PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065513

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065513

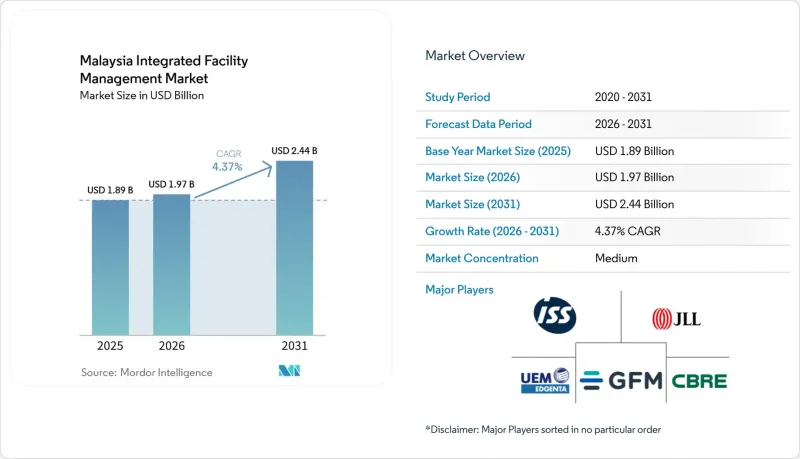

Malaysia Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the malaysia integrated facility management market size is expected to grow from USD 1.89 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 2.44 billion by 2031 at 4.37% CAGR over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Service, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Integrated Facility Management Market Trends and Insights

Growing Adoption of Smart Technologies in Facility Management

The Malaysia integrated facility management market is moving toward a more digital operating model as building owners expect better asset visibility, faster response times, and tighter control of maintenance spending. The July 1, 2025, BIM mandate for public and private construction projects valued at MYR 10 million (USD 2.25 million), or more raised the baseline for digital handover and made structured asset data more important when new buildings enter service. Asset information aligned with PeDATA and SKATA standards improves 3D visualization, scheduled maintenance, and lifecycle planning, which gives the Malaysia integrated facility management market a stronger link between project completion and ongoing service delivery. This matters because providers with BIM-linked CMMS platforms can carry forward asset histories and maintenance rules in ways that disconnected operators cannot easily match. Research cited in the draft also showed that GBI-certified buildings had a 28% adoption rate for digital twin and HVAC-BMS integration, compared with 7% in non-certified stock, which shows how premium buildings are advancing FM practices faster than the wider building base. As a result, the Malaysia integrated facility management market is rewarding operators that can combine software, building controls, and field execution into one service model rather than treating technology as a stand-alone add-on.

Rapid Expansion of Commercial Real Estate and Industrial Assets In Urban Centers

The Malaysia integrated facility management market is expanding with the country's rising stock of commercial, industrial, logistics, and mixed-use assets, especially in Johor and the Klang Valley. Approved investments reached MYR 285.2 billion (USD 64.12 billion), in the first nine months of 2025, and Johor alone drew MYR 91.1 billion (USD 20.47 billion), which increased the long-term need for structured services across new buildings and industrial sites. CapitaLand Investment's partnership with Coronade Properties on the 1.25 million sq ft Coronation Square Mall in Johor Bahru added another visible example of a large-format commercial asset that will require bundled maintenance, cleaning, security, landscaping, and energy management throughout its operating life. The same pattern is visible in industrial property, where portfolio expansion in logistics and manufacturing assets is creating more recurring service demand across high-use facilities with stricter uptime and compliance requirements. The Malaysia integrated facility management market is also seeing a quality shift because data centers require 24-hour uptime management, precision cooling, power continuity, and advanced fire suppression, which makes those contracts more complex than conventional office or retail work. That difference supports a stronger growth profile for providers that can manage critical environments rather than only general building operations.

Fragmented Market Structure with Compliance and Certification Challenges

The Malaysian integrated facility management market has a healthy demand base, but service quality remains uneven because a large share of providers still operate at a small scale across local tender markets. A 2024 literature review cited in the draft found that the sector's main challenge was the lack of standardized maintenance processes across operators, which leads to inconsistent delivery quality and weaker contract renewal potential. Providers also need to manage overlapping registration and approval requirements across CIDB, the Ministry of Finance, JKR-linked public works structures, and healthcare-specific rules, which can be difficult for mid-sized firms with limited compliance staff. This keeps a meaningful share of government-linked work within a relatively small certified pool, even when the broader Malaysia integrated facility management market remains crowded. The same fragmentation also makes it harder for clients to compare providers on a standard basis because performance measures are not yet uniform across contracts. As long as certification depth and operating discipline remain uneven, the Malaysia integrated facility management market will continue to show a split between well-qualified concessionaires and a more price-led middle tier.

Other drivers and restraints analyzed in the detailed report include:

- Government Green Building Incentives and ESG Mandates

- Rise Of Public-Private Partnerships for Government Building Management

- High Initial Capital Requirements for Technology Adoption and System Integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) accounted for 61.6% of the Malaysia integrated facility management (IFM) market size in 2025, which shows how strongly the market still depends on recurring labour-based services across public, commercial, and institutional buildings. Cleaning, security, pest control, landscaping, waste management, catering, and reception services stayed dominant because they are needed frequently and across a broad building base, unlike mechanical maintenance, which follows a more periodic schedule. In the Malaysia IFM industry, those soft service categories also face the most intense price competition because switching costs remain low in cleaning and guarding contracts. Providers therefore rely heavily on workforce control, route planning, attendance tracking, and tighter scheduling to protect margins in contracts that are large by volume but thinner in profitability. The February 2025 minimum wage increase to MYR 1,700 (USD 382) per month placed extra pressure on this segment because labour cost is still the largest cost item in most soft service contracts.

Hard FM is forecast to grow at a 5.1% CAGR through 2031, making it the fastest-growing service category within the Malaysia IFM market. This part of the market is being lifted by more technically demanding buildings that need specialized work across electromechanical systems, HVAC, fire safety, and mission-critical infrastructure. The Malaysia IFM market share is still led by Soft FM, but Hard FM is closing the gap in value terms because each contract now carries more technical scope and tighter uptime requirements. Data center development in Johor is an important reason, since facilities operating at low PUE levels and under 24-hour service expectations need precision cooling, power continuity, and constant optimization that go beyond conventional commercial maintenance. Johnson Controls' work across multiple Sunway Group properties also shows how one building technology deployment can spread across a developer's wider portfolio, which strengthens repeat hard-service revenue once performance is proven. In the Malaysia IFM industry, the July 2025 BIM requirement also supports Hard FM because digital handover makes it easier to structure asset maintenance from the first day a building enters operation.

List of Companies Covered in this Report:

- UEM Edgenta Berhad

- GFM Services Berhad

- ISS A/S

- CBRE Group, Inc.

- JLL Malaysia Sdn Bhd

- Cushman and Wakefield plc

- Knight Frank Malaysia Sdn Bhd

- Colliers International Group Inc.

- KFM Holdings Sdn Bhd

- AWC Berhad

- Sime Darby Property Berhad

- Sodexo S.A.

- OCS Group Limited

- Allied Universal

- G4S Limited

- Johnson Controls International plc

- Honeywell International Inc.

- Tenaga Nasional Berhad

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Smart Technologies In Facility Management

- 4.2.2 Rapid Expansion Of Commercial Real Estate And Industrial Assets In Urban Centers

- 4.2.3 Government Green Building Incentives And ESG Mandates

- 4.2.4 Rise Of Public-Private Partnerships For Government Building Management

- 4.2.5 Mandatory BIM Integration And Digital Twin Adoption In FM

- 4.2.6 Increasing Corporate Focus On Workplace Health, Wellness, And Indoor Environmental Quality

- 4.3 Market Restraints

- 4.3.1 Fragmented Market Structure With Compliance And Certification Challenges

- 4.3.2 High Initial Capital Requirements For Technology Adoption And System Integration

- 4.3.3 Shortage Of Technically Skilled FM Professionals And High Workforce Turnover

- 4.3.4 Regulatory And Competitive Barriers For International Operators

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 UEM Edgenta Berhad

- 6.4.2 GFM Services Berhad

- 6.4.3 ISS A/S

- 6.4.4 CBRE Group, Inc.

- 6.4.5 JLL Malaysia Sdn Bhd

- 6.4.6 Cushman and Wakefield plc

- 6.4.7 Knight Frank Malaysia Sdn Bhd

- 6.4.8 Colliers International Group Inc.

- 6.4.9 KFM Holdings Sdn Bhd

- 6.4.10 AWC Berhad

- 6.4.11 Sime Darby Property Berhad

- 6.4.12 Sodexo S.A.

- 6.4.13 OCS Group Limited

- 6.4.14 Allied Universal

- 6.4.15 G4S Limited

- 6.4.16 Johnson Controls International plc

- 6.4.17 Honeywell International Inc.

- 6.4.18 Tenaga Nasional Berhad

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment