2031.

This report is Segmented by Deployment Mode (On-Premises ERP, Cloud ERP, and Hybrid ERP), Module (Financial Management, Human Capital Management, and Other Modules), Government Level (Federal/National, State/Provincial, and Local/Municipal), Component (Software and Services), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Government Enterprise Resource Planning Market Trends and Insights

Digital Transformation Mandates In Government

Mandatory cloud-first directives are making decades-old mainframes prime candidates for replacement. Oklahoma's 2026-2028 plan requires every agency to adopt cloud architectures by fiscal 2028, and Tennessee earmarked USD 47 million for legacy ERP retirement in FY2026. Vermont is consolidating 14 disparate ledgers, mirroring dozens of U.S. states where COBOL retirements outpace hiring pipelines. Australia shortened procurement lead times from 36 to 12 months by launching a pre-qualified vendor panel in February 2026, unlocking backlogged projects. Because these mandates couple deadlines with audit penalties, budget allocations are ring-fenced, ensuring consistent demand even where internal IT capacity is thin.

Cost Savings From Cloud Migration

Financial models show 30-40% lower five-year total cost of ownership versus on-premises, making cloud attractive for budget-pressed treasuries. The United Kingdom partnered with Rackspace Technology and Rubrik in 2025 to build a sovereign cloud that meets data-residency rules without sacrificing hyperscale elasticity. SAP introduced a France-hosted sovereign cloud in 2025 that satisfies European privacy laws while preserving global support. Rhode Island selected Workday after calculating that subscription fees would be 35% lower than maintaining its legacy PeopleSoft stack. Savings free funds to develop citizen-facing portals, enhancing satisfaction scores, and cutting call-center costs.

Lengthy Government Procurement Cycles

Award schedules of 24-48 months erode modernization business cases. The U.S. Department of Defense cancelled the CIO-SP4 vehicle in 2025, forcing agencies to re-compete IT services and adding up to 18 months to timelines. Union County, North Carolina, expects no vendor decision until late 2026, following a two-stage RFP issued in 2025. The U.K. Public Accounts Committee reported capability gaps that fuel overruns and delay go-lives. Such inertia favors incumbents and dissuades new entrants, slowing overall market momentum.

Other drivers and restraints analyzed in the detailed report include:

- Need For Enhanced Transparency And Accountability

- Integration Of AI And Analytics For Decision Support

- Data Security And Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid ERP is advancing at a 14.80% CAGR, the fastest among deployment modes, because agencies can partition sensitive ledgers on-premises while exploiting cloud elasticity for analytics. Cloud ERP held 42% of the government ERP market size in 2025, driven by municipalities that lack data-center infrastructure. Washington State's USD 518 million One Washington program illustrates the approach, hosting payroll on state servers and procurement on Microsoft Azure Government. SAP's France sovereign cloud shows that similar models satisfy European Schrems II rulings. Orchestration complexity once discouraged hybrid rollouts, but vendors now embed low-latency connectors that keep sub-ledgers synchronized. As air-gapped government cloud regions proliferate, on-premises deployments decline except in defense and revenue agencies bound by high-security baselines.

Vendor consolidation is accelerating because only providers with dual codebases can win large solicitations. Rhode Island's Workday contract contains repatriation options if privacy regulations tighten, proof that even cloud-first buyers want exit flexibility. Australia's 2026 policy makes hybrid the default for federal departments, pushing hyperscalers to partner with local data-center operators. North American agencies benefit from 12 newly FedRAMP-authorized platforms that reduce assessment costs. The competitive lens has shifted from pure functionality to architectural optionality, rewarding suppliers that deliver seamless workload mobility across environments.

Grant management is forecast to grow at a 15.20% CAGR through 2031, eclipsing every other functional pillar as agencies administer escalating stimulus and infrastructure disbursements. Financial management retained 34% of the government ERP market share in 2025, anchoring core ledgers, yet replacement demand has plateaued. HHS Grantsolutions handles more than USD 100 billion annually, setting the compliance bar for indirect-cost validation and performance audits. REI Systems' AI scoring cuts improper payments before awards are issued, and vendors such as OpenGov and GrantWorks added milestone-based disbursement features in 2025. Transparency mandates propel citizen portals that let applicants track award status without staff intervention.

Human-capital modules ride a separate wave of demand as baby-boomer retirements squeeze public-sector recruiting pipelines. Procurement suites integrate e-invoicing mandates that France, Belgium, and Poland phase in by 2026, making PEPPOL compatibility non-negotiable. Asset-management modules are gaining traction in cities that maintain roads, water systems, and public buildings, as predictive maintenance lowers lifecycle costs. Citizen-service portals and case-management tools are blending into core ERP as vendors bundle capabilities, expanding the addressable government ERP market size without requiring separate procurement.

Geography Analysis

North America led the government ERP market with a 37% revenue share in 2025, as the Technology Modernization Fund funded federal upgrades and states such as Washington committed USD 518 million to replace 40-year-old systems. Municipal deployments, such as Miami's Oracle OPAL roll-out, underscore how transparent dashboards enhance credit ratings. Canada's Digital Adoption Program issued CAD 15,000 (USD 11,700) grants and CAD 100,000 (USD 78,000) loans to accelerate cloud migration for small governments. FedRAMP added 12 authorized platforms in 2025, slashing security assessment costs and widening supplier pools.

Asia-Pacific exhibits the fastest 12.80% CAGR through 2031, driven by India's Digital India 2.0 roadmap, China's unifying Government Service Platform, and Australia's vendor panel that cuts procurement to 12 months. Sovereignty laws require in-country hosting, spurring local data-center investment by global vendors. Thailand and Malaysia issue guidelines modeled on Australia's CPS 230, anticipating similar resilience tests. Municipal digitization in Indonesia and the Philippines is expanding the addressable government ERP market, where broadband penetration exceeds 70%.

Europe balances opportunity with regulatory friction. Schrems II, GDPR and country-specific e-invoicing mandates push agencies toward sovereign clouds. France and Germany formed a consortium with Mistral AI and SAP to deploy AI-ready ERP starting 2026, excluding U.S. hyperscalers. Belgium enforced PEPPOL compliance in January 2026, and Poland's KSeF system entered phased go-live in February 2026, compelling ERP vendors to integrate national gateways. The U.K. completed its Home Office migration yet the National Audit Office warns savings remain elusive without stronger vendor governance.

- Tyler Technologies, Inc.

- Infor, Inc.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Workday, Inc.

- CGI Inc.

- Unit4 N.V.

- Accela, Inc.

- Deltek, Inc.

- Axelor S.A.S.

- Adeaca Corp.

- OpenGov, Inc.

- IFS AB

- AccuFund, Inc.

- Appian Corporation

- ECOSIRE Global Solutions Limited

- Strada Global, LLC

- Zoho Corporation Pvt. Ltd.

- Unanet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital Transformation Mandates in Government

- 4.2.2 Cost Savings from Cloud Migration

- 4.2.3 Need for Enhanced Transparency and Accountability

- 4.2.4 Integration of AI and Analytics for Decision Support

- 4.2.5 Zero-Trust Security Requirements Driving ERP Upgrades

- 4.2.6 Stimulus-Funded Green Ledger Tracking for Sustainability Reporting

- 4.3 Market Restraints

- 4.3.1 Lengthy Government Procurement Cycles

- 4.3.2 Data Security and Sovereignty Concerns

- 4.3.3 Shortage of Public-Sector ERP Skillsets

- 4.3.4 Political Turnover Disrupting Long-Term ERP Projects

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premises ERP

- 5.1.2 Cloud ERP

- 5.1.3 Hybrid ERP

- 5.2 By Module

- 5.2.1 Financial Management

- 5.2.2 Human Capital Management

- 5.2.3 Procurement and Supply Chain

- 5.2.4 Asset and Infrastructure Management

- 5.2.5 Grant Management

- 5.2.6 Other Modules

- 5.3 By Government Level

- 5.3.1 Federal / National Government

- 5.3.2 State / Provincial Government

- 5.3.3 Local / Municipal Government

- 5.4 By Component

- 5.4.1 Software

- 5.4.2 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tyler Technologies, Inc.

- 6.4.2 Infor, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 Microsoft Corporation

- 6.4.6 Workday, Inc.

- 6.4.7 CGI Inc.

- 6.4.8 Unit4 N.V.

- 6.4.9 Accela, Inc.

- 6.4.10 Deltek, Inc.

- 6.4.11 Axelor S.A.S.

- 6.4.12 Adeaca Corp.

- 6.4.13 OpenGov, Inc.

- 6.4.14 IFS AB

- 6.4.15 AccuFund, Inc.

- 6.4.16 Appian Corporation

- 6.4.17 ECOSIRE Global Solutions Limited

- 6.4.18 Strada Global, LLC

- 6.4.19 Zoho Corporation Pvt. Ltd.

- 6.4.20 Unanet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment