PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063423

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063423

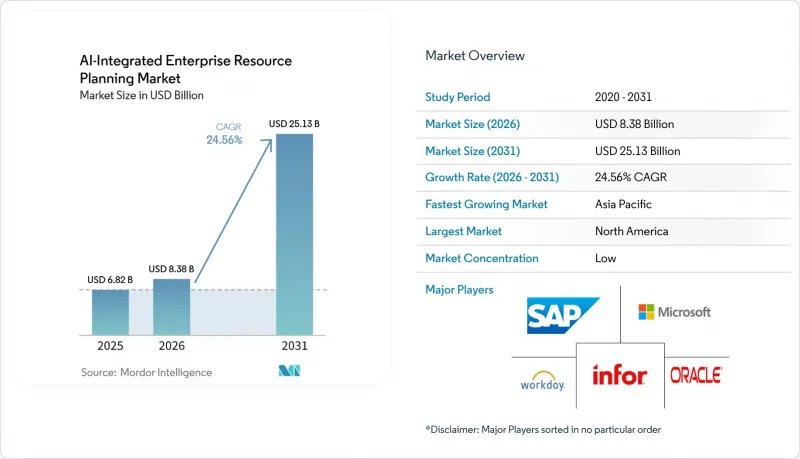

AI-Integrated Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI-integrated enterprise resource planning market size is expected to increase from USD 8.38 billion in 2026 to reach USD 25.13 billion by 2031, growing at a CAGR of 24.56% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software and Services), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), Business Function (Finance and Accounting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Integrated Enterprise Resource Planning Market Trends and Insights

Accelerated Migration to Cloud-Native ERP With Embedded AI

Global corporations typically maintain a single instance of SAP S/4HANA or Oracle Fusion at their headquarters while equipping subsidiaries with lighter, more agile cloud suites such as NetSuite or Microsoft Dynamics 365 Business Central. This hub-and-spoke architecture balances global financial consolidation with localized operational flexibility. Pre-configured templates streamline deployment by packaging manufacturing, distribution, or service workflows, enabling regional entities to achieve go-live in less than 4 months. This is a significant improvement over the year or more typically required for a full-scale rollout. Additionally, nightly synchronization ensures compliance with transfer pricing regulations, while local teams retain the ability to modify procurement rules without triggering corporate-level change control processes. This approach allows organizations to maintain centralized oversight while fostering adaptability at the regional level.

Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

Manufacturers and retailers are increasingly integrating external signals such as port-congestion updates, extreme-weather alerts, and geopolitical indices directly into their planning engines to enhance operational efficiency. These predictive models enable businesses to proactively reschedule production, reroute freight, and rebalance safety stock, preventing shortages from escalating into larger disruptions. For instance, automotive and consumer-electronics companies that have implemented real-time visibility platforms connected to AI-integrated enterprise resource planning market deployments have successfully reduced planning cycles by one-third. Additionally, these companies have significantly reduced expedited shipping costs, demonstrating the tangible benefits of such integrations. This emerging practice is transforming traditional dashboards from merely providing descriptive views into advanced prescriptive engines capable of autonomously executing corrective actions, thereby streamlining decision-making processes and improving overall supply chain resilience.

High Data-Security and Compliance Concerns in Regulated Industries

Healthcare and banking entities are required to demonstrate that training data remains confined within approved jurisdictions and that audit trails comply with regulations such as GDPR, HIPAA, or SOX. This ensures that sensitive data is handled securely and transparently. However, to address regulatory concerns, many organizations implement parallel manual reviews alongside AI-generated journal entries. These reviews are intended to build trust with regulators but often undermine the efficiency gains promised by AI automation. To overcome these challenges, emerging federated-learning techniques offer a potential solution by enabling local model training without transferring sensitive data across jurisdictions. Despite its promise, the adoption of federated learning at scale remains limited, as few enterprise suites have successfully operationalized it.

Other drivers and restraints analyzed in the detailed report include:

- Two-Tier ERP Adoption Among Multinational Subsidiaries

- AI-Driven Reduction in Implementation Time and Cost

- Integration Complexity With Legacy and Edge Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises installations retained 72.13% of 2025 revenue because regulated enterprises keep sensitive records within corporate firewalls and require millisecond-level response times for shop-floor equipment. The AI-integrated enterprise resource planning market size for cloud deployments, however, is projected to climb at a 25.16% CAGR to 2031. Vendors reserve the most advanced copilots for SaaS editions, so financial controllers often champion gradual module migrations even when core ledgers stay on-site.

Hybrid approaches combine local data lakes with cloud analytics sandboxes. Asian organizations in countries with stringent data-residency laws increasingly store personal data on sovereign clouds while pushing anonymized datasets to global regions for AI training. As more proofs of concept succeed, boardrooms become more comfortable staging sensitive workloads off-premises during non-business hours, accelerating broader migration waves across the AI-integrated enterprise resource planning market.

Large manufacturers use programmable logic controllers (PLCs) and supervisory control and data acquisition (SCADA) systems that generate data in proprietary formats. These systems are critical for automating and monitoring industrial processes, but the data they produce often requires translation layers to be compatible with enterprise resource planning (ERP) systems. These translation layers, frequently custom-coded, are essential for enabling predictive maintenance agents to seamlessly integrate with ERP work-order modules. However, the development and maintenance of these layers can significantly increase integration budgets, often surpassing the costs of the core software itself. Additionally, each new interface introduced into the system poses a potential cybersecurity risk, as vulnerabilities can arise from poorly secured connections or outdated protocols.

To address these challenges, low-code integration hubs have emerged as a solution to simplify connecting disparate systems. These hubs reduce the need for extensive custom coding, allowing businesses to streamline integration efforts and lower associated costs. However, while they alleviate some of the pain points, they also come with their own set of challenges, including additional licensing fees and the need for robust governance frameworks to ensure compliance and security. As a result, manufacturers must carefully evaluate the trade-offs between traditional custom-coded solutions and low-code platforms to optimize their operations while mitigating risks.

Geography Analysis

North America accounted for 37.89% of 2025 revenue, driven by public-sector modernizations and aggressive cloud migrations across retail and healthcare. United States federal programs alone represent multi-billion-dollar deals that span a decade. Canadian cloud-first procurement rules further expand the addressable AI-integrated enterprise resource planning market and fuel consulting engagements that localize data-residency controls. Mexico's nearshoring boom entices automotive suppliers to adopt two-tier architectures linking local plants with U.S. headquarters.

Asia-Pacific is set to record a 25.56% CAGR from 2026-2031, the fastest pace worldwide. Japanese subsidies help small manufacturers offset license fees, Indonesian data-localization laws push global vendors to open domestic regions, and Indian tax-digitization mandates accelerate mid-market upgrades. Chinese regulations require in-country data centers, steering deals to joint ventures between global publishers and domestic hyperscalers. Australia and South Korea emphasize cybersecurity and disaster recovery certifications, further expanding regional budgets.

Europe grows more slowly because fragmented compliance rules prolong decision cycles. The United Kingdom's multi-department SAP migration illustrates the complexity of cross-agency programs. German manufacturers add AI agents to track carbon footprints in line with new border-adjustment mechanisms, while French health systems adopt cloud ERP only after local hosting becomes available. Spain and Italy accelerate e-invoicing upgrades, and the Nordics emphasize green-data-center sourcing. South America, the Middle East, and Africa collectively represent a smaller but fast-closing gap, especially where governments introduce real-time e-invoice mandates that require embedded tax logic.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Sage Group Plc

- Infor Inc.

- Epicor Software Corporation

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Odoo SA

- QAD Inc.

- Ramco Systems Limited

- Plex Systems, Inc.

- SYSPRO (Pty) Ltd.

- Rootstok Software

- Deltek, Inc.

- Zoho Corporation Pvt. Ltd.

- IFS AB

- Unit4 N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Migration to Cloud-Native ERP with Embedded AI

- 4.2.2 Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

- 4.2.3 Two-Tier ERP Adoption among Multinational Subsidiaries

- 4.2.4 AI-Driven Reduction in Implementation Time and Cost

- 4.2.5 Mid-Market Appetite for Composable Low-Code ERP Modules

- 4.2.6 Government Digital Transformation Mandates and Incentives

- 4.3 Market Restraints

- 4.3.1 High Data-Security and Compliance Concerns in Regulated Industries

- 4.3.2 Integration Complexity with Legacy and Edge Systems

- 4.3.3 Shortage of AI-Skilled ERP Implementation Talent

- 4.3.4 Vendor Lock-In and Escalating Subscription Costs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Retail and Distribution

- 5.4.5 IT and Telecom

- 5.4.6 Government and Utilities

- 5.4.7 Other Industry Verticals

- 5.5 By Business Function

- 5.5.1 Finance and Accounting

- 5.5.2 Human Resource Management

- 5.5.3 Supply Chain and Logistics

- 5.5.4 Customer Relationship Management

- 5.5.5 Inventory and Work Order Management

- 5.5.6 Other Business Functions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.2.4 Saudi Arabia

- 5.6.5.2.5 Rest of Middle East

- 5.6.5.3 Africa

- 5.6.5.3.1 South Africa

- 5.6.5.3.2 Egypt

- 5.6.5.3.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Sage Group Plc

- 6.4.5 Infor Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 Acumatica, Inc.

- 6.4.8 Workday, Inc.

- 6.4.9 Priority Software Ltd.

- 6.4.10 Odoo SA

- 6.4.11 QAD Inc.

- 6.4.12 Ramco Systems Limited

- 6.4.13 Plex Systems, Inc.

- 6.4.14 SYSPRO (Pty) Ltd.

- 6.4.15 Rootstok Software

- 6.4.16 Deltek, Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 IFS AB

- 6.4.19 Unit4 N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment