PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065557

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065557

Enterprise Resource Planning Customization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

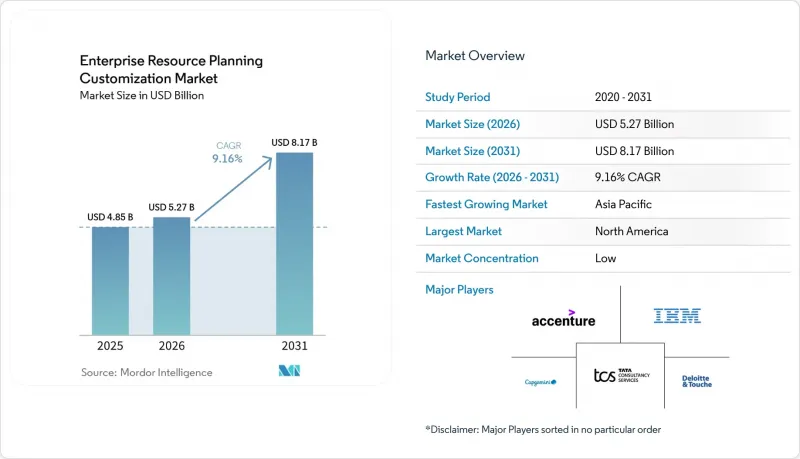

According to Mordor Intelligence, the enterprise resource planning customization services market size is projected to be USD 4.85 billion in 2025, USD 5.27 billion in 2026, and reach USD 8.17 billion by 2031, growing at a CAGR of 9.16% from 2026 to 2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-Use Industry (Manufacturing, Retail and E-Commerce, Banking, Financial Services and Insurance (BFSI), Healthcare, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Customization Market Trends and Insights

Rising Demand for Industry-Specific ERP Modules

Enterprises are moving away from generic suites toward vertical capabilities that embed shop-floor telemetry, regulatory reporting engines, and patient data workflows. Manufacturing adopters seek predictive maintenance and supply-chain visibility, while healthcare providers require seamless interoperability with electronic health records. Financial institutions demand real-time risk dashboards and compliance automation. This push toward specialization accelerates the adoption of modular, API-first designs that keep the ERP core clean and shift heavy customization to loosely coupled extensions.

Acceleration of Cloud-First Digital Transformation Strategies

Cloud-first mandates convert capital expenditure into operating expenditure, enable evergreen upgrades, and shorten deployment cycles. Government agencies and large enterprises increasingly stipulate 99.95% service-level agreements, bundled security tooling, and unified identity management, prompting partnerships between hyperscalers and ERP vendors. As enterprises offload infrastructure management, customization requirements pivot toward integration governance, FinOps visibility, and proactive regression testing for biannual cloud releases.

High Switching Costs Limiting Vendor Migration

Organizations with heavily customized on-premises landscapes face data-egress fees, reimplementation costs, and potential business disruption. The December 2027 end-of-support for a major ERP release magnifies urgency, but talent scarcity and consulting rate inflation complicate large-scale moves. Enterprises are therefore cataloging legacy extensions, quantifying realized benefits, and choosing to retire, retrofit, or rebuild only the highest-value custom objects.

Other drivers and restraints analyzed in the detailed report include:

- Growing SME Adoption of Subscription-Based ERP Suites

- Demand for Post-Implementation Hyper-Care Services

- Shortage of Certified ERP Functional Consultants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 59% of the Enterprise Resource Planning Customization Services market share in 2025 and are on track for a 14.10% CAGR through 2031. The shift reflects demand for evergreen functionality, built-in AI, and consumption-based pricing that lowers total cost of ownership. Enterprises integrate low-code platforms within cloud ecosystems, trimming development cycles by up to 70% and freeing scarce developer capacity. However, hybrid estates persist where latency-sensitive operations or data-sovereignty mandates require local hosting, adding integration overhead.

Across industries, organizations adopting cloud ERP treat custom code as a liability, pushing extensions to platform-as-a-service layers that preserve upgrade paths. This approach reduces technical debt but introduces multi-vendor licensing complexity, prompting the rise of FinOps centers that forecast, monitor, and optimize spend. The Enterprise Resource Planning Customization Services market size for cloud-related services is therefore expanding faster than for on-premise work, even as clients demand stricter service-level guarantees and automated regression testing ahead of each biannual release.

Geography Analysis

North America accounted for 35.70% of the Enterprise Resource Planning Customization Services market in 2025, supported by mature cloud adoption, stringent federal modernization mandates, and a dense ecosystem of global systems integrators. Federal agencies evaluate business-case economics, enforce shared-responsibility security models, and require continuous monitoring of cloud-hosted ERP systems. Contract wins surrounding national health-record modernization and defense logistics confirm the region's appetite for large-scale, AI-enabled customizations.

Asia-Pacific is projected to expand at a 14.80% CAGR to 2031 as sovereign-cloud policies in Australia, India, and Singapore spur localized hosting, encryption, and compliance tooling. Rapid growth in public-cloud revenue, manufacturing offshoring, and digital banking adoption fuels spending on tailored workflows and integration accelerators. Nevertheless, legacy entanglement and specialist talent shortages often trigger hybrid rollouts that phase core-system migrations across multiple budget cycles.

Europe shows steady, if moderated, growth driven by GDPR alignment, industrial automation, and impending end-of-support deadlines for incumbent ERP releases. A significant consultant shortfall inflates labor rates and lengthens project timelines, especially in Germany, France, and the United Kingdom. Northern markets emphasize cloud-native extensions and analytics, while Southern Europe leans on phased, budget-constrained transformations. Emerging regions such as South America, the Middle East, and Africa generate incremental demand, though infrastructure gaps and currency volatility temper near-term scale.

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- International Business Machines Corporation

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- Atos SE

- DXC Technology Company

- Tech Mahindra Limited

- NTT DATA Corporation

- CGI Inc.

- Larsen and Toubro Infotech Ltd (LTI Mindtree)

- EPAM Systems Inc.

- Rackspace Technology Inc.

- Hitachi Consulting Co., Ltd.

- Syntax Systems Ltd.

- Vision33 Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Industry-Specific ERP Modules

- 4.2.2 Acceleration of Cloud-First Digital Transformation Strategies

- 4.2.3 Growing SME Adoption of Subscription-Based ERP Suites

- 4.2.4 Demand for Post-Implementation Hyper-Care Services (Under-the-Radar)

- 4.2.5 Shift Toward Composable ERP Architecture (Under-the-Radar)

- 4.2.6 Increasing Use of Low-Code Platforms for Tailored Workflows (Under-the-Radar)

- 4.3 Market Restraints

- 4.3.1 High Switching Costs Limiting Vendor Migration

- 4.3.2 Shortage of Certified ERP Functional Consultants

- 4.3.3 Rising Concerns Around Data Residency Compliance (Under-the-Radar)

- 4.3.4 Technical Debt From Legacy Customizations (Under-the-Radar)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By End-Use Industry

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-Commerce

- 5.3.3 Banking, Financial Services and Insurance (BFSI)

- 5.3.4 Healthcare

- 5.3.5 Information Technology and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-Use Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Kenya

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 Capgemini SE

- 6.4.4 Tata Consultancy Services Limited

- 6.4.5 Infosys Limited

- 6.4.6 International Business Machines Corporation

- 6.4.7 Cognizant Technology Solutions Corporation

- 6.4.8 Wipro Limited

- 6.4.9 HCL Technologies Limited

- 6.4.10 Atos SE

- 6.4.11 DXC Technology Company

- 6.4.12 Tech Mahindra Limited

- 6.4.13 NTT DATA Corporation

- 6.4.14 CGI Inc.

- 6.4.15 Larsen and Toubro Infotech Ltd (LTI Mindtree)

- 6.4.16 EPAM Systems Inc.

- 6.4.17 Rackspace Technology Inc.

- 6.4.18 Hitachi Consulting Co., Ltd.

- 6.4.19 Syntax Systems Ltd.

- 6.4.20 Vision33 Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment