PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065567

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065567

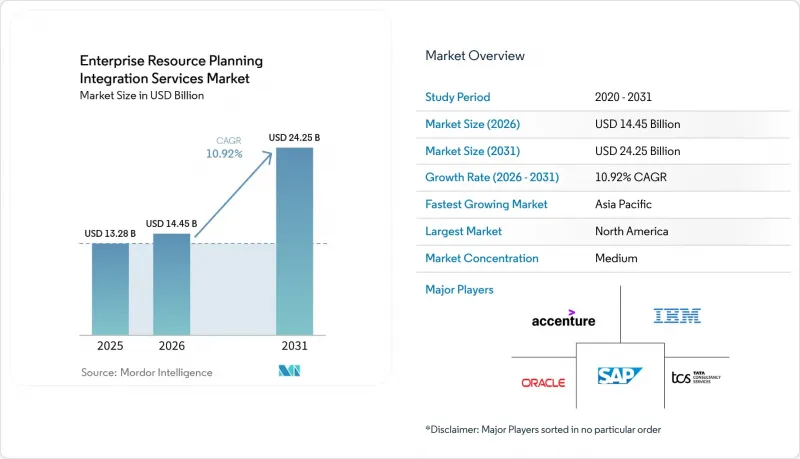

Enterprise Resource Planning Integration Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the eRP integration services market size is projected to be USD 13.28 billion in 2025, USD 14.45 billion in 2026, and reach USD 24.25 billion by 2031, growing at a CAGR of 10.92% from 2026 to 2031.

This report is Segmented by Service Type (Application Integration, Data Integration, Process Integration, and Other Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (SMEs and Large Enterprises), Industry Vertical (Manufacturing, BFSI, Retail and Ecommerce, Healthcare, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Integration Services Market Trends and Insights

Rapid Adoption of Cloud-Based ERP Systems

Cloud ERP deployments are displacing monolithic middleware with distributed integration fabrics that span multiple hyperscalers and private data centers. SAP Integration Suite connected 2.5 million systems as of February 2026, and 85% of those links involved non-SAP applications, signaling a decisive move toward open API gateways. Microsoft Azure's 99.95% service-level commitment for SAP private editions further reduces the perceived need for on-premises high-availability clusters. Odoo reported that cloud and hybrid setups formed 83% of new ERP deployments in 2025, mirroring the broader pivot to subscription economics. IBM's RISE with SAP on Power Virtual Server shaved 15%-25% off migration timelines by bundling storage, networking, and backup, thereby tightening the window for third-party integrators to sell custom connectors. As more production workloads move to the public cloud, the ERP integration services market is evolving toward pre-packaged adapters, policy-driven routing, and low-code orchestration to shorten time-to-value.

Need for Real-Time Data Synchronization Across Heterogeneous Systems

Overnight batch ETL cannot support dynamic pricing, real-time inventory allocation, or instant payments. Oracle embedded J. P. Morgan's cross-border rails into Oracle Cloud ERP in 2025, eliminating 24-hour reconciliation delays for 160 countries. SAP-to-Snowflake Change Data Capture streams cut analytical latency from hours to seconds. Manufacturers processing 200 GB of sensor data daily now route only anomaly events to cloud ERP via sub-second brokers. More than 80 countries already operate instant-payment schemes, and ISO 20022 compliance is now table-stakes for integration vendors. These developments keep the ERP integration services market on a steady growth path as enterprises re-architect for streaming data.

Complexity of Legacy ERP Customizations

Roughly 21,000 SAP ECC installations, 61% of the installed base, remain unmigrated, with mainstream support ending in December 2027. Custom ABAP code and undocumented bolt-ons devour up to half of migration budgets, and consulting rates are set to rise as the deadline nears. Only 30% of organizations were fully live on SAP S/4HANA Cloud in 2025, indicating that the bulk of integration workloads will compress into a two-year window. As backlogs swell, the ERP integration services industry faces execution risk and potential project delays.

Other drivers and restraints analyzed in the detailed report include:

- Increasing API-First Digital Transformation Strategies

- Growing Popularity of iPaaS Platforms Among SMEs

- High Total Cost of Ownership for Large Integration Projects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Application integration accounted for 34.20% of 2025 revenue, reflecting the entrenched web of connectors that tie ERP to CRM, supply chain, and HCM suites. Yet API management is projected to log a 15.40% CAGR over 2026-2031, the fastest within the service stack, as event-driven architectures supersede nightly ETL and embedded-finance use cases call for governed external APIs. The ERP integration services market registers accelerating demand for multi-protocol gateways that wrap REST, SOAP, EDIFACT, and GraphQL under a single policy layer, ensuring consistent authentication and rate controls. Vendors now auto-generate OpenAPI contracts, maintain version lineage, and monetize high-value endpoints through subscription billing.

Data-integration services remain core for analytical workloads, streaming CDC feeds into Snowflake and BigQuery in real time. Process-integration consultancies lean on low-code orchestrators and robotic process automation to knit end-to-end workstreams such as order-to-cash without swivel-chair tasks. B2B and EDI integration still rides demand from aerospace and consumer goods, where ANSI X12 and EDIFACT remain contractual bedrock. Cloud integration brokerage outsources connector maintenance and security patching to providers, freeing enterprise IT from upkeep. As containerized microservices proliferate, API management will command a larger share of the ERP integration services market size through 2031.

Cloud deployments accounted for 57.50% of 2025 revenue, driven by hyperscaler bundles that combine infrastructure, licenses, and native integration. IBM's RISE with SAP on Power Virtual Server posted 30% infrastructure savings by collapsing middleware layers. Yet hybrid configurations are expanding at a 14.00% CAGR, the highest among deployment options, as European and Asian data-residency mandates block certain records from leaving national borders. GDPR Article 48 forbids unsanctioned cross-border transfers, encouraging multinationals to keep master data on-premises while sending analytics to the cloud.

Hybrid topologies, therefore, require secure message buses, dual-region replication, and tenant-aware encryption. IBM X-Force cataloged 16 million devices infected by infostealer malware in 2025, with MuleSoft Anypoint and Microsoft Entra Connect often serving as breach entry points. Only 62% of surveyed SAP cloud users adhere to recommended security hardening, leaving plaintext keys in configs. Integration platforms must therefore bundle secrets management and audit logging that meet ISO 27001 and SOC 2 Type II requirements. Sovereignty and latency constraints ensure that the ERP integration services market share tied to hybrid topologies will continue to rise.

Geography Analysis

North America accounted for 42.30% of 2025 revenue, driven by mature ERP footprints in the United States and Canada that require ongoing integration as new SaaS modules roll in. AI-assisted workloads, such as Microsoft's Jupyter Notebook Copilot for voice queries, accelerate the adoption of governed APIs, shortening user-training cycles. Tougher HIPAA penalties keep healthcare IT budgets flowing toward secure integration fabrics, cushioning any post-migration slowdown. Hence, North America remains a robust contributor to the ERP integration services market size.

Asia-Pacific is projected to post a 14.90% CAGR through 2031, the fastest regional rate. Deferred SAP S/4HANA migrations in China, India, Japan, and South Korea will compress into 2027-2029 as SAP ECC leaves mainstream support. IBM and SAP's Power Virtual Server migrations reduce timelines by up to 25%. China's Data Security Law forces local replication of sensitive records, promoting hybrid integration proxies. Consequently, the ERP integration services market share tied to Asia-Pacific will surge as deadlines loom.

Europe balances entrenched customizations with GDPR fidelity. Article 48's cross-border restrictions promote sovereign-cloud offerings such as SAP Sovereign Cloud. South America and the Middle East and Africa remain smaller but promising. Brazil and Saudi Arabia lead government digitization, and Mexico's USMCA membership accelerates cross-border supply-chain integrations that need real-time ERP connectors. Together, geographic diversification cushions the global ERP integration services market against localized shocks.

- Accenture plc

- IBM Corporation

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infosys Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Deloitte Touche Tohmatsu Limited

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- MuleSoft LLC

- Boomi LP

- Celigo Inc.

- Jitterbit Inc.

- SnapLogic Inc.

- Workato Inc.

- Software AG

- Seeburger AG

- Infor Inc.

- Epicor Software Corporation

- IFS AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Based ERP Systems

- 4.2.2 Need for Real-Time Data Synchronization Across Heterogeneous Systems

- 4.2.3 Increasing API-First Digital Transformation Strategies

- 4.2.4 Growing Popularity of iPaaS Platforms Among SMEs

- 4.2.5 Emergence of Low-Code/No-Code Integration Tools

- 4.2.6 Compliance Mandates Driving Data Integration in Regulated Industries

- 4.3 Market Restraints

- 4.3.1 Complexity of Legacy ERP Customizations

- 4.3.2 High Total Cost of Ownership for Large Integration Projects

- 4.3.3 Data Security and Governance Concerns in Hybrid Environments

- 4.3.4 Shortage of Skilled Integration Specialists

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Application Integration

- 5.1.2 Data Integration

- 5.1.3 Process Integration

- 5.1.4 API Management

- 5.1.5 B2B/EDI Integration

- 5.1.6 Cloud Integration Brokerage

- 5.1.7 Other Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 BFSI

- 5.4.3 Retail and Ecommerce

- 5.4.4 Healthcare

- 5.4.5 IT and Telecom

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Microsoft Corporation

- 6.4.6 Infosys Limited

- 6.4.7 Capgemini SE

- 6.4.8 Tata Consultancy Services Limited

- 6.4.9 Deloitte Touche Tohmatsu Limited

- 6.4.10 Cognizant Technology Solutions Corporation

- 6.4.11 Wipro Limited

- 6.4.12 HCL Technologies Limited

- 6.4.13 MuleSoft LLC

- 6.4.14 Boomi LP

- 6.4.15 Celigo Inc.

- 6.4.16 Jitterbit Inc.

- 6.4.17 SnapLogic Inc.

- 6.4.18 Workato Inc.

- 6.4.19 Software AG

- 6.4.20 Seeburger AG

- 6.4.21 Infor Inc.

- 6.4.22 Epicor Software Corporation

- 6.4.23 IFS AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment