PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065540

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065540

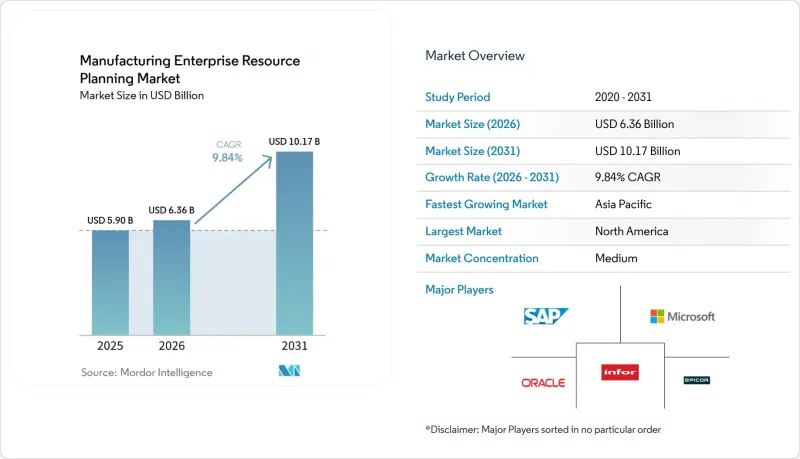

Manufacturing Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the manufacturing ERP market size is projected to expand from USD 5.90 billion in 2025 and USD 6.36 billion in 2026 to USD 10.17 billion by 2031, registering a CAGR of 9.84% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and SMEs), Manufacturing Mode (Discrete, Process, and Mixed-Mode), End-Industry Vertical (Automotive, Aerospace and Defense, Electronics and High-Tech, Food and Beverage, Industrial Machinery, Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Manufacturing Enterprise Resource Planning Market Trends and Insights

Cloud-First Digital Transformation Initiatives in Manufacturing

Manufacturers are relocating transactional workloads to public-cloud infrastructure at scale, lifting cloud adoption to 55.40% market share in 2025. Subscription pricing eliminates upfront license fees for mid-tier firms, and elastic compute lets globally distributed design and procurement teams collaborate in real time, a capability that helped electronics suppliers reroute constrained semiconductors within hours during the 2025 shortage. United States subsidy programs under the CHIPS and Science Act require digital-twin and cloud analytics capabilities, turning modernization into a prerequisite for federal grants. Europe's Machinery Regulation 2023/1230 sets a similar tone by mandating digital product passports by 2026. To balance sovereignty concerns, plants keep recipes on-premises while offloading demand planning to the cloud, which underpins the 18.00% CAGR expected for hybrid deployments.

Integration of IIoT and Real-Time Analytics with ERP Platforms

Terabytes of sensor data from CNC machines and assembly robots often reside outside planning cycles, yet modern ERP suites now ingest MQTT and OPC-UA streams to trigger predictive maintenance and automatically reschedule orders. Tier-one automotive suppliers that closed this loop cut unplanned downtime in 2025, boosting on-time delivery and preferred-supplier status. APAC electronics assemblers lead adoption due to high-mix lines where yield losses are costly. Edge gateways retain millisecond-sensitive control logic on site, while summarized KPIs flow to cloud ERP dashboards, proving that latency and insight can coexist in a tiered architecture.

High Total Cost of Ownership and Complex Implementation for Legacy-Heavy Plants

Brownfield facilities still running three-decade-old controllers face integration costs 40-60% above greenfield benchmarks because proprietary protocols demand custom middleware. A 2025 survey found 38% of North American plants using MS-DOS shop-floor systems that cannot exchange live data, forcing parallel manual entry that erodes automation gains. Replacing antiquated automation often exceeds the software budget, so projects stretch 24-36 months while consultants reverse-engineer undocumented customizations, tying up capital and depressing output during cut-over phases.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Pressure for Traceability and Compliance Across Global Supply Chains

- Shift Toward AI-Enabled Predictive Maintenance and Quality Management

- Cybersecurity and IP Theft Concerns in Cloud-Based Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The manufacturing ERP market size for hybrid deployments is advancing at an 18.00% CAGR as companies reconcile cloud agility with residency laws. In 2025, cloud held 55.40% of the manufacturing ERP market share, yet plants in regulated sectors such as defense and pharmaceuticals still favor on-premises control for export-controlled data. The European GDPR and China's Cybersecurity Law keep recipes and customer files within national borders, pushing firms toward tiered architectures that sync anonymized planning data into public cloud analytics engines.

Edge gateways process millisecond-grade telemetry locally, then post aggregated KPIs to cloud dashboards. As vendors deliver containerized services that run wherever compute resides, hybrid has become the default compromise, particularly for multinational automakers juggling divergent jurisdictional rules.

Large enterprises still account for the majority of purchasing, yet SMEs are the fastest-growing cohort in the manufacturing ERP market, with a 17.00% CAGR. Subscription models eliminate the USD 500,000 capex hurdle of perpetual licenses, while pre-configured vertical SaaS suites compress implementation from 18 months to roughly 8 weeks. Greenfield shops with minimal legacy baggage jump directly to mobile-native interfaces, freeing supervisors from desktop workstations.

Succession-planning pressures also spur digitization as retiring founders codify shop-floor knowledge in software to attract buyers. Regional grants in the United States and Europe further de-risk modernization for smaller plants, accelerating the pivot toward cloud.

Geography Analysis

North America generated 38.60% of global revenue in 2025 as the CHIPS and Science Act incentives tied grants to cloud-based digital twins, prompting semiconductor plants to standardize on modern ERP from day one. reshoring efforts and Mexico's nearshoring boom extend standardized platforms across NAFTA trade corridors, while Canadian factories adopt carbon-tracking features to prepare for prospective border-adjustment levies.

Europe invests heavily to meet the CSRD's Scope 3 emission-disclosure mandate that makes ERP the data backbone for carbon accounting. Germany's Industrie 4.0 and the Machinery Regulation's digital passport requirement accelerate spending in automotive and machinery clusters. Southern European plants tap EU digitization funds to offset subscription fees, narrowing the digital divide with the north.

Asia-Pacific is the fastest-growing region, with a 8.80% CAGR. India links Production-Linked Incentive payouts to ERP-driven production reporting. China mandates domestic ERP systems for state-owned firms to curb IP leakage, opening the door for local vendors. Southeast Asian contract manufacturers adopt cloud suites to meet real-time visibility standards imposed by electronics OEMs. South America, the Middle East, and Africa together remain smaller but show hotspots of rapid adoption, notably in GCC petrochemicals and Brazilian EV supply chains.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- QAD Inc.

- IFS AB

- Plex Systems, Inc.

- SYSPRO (Pty) Ltd.

- Abas Software GmbH

- Acumatica, Inc.

- Rootstock Software

- Aptean, Inc.

- Global Shop Solutions, Inc.

- Cetec ERP, LLC

- Priority Software Ltd.

- MRPeasy Ltd.

- DELMIAWorks (Dassault Systemes SE)

- Syspro Group (UK) Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Digital Transformation Initiatives in Manufacturing

- 4.2.2 Integration of IIoT and Real-Time Analytics with ERP Platforms

- 4.2.3 Regulatory Pressure for Traceability and Compliance Across Global Supply Chains

- 4.2.4 Shift Toward AI-Enabled Predictive Maintenance and Quality Management

- 4.2.5 Proliferation of Industry-Specific SaaS ERP Offerings for SMB Manufacturers

- 4.2.6 Sustainability Reporting Mandates Driving ERP Adoption for ESG Data

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership and Complex Implementation for Legacy-Heavy Plants

- 4.3.2 Cybersecurity and IP Theft Concerns in Cloud-Based Deployments

- 4.3.3 Shortage of Skilled ERP Implementation Professionals in Manufacturing Hubs

- 4.3.4 Organisational Change Resistance and Disruption to Established Production Workflows

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Enterprises (SMEs)

- 5.3 By Manufacturing Mode

- 5.3.1 Discrete Manufacturing

- 5.3.2 Process Manufacturing

- 5.3.3 Mixed-Mode Manufacturing

- 5.4 By End-Industry Vertical

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and High-Tech

- 5.4.4 Food and Beverage

- 5.4.5 Industrial Machinery

- 5.4.6 Pharmaceuticals

- 5.4.7 Other End-Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 QAD Inc.

- 6.4.7 IFS AB

- 6.4.8 Plex Systems, Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Abas Software GmbH

- 6.4.11 Acumatica, Inc.

- 6.4.12 Rootstock Software

- 6.4.13 Aptean, Inc.

- 6.4.14 Global Shop Solutions, Inc.

- 6.4.15 Cetec ERP, LLC

- 6.4.16 Priority Software Ltd.

- 6.4.17 MRPeasy Ltd.

- 6.4.18 DELMIAWorks (Dassault Systemes SE)

- 6.4.19 Syspro Group (UK) Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment