PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065550

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065550

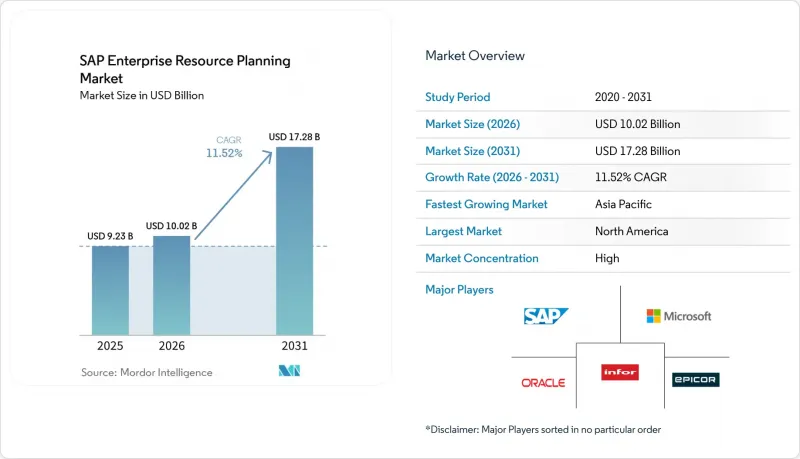

SAP Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sAP enterprise resource planning market size was valued at USD 9.23 billion in 2025 and estimated to grow from USD 10.02 billion in 2026 to reach USD 17.28 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

This report is Segmented by Deployment Model (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises and SMEs), Industry Vertical (Manufacturing, Retail, BFSI, Healthcare, Energy and Utilities, Telecommunications, and More), Module (Financial Management, SCM, HCM, Customer Relationship Management, and More), and Geography. The Market Forecasts are in Value (USD).

Global SAP Enterprise Resource Planning Market Trends and Insights

Growing Demand for Real-Time Business Analytics

Enterprises are replacing nightly batch reports with in-memory dashboards that surface profit leaks and inventory anomalies in seconds. New SAP Joule skills inside S/4HANA Private Edition let finance teams extend expiring price lists with a single prompt, cutting multi-minute tasks to seconds. Pre-configured retail and asset-management data products further shorten the path from raw transactions to AI-ready models. Oracle's rival data agents now bind ERP data to HR policies and supplier contracts, showing customers that autonomous forecasting is table stakes rather than a novelty. The race for predictive and prescriptive insights is therefore compressing upgrade horizons and sustaining double-digit expansion in the SAP Enterprise Resource Planning market.

Acceleration of Cloud-First Digital Transformation Strategies

Expiring data-center leases, hyperscaler incentives, and board-level mandates are pushing firms to cloud deployments well ahead of earlier roadmaps. A four-week factory deployment by Ahlstrom demonstrated that a clean-core S/4HANA Public Cloud roll-out can beat legacy upgrade timelines by months while unlocking Joule-powered AI from day one. RAK Ceramics' decision to move 55 legal entities to S/4HANA Private Cloud echoes the same urgency among diversified manufacturers. Microsoft's 99.95% SLA option in Azure removes the final objection to uptime for mission-critical workloads. Together, these factors sustain a robust mid-teens growth clip for cloud subscriptions inside the broader SAP Enterprise Resource Planning market.

High Migration Costs From ECC to S/4HANA For Legacy Users

Sixteen-terabyte conversions like Al-Futtaim's spotlight the millions of dollars and long weekends needed to migrate decades of custom code and data aggregates. Even with automated tooling, 30-hour outages remain common. Capital now flows into clean-core redesigns, data scrubbing, and change-management programs, diverting funds from innovation workstreams. As long as retrofit costs stay elevated, some mid-market firms defer upgrades, tempering near-term expansion of the SAP Enterprise Resource Planning market.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI and Machine Learning Add-Ons Within SAP

- Rise of Composable ERP Architecture Among Large Enterprises

- Skill Shortage of Certified SAP Consultants In Emerging Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud captured 48.20% SAP Enterprise Resource Planning market share in 2025 and is forecast to post a 14.20% CAGR to 2031. Multitenant SaaS offerings such as GROW with SAP lure mid-market firms with fixed-price bundles, while large manufacturers embrace Private Cloud editions tied to hyperscaler SLAs. On-premises persists in defense and public-sector accounts with strict data-residency rules, keeping hybrid footprints alive as a stepping stone. Cloud-native deployments enjoy quicker access to Joule agents and pre-configured data products, reinforcing their advantage over legacy stacks.

Customers report lower total ownership once infrastructure management shifts to Azure, AWS, or Alibaba Cloud. Clean-core policies mean fewer breakpoints during quarterly release cycles, improving uptime and auditability. Hybrid estates, by contrast, often juggle double integration layers and inconsistent user experiences. As hyperscalers add sovereign-cloud regions, regulatory barriers ease further, driving incremental share gains for cloud and sustaining the expansion of the SAP Enterprise Resource Planning market.

Large enterprises accounted for 63.40% of revenue in 2025 thanks to multi-country rollouts, complex intercompany eliminations, and broader module counts. They remain the revenue anchor of the SAP Enterprise Resource Planning market size, but small and medium enterprises will outpace them at a 15.90% CAGR through 2031. GROW with SAP provides predefined industry processes and low-code extensibility, enabling mid-market CFOs to obtain predictive cash flow insights without bespoke ABAP code.

Early adopters in Indonesia and Vietnam cite faster closings and improved profitability after moving to public-cloud editions. Large enterprises still dominate absolute spend because global templates require consolidation, trade-compliance engines, and deep manufacturing execution tie-ins. Yet mid-market momentum expands the total addressable base, underpinning the long-term health of the SAP Enterprise Resource Planning market.

Geography Analysis

North America retained a 35.90% share in 2025, driven by Fortune 500 ERP refreshes and early cloud adoption. Azure's new 99.95% SLA removes objections to uptime for life-and-mission-critical installations, spurring further cloud migrations. Europe's GDPR and sustainability mandates are driving private-cloud and clean-core strategies, even as digital sovereignty concerns slow multitenant adoption. Government-backed sovereign clouds in France and Germany soften that stance, aligning compliance with innovation.

Asia-Pacific is forecast to record the fastest 13.80% CAGR, buoyed by India's emergence as SAP's AI hub and rapid skills-pipeline expansion. Sovereign-cloud policies in Japan and Australia encourage local hyperscaler-SAP zones, unlocking public-sector demand. China remains a nuanced play, with joint ventures adopting S/4HANA Private Cloud to stay aligned with global parents while satisfying localization rules.

Middle East and Africa exhibit mixed maturity. Vision 2030 investments in Saudi Arabia and large private-sector projects in the United Arab Emirates move public-cloud ERP into mainstream budgets. South Africa's state-owned enterprises prove that selective data transitions can succeed even under tight operational windows. Infrastructure gaps and consultant shortages restrain smaller economies, but anchor projects by mining and telecom majors seed future expansion of the SAP Enterprise Resource Planning market.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- Unit4 N.V.

- IFS AB

- The Sage Group plc

- Workday Inc.

- QAD Inc.

- Acumatica Inc.

- SYSPRO (Pty) Ltd.

- Deltek Inc.

- Ramco Systems Limited

- TOTVS S.A.

- Kingdee International Software Group Company Limited

- Yonyou Network Technology Co., Ltd.

- Priority Software Ltd.

- Plex Systems Inc.

- Cegid Group SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for real-time business analytics

- 4.2.2 Acceleration of cloud-first digital transformation strategies

- 4.2.3 Integration of AI and machine learning add-ons within SAP S/4HANA

- 4.2.4 Rise of composable ERP architecture among large enterprises

- 4.2.5 Sustainability compliance modules driving upgrades

- 4.2.6 Industry-cloud bundles tailored for mid-market niches

- 4.3 Market Restraints

- 4.3.1 High migration costs from ECC to S/4HANA for legacy users

- 4.3.2 Skill shortage of certified SAP consultants in emerging regions

- 4.3.3 Cyber-resilience concerns around multi-tenant deployments

- 4.3.4 Vendor lock-in anxiety amid hyperscaler partnerships

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 Retail and Consumer Goods

- 5.3.3 BFSI

- 5.3.4 Healthcare

- 5.3.5 Energy and Utilities

- 5.3.6 Telecommunications

- 5.3.7 Rest of Industry Verticals

- 5.4 By Module

- 5.4.1 Financial Management

- 5.4.2 Supply Chain Management

- 5.4.3 Human Capital Management

- 5.4.4 Customer Relationship Management

- 5.4.5 Production Planning and Execution

- 5.4.6 Analytics and Business Intelligence

- 5.4.7 Other Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 Unit4 N.V.

- 6.4.7 IFS AB

- 6.4.8 The Sage Group plc

- 6.4.9 Workday Inc.

- 6.4.10 QAD Inc.

- 6.4.11 Acumatica Inc.

- 6.4.12 SYSPRO (Pty) Ltd.

- 6.4.13 Deltek Inc.

- 6.4.14 Ramco Systems Limited

- 6.4.15 TOTVS S.A.

- 6.4.16 Kingdee International Software Group Company Limited

- 6.4.17 Yonyou Network Technology Co., Ltd.

- 6.4.18 Priority Software Ltd.

- 6.4.19 Plex Systems Inc.

- 6.4.20 Cegid Group SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment