PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063413

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063413

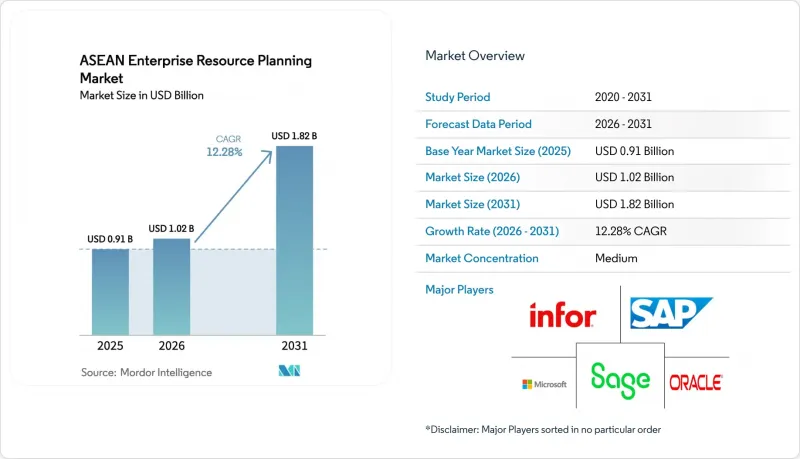

ASEAN Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aSEAN enterprise resource planning market size is expected to grow from USD 0.91 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at a 12.28% CAGR over 2026-2031.

This report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

ASEAN Enterprise Resource Planning Market Trends and Insights

Cloud Migration Acceleration Among ASEAN SMEs

Small and medium enterprises are shifting to cloud-native suites to avoid capital expenditure on servers, scale modules incrementally, and keep statutory requirements up to date without manual patching. Digital-native retailers and logistics firms founded after 2024 bypassed desktop accounting entirely, choosing subscription packages that bundle inventory, payroll, and e-invoicing. Subsidy programs in Malaysia and Indonesia routinely offset up to half of first-year fees, compressing payback periods to under 18 months. Vendors that offer free trials and localized tax engines win conversions quickly, and quarterly automatic updates ensure compliance with rapid regulatory changes, reducing audit-related downtime.

Rising Government Digital Economy Initiatives

Regional policy frameworks now treat ERP software as foundational infrastructure. Preferential procurement scoring for suppliers connected via API to government portals and low-interest transformation loans pressure manufacturers, healthcare providers, and service firms to upgrade. Thailand 4.0 incentives, Indonesia's co-funding roadmap, and Singapore's Smart Nation 2.0 collectively underwrite upgrade costs, making ERP adoption a prerequisite for accessing trade-finance, tax holidays, or fast-track licensing. Enforcement mechanisms, such as real-time invoice or e-tax submission, convert policy into immediate operating requirements rather than aspirational goals.

Data Sovereignty and Localization Regulations

Mandates in Indonesia, Thailand, and Vietnam require local data storage for citizen or sensitive records, forcing ERP vendors to operate domestic cloud regions or hybrid topologies. Indonesia's Government Regulation 71/2019 mandates that all electronic systems handling citizen data must store and process information within the country, effectively prohibiting pure public-cloud ERP deployments for government contractors, healthcare providers, and financial institutions unless vendors establish in-country data centers.Additional audit, infrastructure, and legal costs inflate subscription pricing by up to one-quarter and slow feature parity relative to markets without residency restrictions. Enterprises that cannot justify the expense of private cloud defer modernization, preserving a pool of on-premises systems that drags overall growth.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI and Analytics into ERP Suites

- Adoption of Modular Two-Tier ERP for Subsidiaries

- Shortage of ERP Implementation Talent in ASEAN

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Two-tier architectures captured 13.08% growth and represent the fastest-expanding segment within the ASEAN enterprise resource planning market. These architectures enable headquarters instances of SAP or Oracle to synchronize nightly with subsidiary platforms such as NetSuite or Business Central. This synchronization eliminates manual currency translation errors, streamlines financial reporting, and reduces consolidation cycles from weeks to just a few days. Cloud-native suites accounted for 41.12% of the installed base in 2025, while mobile-first platforms cater to logistics and field-service operators who require seamless smartphone access for their operations.

Localized compliance requirements significantly drive the adoption of this architecture. The presence of separate e-tax portals, payroll statutes, and invoice formats across five key ASEAN markets makes it economically unfeasible to customize a single global instance. Instead, subsidiaries can implement localized platforms and go live within 3 months, with support from regional partners well-versed in domestic regulations. Meanwhile, headquarters retains centralized control over group reporting and financial oversight. Consequently, two-tier adoption has become a cornerstone of hybrid rollouts, solidifying its role in the growth and evolution of the market.

Human-capital suites will expand at 13.28% through 2031, eclipsing finance as enterprises seek accurate payroll, leave, and benefits processing across 11 statutory landscapes. The finance and accounting segment accounts for 35.16% of spend, but growth moderates as many firms have already automated core ledgers. Fragmented social-security rules expose firms to penalties when calculations go awry, turning payroll accuracy into a board-level risk. Unified cloud payroll covering Indonesia, Malaysia, Thailand, Singapore, the Philippines, and Vietnam reduces manual filing errors by over one-third. In turn, policy-driven complexities in overtime and severance accelerate demand for modern HCM suites in the ASEAN enterprise resource planning market.

The market is divided into finance, human resources, supply chain management, manufacturing, procurement, and customer relationship management (CRM). Finance modules continue to serve as the foundation of ERP implementations, as they play a critical role in financial reporting, budgeting, taxation, and regulatory compliance. However, supply chain and procurement functions are seeing increased adoption as businesses in the region expand cross-border trade and seek enhanced visibility into supplier networks, inventory management, and logistics. At the same time, CRM modules are gaining traction as companies prioritize customer engagement, sales forecasting, and service management.

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 N.V.

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO (Pty) Ltd.

- Acumatica Inc.

- Ramco Systems Ltd.

- HashMicro Pte. Ltd.

- Epicor Software Corporation

- QAD Inc.

- Deskera Holdings Ltd.

- SunFish DataOn Philippins Inc.

- Zoho Corporation Pvt. Ltd.

- ECOUNT Co., Ltd.

- Highnix Pte. Ltd.

- HashMicro Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration Acceleration among ASEAN SMEs

- 4.2.2 Rising Government Digital Economy Initiatives

- 4.2.3 Integration of AI and Analytics into ERP Suites

- 4.2.4 Adoption of Modular Two-Tier ERP for Subsidiaries

- 4.2.5 Growing Mobile Workforce Demanding Anytime Access

- 4.2.6 Surge in ESG Reporting Needs Driving ERP Upgrades

- 4.3 Market Restraints

- 4.3.1 Data Sovereignty and Localization Regulations

- 4.3.2 Shortage of ERP Implementation Talent in ASEAN

- 4.3.3 Legacy System Integration Complexities

- 4.3.4 High Total Cost of Ownership for SMEs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 Singapore

- 5.6.2 Thailand

- 5.6.3 Malaysia

- 5.6.4 Indonesia

- 5.6.5 Philippines

- 5.6.6 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Unit4 N.V.

- 6.4.5 IFS AB

- 6.4.6 Infor Inc.

- 6.4.7 Sage Group Plc

- 6.4.8 Workday Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Acumatica Inc.

- 6.4.11 Ramco Systems Ltd.

- 6.4.12 HashMicro Pte. Ltd.

- 6.4.13 Epicor Software Corporation

- 6.4.14 QAD Inc.

- 6.4.15 Deskera Holdings Ltd.

- 6.4.16 SunFish DataOn Philippins Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 ECOUNT Co., Ltd.

- 6.4.19 Highnix Pte. Ltd.

- 6.4.20 HashMicro Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment