PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065541

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065541

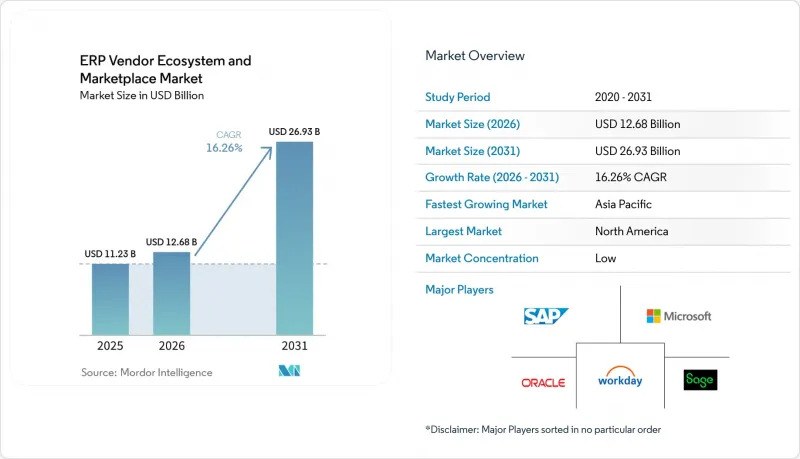

ERP Vendor Ecosystem And Marketplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the eRP vendor ecosystem and marketplace market size is projected to be USD 11.23 billion in 2025, USD 12.68 billion in 2026, and reach USD 26.93 billion by 2031, growing at a CAGR of 16.26% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and SMEs), Component (Software and Services), Industry Vertical (Manufacturing, Retail and E-Commerce, and Other Industry Verticals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global ERP Vendor Ecosystem And Marketplace Market Trends and Insights

SAP ECC 2027 End-of-Support Driving Replacement Cycles

SAP's December 2027 support cutoff for ECC 6.0 is compressing a decade of migration activity into the next 24 months, creating a surge of license churn that benefits both SAP S/4HANA Cloud and rival suites. Implementation partners grew their certified headcount by double digits in 2025, yet vacancy rates above 20% are inflating day-rates for experienced consultants, pushing enterprises toward low-code migration kits distributed through vendor marketplaces. Oracle and Workday exploited the fatigue by offering time-limited discounts and fee waivers, luring defectors that prefer greenfield deployments over brownfield conversions.

Adoption of AI-Embedded ERP Suites

Generative AI is recasting ERP from a passive system of record into an autonomous decision cockpit. Oracle's AI Agent Marketplace ships bots that reconcile invoices and predict demand, trimming finance closings from 10 days to 3 days in early pilots. Microsoft Copilot for Dynamics 365 uses natural-language prompts to automatically post journals, reducing month-end labor hours by 30%. SAP's Joule assistant lets buyers renegotiate contract terms in chat rather than e-mail threads, catalyzing a new ecosystem of prompt-engineering consultancies. Growing API traffic between ERP cores and data lakes is stressing legacy middleware, accelerating uptake of event-driven integration platforms.

High Implementation Costs and Budget Overruns

Total cost of ownership for a 500-employee manufacturer moving to SAP S/4HANA Cloud averages USD 2.8 million over five years, and deployments still overshoot budgets by up to 50% when data cleansing and change management are underestimated. In response, vendors rolled out fixed-price quick-start bundles that cap customization requests, lowering the barrier to entry yet compressing partner margins. Smaller consultancies are merging to achieve scale, and self-service migration tools are proliferating inside marketplaces to limit human billable hours.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Cloud Adoption Among Enterprises

- Demand for Integrated Supply-Chain Visibility

- Data Security and Privacy Concerns in Cloud ERP

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures held 9% of 2025 spending but are expanding at a 19.90% CAGR, the fastest among deployment models. Enterprises anchor transaction databases on-premises for latency or regulatory reasons and shuttle analytics and collaboration modules to hyperscalers, achieving a near 40% cost relief compared with pure on-premises landscapes. Vendors are pivoting: SAP's RISE service now orchestrates mixed topologies for 35% of S/4HANA clients, Oracle Cloud at Customer packages public-cloud software in an on-site appliance, and Azure Stack extends Dynamics 365 to edge factories, responses that deepen the ERP vendor ecosystem market penetration in regulated industries.

The ERP vendor ecosystem and marketplace market size advantage remains with cloud at 70.40% in 2025, yet momentum is firmly with hybrid. Marketplace sales skew heavier in hybrid estates; customers average 4.1 add-ons compared with 3.2 for pure cloud, because integration accelerators are required to bridge on-prem and cloud services.

Large organizations accounted for 62% of 2025 revenue, but the small and medium cohort is expanding at a 21.20% CAGR, nearly double the headline rate. Consumption-based pricing now lets a USD 50 million manufacturer roll out a financial core for under USD 100,000 in year one, eroding the historical barrier. Two-tier strategies intensify the shift: conglomerates keep SAP or Oracle at headquarters but provision Odoo or Acumatica at plants in Southeast Asia, reducing per-site fees by 60% and lifting ERP vendor ecosystem and marketplace market share for mid-market specialists.

The ERP vendor ecosystem and marketplace market-size tailwind for small and medium enterprises stems from modularity. Odoo ships 40 vertical packs that deploy in four weeks, and Rootstock leverages Salesforce-native objects to unite CRM and ERP without custom connectors. Large-enterprise renewals are slowing, but they remain the profit core: average contract value still tops USD 5 million, cushioning incumbents while they court smaller logos.

Geography Analysis

North America accounted for 37% of 2025 revenue, thanks to its dense partner network and rapid cloud adoption. The United States construction labor crunch is spurring adoption of mobile ERP modules that clock worker hours and materials on site, cutting back-office headcount 30%. Canada's 796 SAP-certified firms, many of which are bilingual in Quebec, support localized rollouts that comply with dual-jurisdiction tax codes. Mexico's nearshoring wave is driving demand for multi-currency consolidation between maquiladora subsidiaries and their U.S. parents.

Asia-Pacific is the fastest climber at 14.00% CAGR. Digital India forces 120,000 suppliers onto cloud ERP by 2027, and China's substitution drive toward Kingdee and Yonyou re-shapes the vendor mix even while multinationals cling to SAP global templates. Japanese mid-market manufacturers are now migrating ECC to the cloud to cut maintenance payroll by 40%. Indonesia, Vietnam, and Thailand together account for 18% CAGR as e-commerce giants spur demand for real-time inventory.

Europe contributes 28% of revenue. The European Single Electronic Format requirement, effective September 2026, obliges 12,000 listed firms to embed XBRL tags, prompting upgrades to reporting modules. Germany's Mittelstand runs two-tier deployments, and France is migrating from AS/400 legacies under ECC support deadlines. In South America, TOTVS dominates the mid-market through localized tax engines, while Vision 2030 public projects galvanize demand in the Middle East. Africa remains nascent, yet records lift from mobile-first public-sector tenders.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- IFS AB

- Unit4 N.V.

- Acumatica, Inc.

- Sage Group plc

- Syspro (Pty) Ltd.

- QAD Inc.

- Deltek, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

- Rootstock Software, Inc.

- Priority Software Ltd.

- Workday, Inc.

- Odoo SA

- Ramco Systems Limited

- TOTVS S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Cloud Adoption Among Enterprises

- 4.2.2 Adoption of AI-Embedded ERP Suites

- 4.2.3 Demand for Integrated Supply-Chain Visibility

- 4.2.4 Regulatory Mandates for Real-Time Financial Reporting

- 4.2.5 SAP ECC 2027 End-of-Support Driving Replacement Cycles

- 4.2.6 Two-Tier ERP Strategies Fueling Niche Vendor Growth

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs and Budget Overruns

- 4.3.2 Data Security and Privacy Concerns in Cloud ERP

- 4.3.3 Shortage of ERP-Qualified Implementation Talent

- 4.3.4 Interoperability Challenges in Composable Architectures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

- 4.9 Analysis on Ecosystem Type

- 4.9.1 Vendor-native marketplaces (SAP Store, Oracle Cloud Marketplace)

- 4.9.2 Partner ecosystems (system integrators, ISVs)

- 4.9.3 Open ecosystems (API-based, multi-ERP integrations)

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Component

- 5.3.1 Software Modules

- 5.3.2 Services

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Banking, Financial Services and Insurance

- 5.4.5 Professional Services

- 5.4.6 Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 IFS AB

- 6.4.7 Unit4 N.V.

- 6.4.8 Acumatica, Inc.

- 6.4.9 Sage Group plc

- 6.4.10 Syspro (Pty) Ltd.

- 6.4.11 QAD Inc.

- 6.4.12 Deltek, Inc.

- 6.4.13 Aptean, Inc.

- 6.4.14 Plex Systems, Inc.

- 6.4.15 Rootstock Software, Inc.

- 6.4.16 Priority Software Ltd.

- 6.4.17 Workday, Inc.

- 6.4.18 Odoo SA

- 6.4.19 Ramco Systems Limited

- 6.4.20 TOTVS S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment