PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065755

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065755

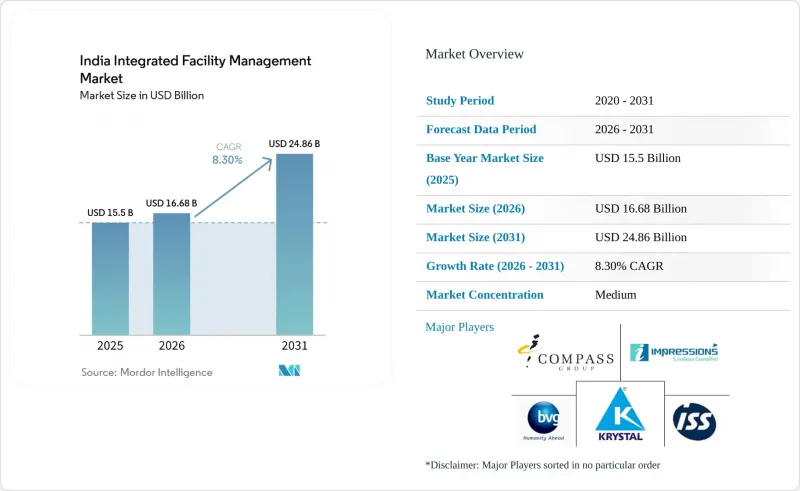

India Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india integrated facility management market size is projected to be USD 15.5 billion in 2025, USD 16.68 billion in 2026, and reach USD 24.86 billion by 2031, growing at a CAGR of 8.30% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Integrated Facility Management Market Trends and Insights

Expansion Of Grade A Offices and Mixed-use Campuses

India's Grade A office market delivered its strongest year on record in 2025, with net absorption of 61.4 million sq ft across the top 8 cities, up 25% year over year, thereby directly expanding the professionally managed estate that requires continuous operating support. India is also expected to account for 40% of Asia-Pacific's 61.3 million sq ft of new Grade A office supply in 2026, which keeps the onboarding pipeline active for the India integrated facility management market. The quality mix matters as much as the quantity mix, because 80% of the new 2026 supply is expected to be green-certified, and that raises the service threshold for energy management, water monitoring, indoor air quality control, and audit-ready reporting. Mixed-use campuses are also bringing office, retail, hospitality, and food service functions into a single managed environment, which makes owners more likely to appoint one accountable operator across multiple service lines. This combination of scale, technical requirements, and ownership preference continues to favour integrated providers with balanced Hard FM and Soft FM depth, which supports the move toward fuller IFM contracts within the India integrated facility management market.

Vendor Consolidation into Integrated and Outcome-based Contracts

The India integrated facility management market is moving away from headcount-driven contracts and toward SLA-linked commercial models that measure uptime, energy efficiency, hygiene quality, and user experience rather than just labour deployment. Enterprises that use a single IFM partner across 5 or more service categories have reported an average 18% reduction in vendor management overhead, which gives procurement teams a direct cost and control argument for consolidation. This shift also lifts the strategic value of Hard FM, because technical metrics such as HVAC uptime, electrical reliability, and power usage performance are easier to verify and govern than many soft-service outputs at the bid stage. Institutional ownership is expanding across India's office stock, with more than 380 million sq ft of Grade A space carrying REIT potential, and these owners prefer consistent standards across distributed portfolios rather than separate local operating arrangements. As this model becomes standard, smaller firms without national reach, data systems, and compliance depth are likely to lose share in the India integrated facility management market even when they remain locally competitive on price.

Price-led Competition from Unorganized Vendors

Price-led competition from unorganized vendors remains the clearest structural brake on the India integrated facility management market, with smaller operators undercutting organized firms by 15% to 20% by bypassing Provident Fund, Employees' State Insurance, and minimum wage obligations. The pressure is strongest in cleaning, housekeeping, and security, where labour is the main cost input and output quality is often harder for buyers to benchmark objectively during procurement. The problem does not end at contract award, because the visible price gap then shapes renewal discussions and creates fresh pressure on organized firms to accept lower rates on compliant delivery models. India's labour code consolidation could improve the competitive balance over time, but state-level implementation remains uneven, and that keeps enforcement outcomes inconsistent across locations. Even so, large enterprise buyers are slowly shifting from lowest-bid decisions toward total-cost-of-ownership reviews, which should gradually improve the quality mix in the India integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Wider Adoption of Smart Buildings and Predictive Maintenance

- Sustainability-led Demand for Energy, Water and Waste Optimization

- Skilled Workforce Attrition and Wage Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard facility management (FM) is forecast to expand at a 9.47% CAGR through 2031, which places it ahead of the overall growth rate and makes it the strongest service-side growth engine in the India integrated facility management (IFM) market. This acceleration is closely tied to higher technical density in Grade A assets and to data center expansion, with national capacity projected to rise from nearly 1.7 GW at the end of 2025 to more than 4 GW by FY30. That buildout increases demand for MEP services, HVAC management, electrical reliability, power backup support, and 24/7 technical staffing that general service operators cannot easily scale. Asset management services are also gaining a larger role as REIT-led portfolios and GCC campuses shift from periodic maintenance cycles toward lifecycle planning, replacement tracking, and capex-linked stewardship.

Soft FM held 67.19% share of the India IFM market size in 2025, which reflects the large labour base needed for cleaning, catering, office support, and security across India's commercial, hospitality, healthcare, and institutional estate. The segment remains the revenue anchor for many providers because it touches daily occupancy experience and is difficult for large occupiers to internalize across multi-site portfolios. Even so, the service mix inside integrated contracts is gradually shifting, because hard services carry higher value per square foot and support more measurable SLA outcomes than many labour-heavy soft lines. Cleaning is benefiting from mechanization and robotic floor care, while office support and security functions are being upgraded through AI-assisted surveillance and intelligent visitor management, which helps the India IFM industry defend service quality in a price-sensitive environment.

List of Companies Covered in this Report:

- BVG India Limited

- SIS Limited

- Sodexo India Services Private Limited

- Updater Services Limited

- Bluspring Enterprises Limited

- ISS Facility Services India Private Limited

- Krystal Integrated Services Limited

- CBRE South Asia Private Limited

- Jones Lang LaSalle Property Consultants (India) Private Limited

- Cushman & Wakefield India Private Limited

- Compass Group India (Compass Group PLC)

- Colliers International (India) Property Services Private Limited

- Knight Frank (India) Private Limited

- Tenon Facility Management India Private Limited

- Dusters Total Solutions Services Private Limited

- Property Solutions (India) Private Limited

- OCS India

- SMS Integrated Facility Services Private Limited

- Impressions Services Private Limited

- ServiceMax Facility Management Private Limited

- Supreme Facility Management Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Grade A Offices and Mixed-use Campuses

- 4.2.2 Vendor Consolidation Into Integrated and Outcome-based Contracts

- 4.2.3 Wider Adoption of Smart Buildings and Predictive Maintenance

- 4.2.4 Sustainability-led Demand for Energy, Water and Waste Optimization

- 4.2.5 Global Capability Centre Expansion Beyond Tier-1 Hubs

- 4.2.6 Data Centre and Mission-critical Infrastructure Buildout

- 4.3 Market Restraints

- 4.3.1 Price-led Competition From Unorganized Vendors

- 4.3.2 Skilled Workforce Attrition and Wage Inflation

- 4.3.3 Working-capital Stress From Delayed Receivables

- 4.3.4 Utility Reliability and Water-stress Exposure in Critical Assets

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BVG India Limited

- 6.4.2 SIS Limited

- 6.4.3 Sodexo India Services Private Limited

- 6.4.4 Updater Services Limited

- 6.4.5 Bluspring Enterprises Limited

- 6.4.6 ISS Facility Services India Private Limited

- 6.4.7 Krystal Integrated Services Limited

- 6.4.8 CBRE South Asia Private Limited

- 6.4.9 Jones Lang LaSalle Property Consultants (India) Private Limited

- 6.4.10 Cushman & Wakefield India Private Limited

- 6.4.11 Compass Group India (Compass Group PLC)

- 6.4.12 Colliers International (India) Property Services Private Limited

- 6.4.13 Knight Frank (India) Private Limited

- 6.4.14 Tenon Facility Management India Private Limited

- 6.4.15 Dusters Total Solutions Services Private Limited

- 6.4.16 Property Solutions (India) Private Limited

- 6.4.17 OCS India

- 6.4.18 SMS Integrated Facility Services Private Limited

- 6.4.19 Impressions Services Private Limited

- 6.4.20 ServiceMax Facility Management Private Limited

- 6.4.21 Supreme Facility Management Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment