PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066729

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066729

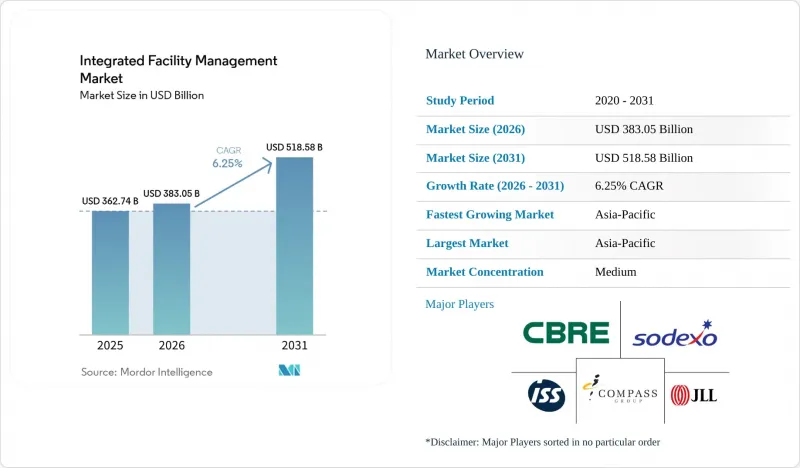

Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the integrated facility management market size was valued at USD 362.74 billion in 2025 and is estimated to grow from USD 383.05 billion in 2026 to reach USD 518.58 billion by 2031, at a CAGR of 6.25% during the forecast period (2026-2031).

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Hospitality, Healthcare, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Integrated Facility Management Market Trends and Insights

Smart Building and Predictive Maintenance Adoption: AI Now Sets the Procurement Floor

AI-enabled monitoring and IoT building systems are changing how integrated facility management is procured and delivered. Uptime and energy performance are now moving from service aspirations into contract obligations in large enterprise accounts. Honeywell reported in April 2025 that 60% of organizations had integrated AI-driven maintenance systems, while 84% of commercial building decision-makers planned to expand AI further. CBRE reported 13% growth in its facility management segment in 2025, supported by data center technical services and local FM deployments linked to smart infrastructure programs. Providers with long-tenure contracts are building asset-level performance baselines that new entrants cannot easily match, which raises switching costs for clients. Siemens expanded this shift in May 2026, launching Asset Performance Advanced, a managed building service that combines predictive failure classification with automated workflow execution for HVAC and building automation systems.

Outsourcing Of Non-Core Workplace and Estate Operations: First-Time Outsourcers Expand the Addressable Market

The integrated facility management (IFM) market is gaining from a broader outsourcing cycle as building systems become harder for occupiers to manage in-house. Mechanical, electrical, air-quality, security, and control systems now require a level of coordination that many occupiers do not maintain internally. JLL reported 9% revenue growth in its Real Estate Management Services segment in the fourth quarter of 2025, supported by workplace management expansion and new client wins in sectors that had relied on self-operated FM models. CBRE also extended its outsourcing platform through the USD 800 million acquisition of J&J Worldwide Services in February 2024, adding federal facilities with long-term fixed-price contracts and institutional-grade service requirements. Mid-market occupiers are adding fresh demand to the integrated facility management market as office footprints are redesigned around hybrid attendance patterns and service flexibility. IFMA reported in 2025 that leading organizations increasingly treat FM as a direct lever for financial, environmental, and workforce outcomes, which is moving procurement attention from operations teams to executive leadership.

Shortage Of Multi-Trade Technical Labor: Supply Gaps Are Becoming Strategic Risks

The integrated facility management (IFM) market is facing a structural labour problem rather than a short hiring cycle. Providers need more electricians, HVAC technicians, control specialists, and compliance staff than current training pipelines can supply. The SFG20 State of Facilities Management 2026 report found that 51% of FM organizations reported staff shortages and 42% reported a significant skills gap, especially in compliance, digital capability, and energy management. JLL projected 2.1 million unfilled skilled trades positions by 2030, with potential economic losses of USD 1 trillion per year if the gap persists. The U.S. Bureau of Labor Statistics projected HVAC technician employment to grow 8.1% and electrician roles to grow 9.5% through 2034, both above the 3.1% average for all occupations. This slows hard FM mobilization in the integrated facility management market while also pushing providers to invest more aggressively in remote diagnostics and predictive maintenance to reduce site-level labour dependence.

Other drivers and restraints analyzed in the detailed report include:

- ESG And Building-Performance Compliance Mandates: Penalties Are Driving Procurement Decisions

- Data Center and Life Sciences Capacity Expansion: Specialized FM Becomes a Barrier to Entry

- Cybersecurity Liability from Connected Building Stacks: OT-IT Convergence Introduces Systemic Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management (FM) held 61.73% of the integrated facility management (IFM) market share in 2025. Its lead reflects the long-standing outsourcing of cleaning, security, catering, reception, and office support across commercial, institutional, and hospitality portfolios. These services are usually the first to move outside the client organization because they are easier to standardize across multiple sites. Office support and security continue to carry the largest weight within soft FM, while cleaning is moving through a technology upgrade cycle with greater use of robotic tools and occupancy-based scheduling. Compass Group reported FY2025 revenue of USD 46.1 billion and net new business growth of 4-5% for the fourth straight year, which supports the durability of institutional catering within the IFM market.

Hard FM is projected to expand at a 6.83% CAGR through 2031, making it the fastest-growing service category in the IFM market. Growth is being driven by data center critical-systems management, energy-system retrofits, and mechanical, electrical, and plumbing servicing in technically demanding environments. Asset management, MEP services, and HVAC maintenance remain the largest hard FM activities because aging infrastructure and compliance cycles leave limited room for deferred work. This shift shows where pricing power is building in the integrated facility management industry, since performance-linked hard FM contracts tied to uptime, energy use, and carbon outcomes carry more value than task-based service schedules. Mitie strengthened that position in May 2026 through a GBP 26 million (USD 33 million) M&E maintenance and energy management contract with AstraZeneca at its Macclesfield pharmaceutical campus.

Geography Analysis

Asia-Pacific held 40.76% of the integrated facility management market share in 2025 and is projected to grow at a 7.24% CAGR through 2031. The region combines mature outsourcing markets such as Japan, Australia, and Singapore with high-growth corridors in China, India, and Southeast Asia. Japan is showing especially strong momentum because integrated FM contracts are helping occupiers handle labour pressure, tighter governance needs, and growing ESG reporting expectations. Azbil expanded the use of AI-enabled FM platforms across Japanese facilities in 2024, while NTT Facilities also advanced IoT-based monitoring deployments in the same year. The integrated facility management market in Asia-Pacific is also benefiting from new-build demand tied to commercial real estate growth, smart-city programs, and data center pipelines in Singapore and India.

North America and Europe remain the highest-margin regional blocks in the integrated facility management (IFM) market. European demand is being supported by the need for verified facilities data, stronger carbon accountability, and a clear preference for fewer suppliers across large portfolios. In the United Kingdom, ISS secured an annual IFM contract with a major government department that starts in the second quarter of 2026, reinforcing the role of public-sector outsourcing in regional demand. Germany remains the region's highest-value single-country market, and Apleona extended its Deutsche Bank IFM agreement through December 2029 across 825 properties and 1.9 million sqm in Germany and Luxembourg. In North America, procurement is being reshaped by building-performance rules such as Local Law 97 in New York City and Title 24 in California, which favour providers that can deliver portfolio-level emissions accountability.

The Middle East is one of the fastest-moving sub-regions in the IFM market because of Saudi Arabia's project pipeline, UAE smart-city investment, and tourism-led hospitality demand. Farnek reported AED 58 million (USD 15.8 million) in first-quarter 2026 FM contract wins covering Equinix data centers and UAE education institutions, which shows the breadth of current demand in the Gulf Cooperation Council. Africa remains at an earlier stage, with South Africa, Nigeria, and Egypt leading activity as commercial property growth increases institutional outsourcing demand despite technical labour constraints. South America is centered on Brazil and Argentina, where multinational occupiers are looking for more consistent service standards across expanding commercial real estate portfolios.

- ISS A/S

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Sodexo S.A.

- Compass Group PLC

- Cushman & Wakefield plc

- Mitie Group plc

- Aramark

- ABM Industries Incorporated

- Apleona GmbH

- ATALIAN Holding Development and Strategy

- BGIS Global Integrated Solutions Canada LP

- Dussmann Group

- ENGIE

- EMCOR Group, Inc.

- OCS Group Holdings Limited

- GDI Integrated Facility Services Inc.

- VINCI Facilities

- Coor Service Management Holding AB

- Facilicom Group N.V.

- BVG India Limited

- AEON DELIGHT CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing of Non-core Workplace and Estate Operations

- 4.2.2 Smart Building and Predictive Maintenance Adoption

- 4.2.3 ESG and Building-Performance Compliance Mandates

- 4.2.4 Demand for Single Accountability Across Multi-site Portfolios

- 4.2.5 Data Center and Life Sciences Capacity Expansion

- 4.2.6 Outcome-based FM Contracts Linked to Carbon and Uptime KPIs

- 4.3 Market Restraints

- 4.3.1 Shortage of Multi-trade Technical Labor

- 4.3.2 Cybersecurity Liability from Connected Building Stacks

- 4.3.3 Margin Compression from Inflation Reset Lag in FM Contracts

- 4.3.4 Tariff and Lead-time Volatility in HVAC and Controls Supply

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End-user Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 India

- 5.3.4.4 South Korea

- 5.3.4.5 Australia

- 5.3.4.6 Southeast Asia

- 5.3.4.7 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Nigeria

- 5.3.6.4 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ISS A/S

- 6.4.2 CBRE Group, Inc.

- 6.4.3 Jones Lang LaSalle Incorporated

- 6.4.4 Sodexo S.A.

- 6.4.5 Compass Group PLC

- 6.4.6 Cushman & Wakefield plc

- 6.4.7 Mitie Group plc

- 6.4.8 Aramark

- 6.4.9 ABM Industries Incorporated

- 6.4.10 Apleona GmbH

- 6.4.11 ATALIAN Holding Development and Strategy

- 6.4.12 BGIS Global Integrated Solutions Canada LP

- 6.4.13 Dussmann Group

- 6.4.14 ENGIE

- 6.4.15 EMCOR Group, Inc.

- 6.4.16 OCS Group Holdings Limited

- 6.4.17 GDI Integrated Facility Services Inc.

- 6.4.18 VINCI Facilities

- 6.4.19 Coor Service Management Holding AB

- 6.4.20 Facilicom Group N.V.

- 6.4.21 BVG India Limited

- 6.4.22 AEON DELIGHT CO., LTD.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment