PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062410

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062410

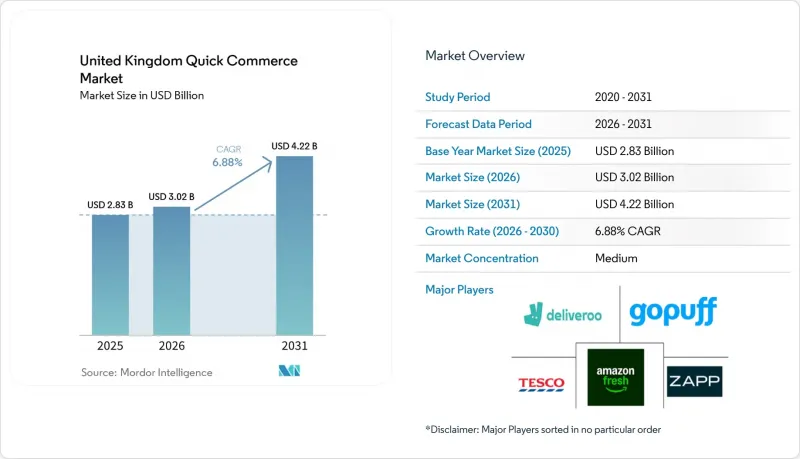

United Kingdom Quick Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom (UK) quick commerce market size was valued at USD 2.83 billion in 2025 and estimated to grow from USD 3.02 billion in 2026 to reach USD 4.22 billion by 2031, at a CAGR of 6.88% during the forecast period (2026-2031).

This report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care, Home Supplies, Electronics, Pet Care, and Flowers and Gifts), Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes). The Market Forecasts are in Value (USD).

United Kingdom Quick Commerce Market Trends and Insights

Growing Consumer Demand For Hyper-Convenience In Urban Centers

Urban density remained the clearest demand driver for the UK quick commerce market, and that demand extended well beyond the narrow pandemic-user cohort. Survey work from March 2026 showed that 67% of British adults were aware of rapid grocery delivery services, while convenience at 47% and speed at 43% were the main reasons for use. The same survey also showed that 38% of active users were willing to switch providers for better delivery options, which points to service quality as a core retention lever. Usage widened across age groups as well, with Gen Z penetration reaching 66% in 2024, while the average basket value rose from GBP 30 (USD 38.4) to GBP 40 (USD 51.2) between 2021 and 2024. That change suggests that many shoppers now use the United Kingdom quick commerce market for planned convenience spending rather than one-off impulse orders. Co-op's goal of capturing close to one-third of the store-to-door rapid delivery space by 2027, supported by a GBP 1 million (USD 1.3 million) first-year investment in the Peckish platform, reflects that broader behavior shift across urban convenience retail.

Expansion Of Dark-Store Networks By Major Grocery Chains

The expansion of dark-store capacity by grocery incumbents is reshaping the United Kingdom quick commerce market through asset reuse rather than pure new-build rollout. Tesco's Whoosh service operated from 1,600 stores, including 180 large-format sites, and reached more than 70% of United Kingdom households by early 2026, while sales rose 47% year over year in the 19 weeks ending January 3. This model is structurally important because store-based rapid fulfillment avoids the annual lease burden of a standalone dark store, which the input placed at more than GBP 500,000 (USD 640,000). Amazon also moved more decisively into this model when it launched Amazon Now from a purpose-built Southwark dark store in January 2026 and then added Battersea and Lewisham while securing at least 4 more sites. Tesco's acquisition of 5 former Amazon Fresh sites after Amazon shut all 14 of its United Kingdom Fresh stores in September 2025 showed how quickly physical assets can be recycled across competing retail networks. The result is a planning environment in which existing retailers can scale faster and with less regulatory friction than pure-play operators that still need separate change-of-use approvals.

High Burn Rates And Path-To-Profitability Challenges

Profitability remains one of the clearest operating constraints on the United Kingdom quick commerce market, even after the most aggressive subsidy phase faded. Gopuff's United Kingdom business reduced its pre-tax loss from GBP 93.8 million (USD 120.1 million) to GBP 51.6 million (USD 66.0 million) in 2023, while revenue rose from GBP 42.8 million (USD 54.8 million) to GBP 78.1 million (USD 100 million), yet cumulative losses since entry still exceeded GBP 187 million (USD 239.4 million). Deliveroo showed the other side of the picture when it recorded its first full year of profitability in 2024, with GBP 2.9 million (USD 3.7 million) profit on GBP 7.4 billion gross transaction value. That result came mainly from better stacked-order efficiency and lower marketing spend, rather than from a broad margin reset in rapid grocery. Platform margins also remain under pressure because large grocery partners can negotiate harder on commissions as they scale. In less dense parts of the United Kingdom quick commerce market, breakeven still depends on maintaining 8 or more orders per rider-hour, and that threshold remains difficult to protect when order density weakens.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of AI-Driven Demand Forecasting Reducing Stock-Outs

- Rising Penetration Of 5G Smartphones Accelerating Mobile-First Ordering

- Regulatory Uncertainty Around Gig-Worker Employment Status

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grocery and Staples accounted for 52.61% of the United Kingdom quick commerce market share in 2025, which confirmed that emergency and top-up grocery missions still formed the core demand base. Electronics and Accessories is the fastest-growing product segment in the United Kingdom quick commerce market, with a projected 7.10% CAGR from 2026 to 2031. That growth reflects a change in purchase behavior as urban consumers increasingly apply instant-delivery expectations to chargers, earphones, and other small but high-urgency items. Deliveroo said its retail proposition added around 2,000 partner sites in 2024, and the retail vertical delivered double-digit gross transaction value growth in the second half of the year. Personal Care and OTC Pharma also gained momentum as Boots expanded its on-demand service through Deliveroo and Uber Eats to 500 United Kingdom stores by September 2025 and offered more than 10,000 products with delivery times as short as 30 minutes.

Fresh Produce and Dairy, Snacks and Beverages, and Home and Cleaning Supplies continued to add meaningful volume around the grocery core of the United Kingdom quick commerce market. These categories work well because they can be picked within the same pathways as staple grocery orders, which helps lift average basket value without the same level of extra cost. Pet Care and Flowers and Gifts stayed smaller in scale, but both serve a useful role because they carry stronger margins and lower return rates than many other non-food categories. Pet Care is especially relevant because recurring replenishment patterns can support better customer lifetime value and stronger repeat behavior. Procurement and fulfillment standards for fresh categories also continued to matter more as operators tried to protect quality while expanding the category mix.

List of Companies Covered in this Report:

- Snappy Shopper

- Gopuff

- Deliveroo plc

- Zapp

- Uber Technologies Inc.

- Just Eat Takeaway.com N.V.

- Ocado Group plc

- Tesco plc (Whoosh)

- J Sainsbury plc (Chop Chop)

- Co-operative Group Limited

- Amazon.com Inc. (Amazon Fresh)

- Marks & Spencer Group plc

- Morrisons (Morrisons on Amazon)

- Aldi Stores Limited

- Lidl Stiftung & Co. KG

- Waitrose Ltd. (Waitrose Rapid)

- Asda Stores Ltd.

- Iceland Foods Ltd.

- Stuart Delivery Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Penetration of 5G Smartphones Accelerating Mobile-First Ordering

- 4.2.2 Growing Consumer Demand for Hyper-Convenience in Urban Centers

- 4.2.3 Expansion of Dark-Store Networks by Major Grocery Chains

- 4.2.4 Venture Capital Infusion into Last-Mile Logistics Start-Ups

- 4.2.5 Integration of AI-Driven Demand Forecasting Reducing Stock-outs

- 4.2.6 Partnerships With Residential Real-Estate Operators for Lobby Micro-Fulfillment

- 4.3 Market Restraints

- 4.3.1 High Burn Rates and Path-to-Profitability Challenges

- 4.3.2 Regulatory Uncertainty Around Gig-Worker Employment Status

- 4.3.3 Rising Urban Congestion Charges Increasing Delivery Costs

- 4.3.4 Consumer Backlash Against Single-Use Packaging Waste

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Grocery and Staples

- 5.1.2 Fresh Produce and Dairy

- 5.1.3 Snacks and Beverages

- 5.1.4 Personal Care and OTC Pharma

- 5.1.5 Home and Cleaning Supplies

- 5.1.6 Electronics and Accessories

- 5.1.7 Pet Care

- 5.1.8 Flowers and Gifts

- 5.1.9 Other Product Categories

- 5.2 By Delivery Time Promise

- 5.2.1 Less than 10 Minutes

- 5.2.2 11-30 Minutes

- 5.2.3 31-60 Minutes and More

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Snappy Shopper

- 6.4.2 Gopuff

- 6.4.3 Deliveroo plc

- 6.4.4 Zapp

- 6.4.5 Uber Technologies Inc.

- 6.4.6 Just Eat Takeaway.com N.V.

- 6.4.7 Ocado Group plc

- 6.4.8 Tesco plc (Whoosh)

- 6.4.9 J Sainsbury plc (Chop Chop)

- 6.4.10 Co-operative Group Limited

- 6.4.11 Amazon.com Inc. (Amazon Fresh)

- 6.4.12 Marks & Spencer Group plc

- 6.4.13 Morrisons (Morrisons on Amazon)

- 6.4.14 Aldi Stores Limited

- 6.4.15 Lidl Stiftung & Co. KG

- 6.4.16 Waitrose Ltd. (Waitrose Rapid)

- 6.4.17 Asda Stores Ltd.

- 6.4.18 Iceland Foods Ltd.

- 6.4.19 Stuart Delivery Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment