PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066684

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066684

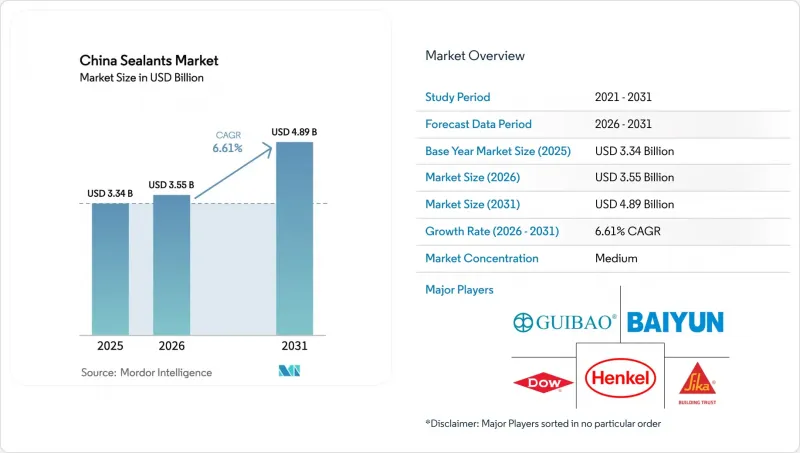

China Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china sealants market size is expected to grow from USD 3.34 billion in 2025 to USD 3.55 billion in 2026 and is forecast to reach USD 4.89 billion by 2031 at 6.61% CAGR over 2026-2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins) and End-User Industry (Aerospace, Automotive and Transportation, Electronics and Semiconductors, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

China Sealants Market Trends and Insights

Green-Building Code Enforcement Accelerates Premium, Low-VOC Sealant Demand

Mandatory national standard GB 30981.1-2025, effective June 2026, tightens limits on VOCs, semi-volatile compounds, biocides, and heavy metals in architectural coatings and accessory materials, forcing producers to reformulate or face higher environmental-protection taxes and provincial audits. Life-cycle assessment requirements in group standard T/CBMF 297-2024 heighten procurement scrutiny for public-sector projects, propelling alcohol-cure silicones and water-based acrylics in curtain-wall and prefabricated-building joints. Complementary frameworks such as GB/T 35609-2025 embed environmental metrics into green-product labeling, accelerating market bifurcation where legacy oxime-cure silicones compete mainly on price in residential retrofit channels. Tier-1 cities are already mandating digital VOC-emission reporting via real-time monitoring, giving an early-mover advantage to companies that invested in low-emission pilot lines. As compliance costs rise, the China Sealants market increasingly rewards vertically integrated suppliers capable of rapid formulation pivots and cradle-to-gate traceability.

Automotive Light-Weighting Drives Multi-Substrate Bonding Shift

China's electric-vehicle segment is migrating from mechanical fasteners to adhesive-intensive aluminum and mixed-material bodies to meet stringent range and efficiency targets. The automotive aluminum-alloy body connection-process market was roughly RMB 86 billion (USD 12 billion) in 2024 and is expected to climb to RMB 230 billion (USD 32 billion) by 2030 as aluminum-body penetration rises toward 40%. Structural polyurethane adhesives are favored for ambient-temperature cure and vibration damping, supporting higher takt times on robotized lines. Flagship EV platforms such as the NIO ET7 feature more than 120 meters of crash-toughened structural adhesive per vehicle, a threefold increase from first-generation models. Domestic Tier-1s co-developing proprietary bonding recipes with automakers shorten design iterations and retain intellectual property in-country, strengthening the technology spine of the China Sealants market.

Volatile Silicone Monomer Pricing Squeezes Margins

Spot prices for dimethyl-cyclosiloxane (DMC) jumped 20% in November 2025 to RMB 13,200 (USD 1,892.88) per ton after monomer producers coordinated 30% output cuts. Hydropower curtailments in Southwest China and higher industrial-silicon costs pushed quotes further to RMB 13,775 (USD 1,975.33) per ton by January 2026. Smaller formulators, lacking long-term contracts or financial hedges, saw gross margins compress by up to 450 basis points. Large integrated players such as Wacker leveraged captive siloxane capacity to buffer cost spikes, widening competitive gaps within the China Sealants market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Warehousing Boom Raises Floor-Joint and Cold-Storage Sealant Use

- Rapid Expansion of China's Commercial Aerospace MRO Ecosystem

- Intensifying Provincial Environmental Audits on Solvent Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone products commanded 41.55% of the China Sealants market share in 2025, supported by proven durability in curtain-wall glazing, facade panels, and photovoltaic modules. Polyurethane's 7.56% forecast CAGR through 2031 is propelled by direct-glazing in new-energy vehicles and by cold-storage insulation panels that demand flexibility at sub-zero temperatures. Epoxy, acrylic, and MS-hybrid chemistries remain growth niches, yet MS-hybrids are adding 80 basis points of share per year thanks to isocyanate-free safety and faster green strength.

Silicone's cost disadvantage widens when D4 intermediates surge, but formulation science, neutral-cure catalysts, adhesion promoters, and UV-stability packages continue to raise performance ceilings. Wacker's Zhangjiagang specialty silicones hub supplies high-purity fluids initially imported from Germany, shortening lead times for electronics encapsulation grades. Domestic challengers, such as Guangzhou Jointas, are promoting MS-hybrids with Shore-A hardness tunable from 20 to 50 and primer-less adhesion to galvanized steel, a compelling proposal in modular-construction factories that switch substrates several times per shift. Over the forecast window, the China sealants market will tilt toward diversified resin portfolios rather than single-chemistry dominance.

List of Companies Covered in this Report:

- 3M

- ACC Silicones (Shenzhen)

- Anabond Limited

- Arkema

- Beijing Oriental Yuhong Waterproof Technology

- Bondchem

- Chengdu Guibao Science and Technology Co., Ltd.

- CHT Germany GmbH

- Dow

- Guangzhou Baiyun Technology Co, Ltd.

- Guangzhou Jointas Chemical Co.

- H.B. Fuller Company

- Hangzhou Zhijiang Advanced Material Co.

- Henkel AG & Co. KGaA

- Huitian Adhesive Co.

- Momentive Performance Materials

- Shin-Etsu Chemical Co.

- Sika AG

- Tonsan Adhesive

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Green-building code enforcement accelerates premium, low-VOC sealant demand

- 4.2.2 Automotive light-weighting drives multi-substrate bonding shift

- 4.2.3 E-commerce warehousing boom raises floor-joint and cold-storage sealant use

- 4.2.4 Rapid expansion of China's commercial aerospace MRO ecosystem

- 4.2.5 Smart-factory adoption spurs demand for one-component UV-curable sealants

- 4.3 Market Restraints

- 4.3.1 Volatile silicone monomer pricing squeezes margins

- 4.3.2 Intensifying provincial environmental audits on solvent emissions

- 4.3.3 Over-capacity in low-grade construction silicones

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive and Transportation

- 5.2.3 Aerospace

- 5.2.4 Electronics and Semiconductors

- 5.2.5 Healthcare

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACC Silicones (Shenzhen)

- 6.4.3 Anabond Limited

- 6.4.4 Arkema

- 6.4.5 Beijing Oriental Yuhong Waterproof Technology

- 6.4.6 Bondchem

- 6.4.7 Chengdu Guibao Science and Technology Co., Ltd.

- 6.4.8 CHT Germany GmbH

- 6.4.9 Dow

- 6.4.10 Guangzhou Baiyun Technology Co, Ltd.

- 6.4.11 Guangzhou Jointas Chemical Co.

- 6.4.12 H.B. Fuller Company

- 6.4.13 Hangzhou Zhijiang Advanced Material Co.

- 6.4.14 Henkel AG & Co. KGaA

- 6.4.15 Huitian Adhesive Co.

- 6.4.16 Momentive Performance Materials

- 6.4.17 Shin-Etsu Chemical Co.

- 6.4.18 Sika AG

- 6.4.19 Tonsan Adhesive

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment