PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066682

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066682

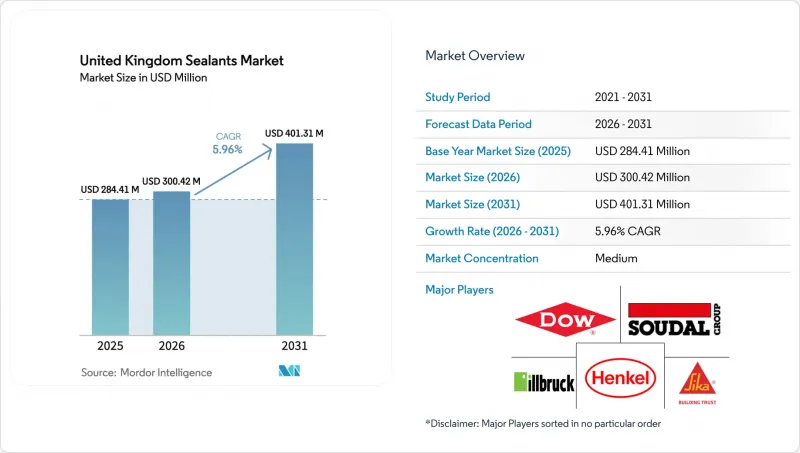

United Kingdom Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom sealants market size is projected to expand from USD 284.41 million in 2025 and USD 300.42 million in 2026 to USD 401.31 million by 2031, registering a CAGR of 5.96% between 2026 and 2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, Polysulfide, Hybrid Silane-Modified Polymer (SMP), and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

United Kingdom Sealants Market Trends and Insights

Growing Demand for Fire-Resistant Sealants in UK High-Rise Refurbishments

The Building Safety Act is transforming fire-rated sealants from optional upgrades to compulsory products across roughly 12,500 high-rise dwellings in England. Intumescent acrylics and silicones must now achieve EN 13501-1 classification and prove compatibility with cavity-barrier systems, shifting procurement toward brands that can present third-party test evidence. Post-Grenfell inquiries traced smoke spread to joint failures, raising client scrutiny and lengthening approval cycles for unproven chemistries. Infrastructure upgrades in rail hubs and airports also require dual fire and acoustic ratings, which narrows the supplier pool and supports premium pricing. Smaller formulators lacking EN-certified lines are ceding share to multinational suppliers that can finance continuous testing, while demand remains concentrated in London and Manchester, where labor and logistics costs already elevate project budgets.

Stricter VOC Regulations Pushing Shift to Hybrid Silane-Terminated Polymers

SI 2012/1715 caps VOC content in construction sealants at 5-10 g/L, and intensified site inspections since 2024 have made compliance visible to contractors. Hybrid SMP grades meet the limit with negligible emissions, cure through ambient moisture, and avoid isocyanate labeling, which makes them the default choice in many framework contracts. Europe holds 44% of global SMP capacity, and the United Kingdom is the region's fastest adopter because public-sector buyers mandate Environmental Product Declarations in tender documents. Suppliers such as Wacker Chemie and KCC Corporation have expanded UK technical teams to train applicators on moisture-sensitive handling. The transition raises costs by 15-25% per liter compared with solvent-borne polyurethane but positions contractors for forthcoming lifecycle-carbon rules that could expedite the exit of legacy solvent systems.

Volatility in Silicon-Metal and MDI Raw-Material Prices

Silicon metal declined 14.98% year-on-year to March 2026 on Chinese oversupply, while European MDI rose 7.9% in February 2026, and aniline rose 18% in Q4 2024. Polyurethane producers, therefore, face margin compression because residential contractors resist full pass-through price increases. Divergent raw-material trends are shifting share toward silicone in premium applications, while polyurethane suppliers are experimenting with TDI blends that raise occupational-exposure risks. Freight disruptions through the Red Sea add 10-14 days to lead times, compelling distributors to carry higher inventories that tie up working capital.

Other drivers and restraints analyzed in the detailed report include:

- Post-Brexit Infrastructure Stimulus Accelerating Construction Sealant Consumption

- NHS Estate Maintenance Backlog Driving Healthcare-Facility Refurbishment

- Skilled Applicator Shortage Causing Project Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone grades accounted for 33.50% of 2025 demand, anchored by EN 15651-certified applications in healthcare and fire-rated facades. Hybrid Silane-Modified Polymer (SMP) products are forecast to grow at a CAGR of 7.12% annually during the forecast period (2026-2031), the fastest among all resins. That rise aligns with contractor preference for one-component, label-free systems that comply with tightening VOC caps. Polyurethane retains relevance in EV battery packs and industrial flooring because of its chemical resistance and adhesion to dissimilar substrates. Acrylic and polysulfide persist in interior decoration and immersion-zone civil works. Regulatory convergence around ISO 11600 and ASTM C920 is elevating performance thresholds, which is accelerating research and development spend on silicone, SMP, and polyurethane while niche chemistries stagnate.

The competitive effects are already visible. Wacker Chemie expanded UK technical support in 2025, and Sika AG introduced Sikaflex-268 PowerCure for rail carriages, aiming to displace polysulfide with faster SMP curing. Smaller formulators focusing on polysulfide now confine their offers to marine and tidal applications where immersion durability still commands a premium. As building-control officers increasingly request EPDs, suppliers that cannot finance lifecycle assessments are losing specification visibility, reinforcing the leadership of vertically integrated silicone and SMP producers.

List of Companies Covered in this Report:

- 3M

- Adshead Ratcliffe & Co Ltd.

- Arkema

- Bond It Group

- DAP Products

- Dow

- Sika Limited

- Fischer UK

- The Sherwin-Williams Company

- Gorilla Glue Company

- Henkel AG & Co. KGaA

- Hodgson Sealants

- illbruck (Tremco CPG)

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Soudal Group

- Tremco Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for fire-resistant sealants in UK high-rise refurbishments

- 4.2.2 Stricter VOC regulations pushing shift to hybrid silane-terminated polymers

- 4.2.3 Post-Brexit infrastructure stimulus accelerating construction sealant consumption

- 4.2.4 Rising electric-vehicle battery-pack sealing needs

- 4.2.5 NHS estate maintenance backlog driving healthcare-facility refurbishment

- 4.3 Market Restraints

- 4.3.1 Volatility in silicon-metal and MDI raw-material prices

- 4.3.2 Skilled applicator shortage causing project delays

- 4.3.3 Competition from prefabricated gasket solutions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Polysulfide

- 5.1.6 Hybrid Silane-Modified Polymer (SMP)

- 5.1.7 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.3.1 Residential

- 5.2.3.2 Commercial

- 5.2.3.3 Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Adshead Ratcliffe & Co Ltd.

- 6.4.3 Arkema

- 6.4.4 Bond It Group

- 6.4.5 DAP Products

- 6.4.6 Dow

- 6.4.7 Sika Limited

- 6.4.8 Fischer UK

- 6.4.9 The Sherwin-Williams Company

- 6.4.10 Gorilla Glue Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Hodgson Sealants

- 6.4.13 illbruck (Tremco CPG)

- 6.4.14 MAPEI S.p.A.

- 6.4.15 RPM International Inc.

- 6.4.16 Sika AG

- 6.4.17 Soudal Group

- 6.4.18 Tremco Incorporated

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment