PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063430

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063430

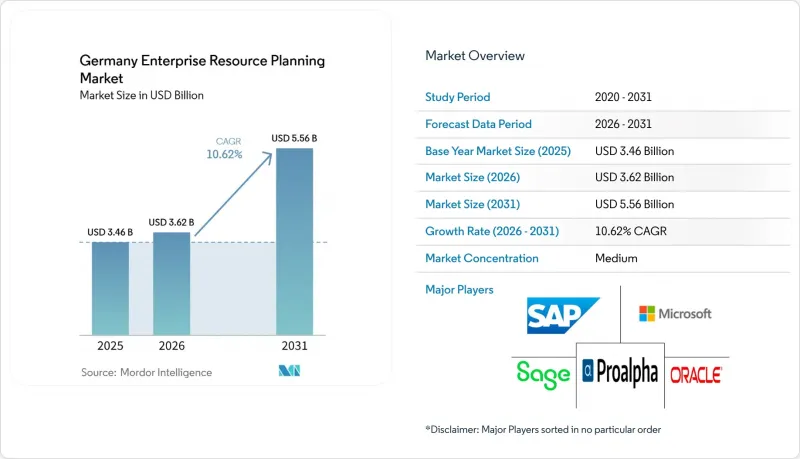

Germany Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany enterprise resource planning market size is expected to increase from USD 3.46 billion in 2025 to USD 3.62 billion in 2026 and reach USD 5.56 billion by 2031, growing at a CAGR of 6.58% over 2026-2031.

This report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Enterprise Resource Planning Market Trends and Insights

Accelerated Cloud Adoption Among German Mid-Market Firms

Mittelstand companies have replaced two-thirds of their core systems within two years, favoring cloud-native and hybrid models that align with vendor roadmaps and support remote work. A 2025 BITMi survey showed 82% of firms planning higher IT budgets for 2026, with 53% earmarked for cloud infrastructure. The SAP-Microsoft 99.95% SLA for Cloud ERP Private on Azure exemplifies offerings that de-risk uptime and integrate with Copilot and Teams. Yet many buyers still prefer private or sovereign clouds to avoid extraterritorial data-access laws, prompting vendors such as proALPHA to release hybrid options that keep MES on-premise while moving CRM to SaaS.

Stringent Data Protection Regulations Driving Demand for Compliant ERP

The General Data Protection Regulation, the German Federal Data Protection Act, and the EU Data Act mandate open interfaces, standardized export formats, and the abolition of switching fees by 2027. 42% of enterprises cite data protection as a barrier to public cloud adoption. SAP and Microsoft responded by partnering with Delos Cloud GmbH, which hosts workloads in German-controlled data centers to mitigate CLOUD Act concerns. For banks, the Digital Operational Resilience Act extends compliance to third-party risk management, forcing rigorous audits of ERP providers.

Legacy System Complexity and High Migration Costs

Currently, 71% of SAP customers continue to operate on ECC HCM, even as the May 2026 migration deadline approaches. This trend highlights the challenges posed by payroll customizations, which often make rapid re-implementation difficult. For instance, a mid-sized manufacturer is facing migration costs exceeding EUR 10 million (USD 11.3 million) and project timelines extending up to 36 months. While third-party maintenance services can provide a temporary solution by deferring upgrades, they also hinder innovation. This approach often results in organizations becoming reliant on outdated systems, which in turn locks valuable technical talent into managing legacy technical debt rather than focusing on forward-looking initiatives.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Push Within German Manufacturing

- Rising Need for Real-Time Supply Chain Visibility

- Stringent Data Residency Concerns Limiting Public Cloud Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Two-tier deployments are forecast to grow at 15.12% annually through 2031, while the Cloud-Native Suite segment captured the largest share of 48.21%. As multinational Mittelstand firms overlay lightweight regional instances atop core S/4HANA or Oracle ledgers. The Germany enterprise resource planning market size for two-tier architecture is projected to expand faster than any other segment, reflecting statutory reporting demands and cost discipline. ProALPHA's hybrid-ready 9.5 release lets manufacturers keep latency-sensitive MES on-premises while syncing CRM to the cloud, preserving works council requirements without forfeiting global visibility. Vendors able to automate data replication and identity management across tiers will outpace competitors.

Second-order impacts include growing interface complexity and rising demand for unified admin consoles. Vendors such as proALPHA now bundle single sign-on (SSO) and multi-factor authentication (MFA) to address fragmentation and improve the user experience. As the EU Data Act enforces the use of open APIs, customers are increasingly expecting a seamless transition between edge instances and the core systems. This shift is driving the accelerated adoption of advanced integration patterns, such as message-queue systems and event-streaming architectures, which enable real-time data exchange and improved operational efficiency.

Human capital management is projected to log a 13.28% CAGR; however, finance and accounting generated 34.97% over the forecast period. As organizations accelerate efforts to meet SAP's H4S4 deadline. The Germany enterprise resource planning market share for HCM is expected to grow significantly, as cloud payroll adoption remains low due to the complexities of collective-bargaining rules. While finance remains the core function, the growing integration of embedded analytics and the enforcement of e-invoicing legislation are driving functional upgrades across enterprises. To stand out in the competitive landscape, vendors are incorporating advanced features such as AI-driven candidate scoring, predictive attrition analysis, and sentiment analysis into their offerings.

The persistent shortage of approximately 100,000 SAP specialists across Europe further amplifies the demand for low-code workflow builders. Enterprises are now placing greater emphasis on solutions that empower HR and finance teams to modify rules independently, without requiring ABAP coding expertise. This shift not only shortens release cycles but also reduces dependency on the limited pool of specialized consultants, enabling organizations to adapt more quickly to evolving business needs.

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Sage Group plc

- proALPHA Business Solutions GmbH

- Abas Software GmbH

- IFS AB

- Unit4 NV

- Epicor Software Corporation

- Workday Inc.

- Deltek Inc.

- DATEV eG

- Haufe-Lexware GmbH & Co. KG

- Exact Holding B.V.

- SYSPRO (Pty) Ltd

- Priority Software Ltd

- Acumatica Inc.

- Forterro Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Cloud Adoption Among German Mid-Market Firms

- 4.2.2 Stringent Data Protection Regulations Driving Demand for Compliant ERP

- 4.2.3 Industry 4.0 Push Within German Manufacturing

- 4.2.4 Rising Need for Real-Time Supply Chain Visibility

- 4.2.5 De-carbonization Reporting Mandates Fueling ERP Sustainability Modules

- 4.2.6 Shortage of Skilled SAP ABAP Developers Pushing Low-Code ERP Adoption

- 4.3 Market Restraints

- 4.3.1 Legacy System Complexity and High Migration Costs

- 4.3.2 Stringent Data Residency Concerns Limiting Public Cloud Uptake

- 4.3.3 Economic Uncertainty Curbing IT Budgets Among SMEs

- 4.3.4 Rising Energy Prices Increasing On-Premise TCO and Hindering Upgrades

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Sage Group plc

- 6.4.6 proALPHA Business Solutions GmbH

- 6.4.7 Abas Software GmbH

- 6.4.8 IFS AB

- 6.4.9 Unit4 NV

- 6.4.10 Epicor Software Corporation

- 6.4.11 Workday Inc.

- 6.4.12 Deltek Inc.

- 6.4.13 DATEV eG

- 6.4.14 Haufe-Lexware GmbH & Co. KG

- 6.4.15 Exact Holding B.V.

- 6.4.16 SYSPRO (Pty) Ltd

- 6.4.17 Priority Software Ltd

- 6.4.18 Acumatica Inc.

- 6.4.19 Forterro Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment