PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063487

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063487

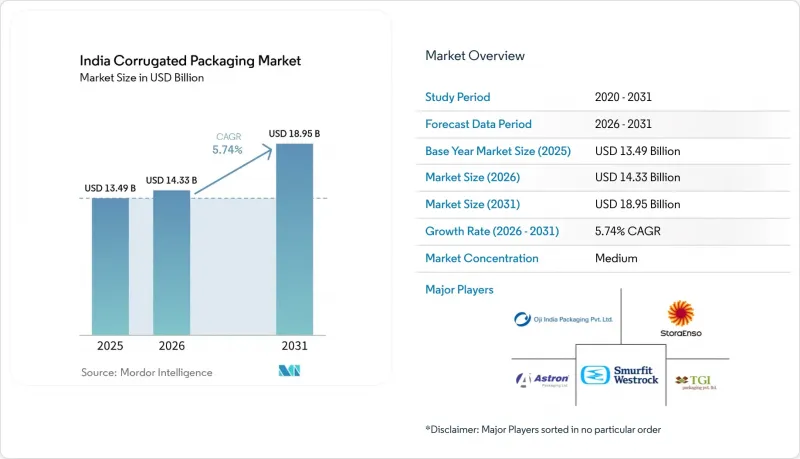

India Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india corrugated packaging market size is expected to increase from USD 13.49 billion in 2025 to USD 14.33 billion in 2026 and reach USD 18.95 billion by 2031, growing at a CAGR of 5.74% over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, B Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, Double-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Corrugated Packaging Market Trends and Insights

Rising E-Commerce Logistics Acceleration

Quick-commerce operators cut delivery windows to 10-15 minutes in 2025, forcing dark-store layouts that rely on shelf-ready corrugated totes doubling as display units. Amazon India surpassed 60 fulfillment centers, each standardizing corrugate footprints to mesh with robotic arms, which raised demand for high-precision die-cuts with +-1 mm tolerances. Flipkart's augmented-reality storefront initiative triggered a spike in litho-laminated mailers, as photogenic packaging boosts conversion on mobile product pages. Parallel to these design shifts, leading platforms mandated burst strengths 15% above BIS IS 2771 to minimize monsoon-season returns, compelling converters to blend recycled linerboard with imported long-fiber kraft for edge-crush stability. Together, these pressures accelerate upgrade cycles toward high-speed flexo-folder-gluers and single-pass digital presses that can swap artwork in minutes without halting lines.

Growth in Processed Food and Beverage Exports

India's processed food exports climbed to USD 8.7 billion in FY 2024-25, channeling roughly 40% of packaging spend into corrugated secondary formats. Ventilated mango and grape cartons with moisture-barrier liners now meet 21-day sea-freight shelf-life targets for European grocery chains, amplifying demand for triple-wall boxes coated with biodegradable starch films. Punjab basmati shippers achieved a 12-point reduction in breakage after switching from jute sacks to palletized corrugated bins, unlocking A-grade shelf placement premiums in UK supermarkets. On the beverage side, craft spirit exports surged once Uttar Pradesh relaxed micro-distillery rules; litho-laminated six-packs that conform to U.S. TTB labeling moved from a niche to a baseline SKU.

Recycled Paper Price Volatility

Old Corrugated Containers import prices climbed 18% year-on-year in early 2025 and then eased as Chinese demand softened, creating margin whiplash for converters that carry 45-60 days of feedstock inventory. Domestic collection relies on informal waste-picker networks that lack transparent spot pricing, so converters in Uttar Pradesh and Bihar often pay premiums that erode the recycled-fiber cost advantage. The Directorate General of Trade Remedies' 2024 minimum-import-price floor on virgin linerboard narrowed the spread between recycled and virgin grades, further squeezing mills that cannot hedge OCC costs through futures contracts. Larger players have responded by signing multi-year supply pacts with municipal aggregators and by co-locating baling stations at major consumption hubs, but small single-corrugator firms lack that bargaining power. Until India formalizes an exchange-traded OCC benchmark, the Indian corrugated packaging market will see periodic pricing shocks that discourage capacity expansion during tight cycles.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift Toward Recyclable Packaging

- Nearshoring-Led Electronics Output

- Competition from Returnable Plastic Crates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard represented 46.68% of the Indian corrugated packaging market share in 2025, confirming the role of post-consumer fiber in meeting cost targets for e-commerce and FMCG cartons. Semi-chemical fluting, the fastest-rising substrate at 7.48% CAGR, attracts electronics assemblers that need lighter inserts to pass drop tests without breaching air-freight weight bands. Virgin Kraft retains a niche in export-oriented rice, spirits, and smartphone boxes that must carry FSC logos, keeping imports of northern bleached softwood kraft afloat despite domestic price floors. Other specialty grades, such as moisture-resistant liners, serve frozen seafood exporters that face condensation inside reefers, a segment where converters charge 12-15% premiums.

Policy dynamics could reshape the Indian corrugated packaging market for virgin fiber, as the 2024 Forest Conservation Act opened degraded land to farm forestry, a move intended to trim USD 1.2 billion in pulp imports. Astron Packaging's USD 90 million Pune mill, commissioned in August 2025, bets that recycled linerboard will remain the volume workhorse while premium tiers continue to source imported kraft. Experiments with wheat-straw and bagasse pulps signal an eventual broadening of the feedstock base, though inconsistent fiber quality keeps commercial output limited. As mills upgrade de-inking and water-recycling loops to cut resource intensity, recycled grades are likely to deepen their hold on the India corrugated packaging market.

B flute held 41.37% of 2025 shipments, prized for its 3.2 mm height that balances cushioning and print real estate for general-purpose shipping cases. E flute posted a 6.93% CAGR and is on track to expand its market share in India's corrugated packaging market as smartphone, pharma, and cosmetics brands embrace thinner profiles that enable pallet density gains without failing ISTA 3A tests. C flute remains entrenched in heavy parts and ceramic tiles where stacking loads exceed 1,000 kg. A flute and F flute fill opposite niches, fragile glassware on the high-cushion side and luxury gift packs on the ultra-thin side.

Oji India installed high-speed corrugators that switch between E-flute and F-flute at its Sri City plant in March 2025 to serve electronics OEMs that demand +-0.5 mm caliper control. E-commerce platforms, meanwhile, impose dimensional caps that penalize bulky C flute boxes, reinforcing the material-reduction tilt of the Indian corrugated packaging market. Quality compliance for thinner flutes drives capital upgrades in adhesive control, board inspection, and automatic slotting, favoring large converters over cottage-scale plants that still rely on manual glue stations.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- Rengo Co. Ltd.

- Stora Enso Oyj

- B and B Triplewall Containers Ltd.

- Oji India Packaging Pvt. Ltd.

- Horizon Packs Pvt. Ltd.

- TGI Packaging Pvt. Ltd.

- Astron Packaging Ltd.

- Worth Peripherals Ltd.

- JK Packaging Pvt. Ltd.

- Sri Krishna Packaging

- Kanpur Packaging Industries

- Packman Packaging Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-commerce Logistics Acceleration

- 4.2.2 Growth in Processed Food and Beverage Exports

- 4.2.3 Regulatory Shift Toward Recyclable Packaging

- 4.2.4 Nearshoring-Led Electronics Output

- 4.2.5 Craft-Brewery Demand for Custom Boxes

- 4.2.6 Government Subsidies for Bio-Based Barrier Coatings

- 4.3 Market Restraints

- 4.3.1 Recycled Paper Price Volatility

- 4.3.2 Competition from Returnable Plastic Crates

- 4.3.3 Water-Scarcity Constraints on Mills

- 4.3.4 Dependence on Imported Virgin Fiber

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Rengo Co. Ltd.

- 6.4.3 Stora Enso Oyj

- 6.4.4 B and B Triplewall Containers Ltd.

- 6.4.5 Oji India Packaging Pvt. Ltd.

- 6.4.6 Horizon Packs Pvt. Ltd.

- 6.4.7 TGI Packaging Pvt. Ltd.

- 6.4.8 Astron Packaging Ltd.

- 6.4.9 Worth Peripherals Ltd.

- 6.4.10 JK Packaging Pvt. Ltd.

- 6.4.11 Sri Krishna Packaging

- 6.4.12 Kanpur Packaging Industries

- 6.4.13 Packman Packaging Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment