PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063878

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063878

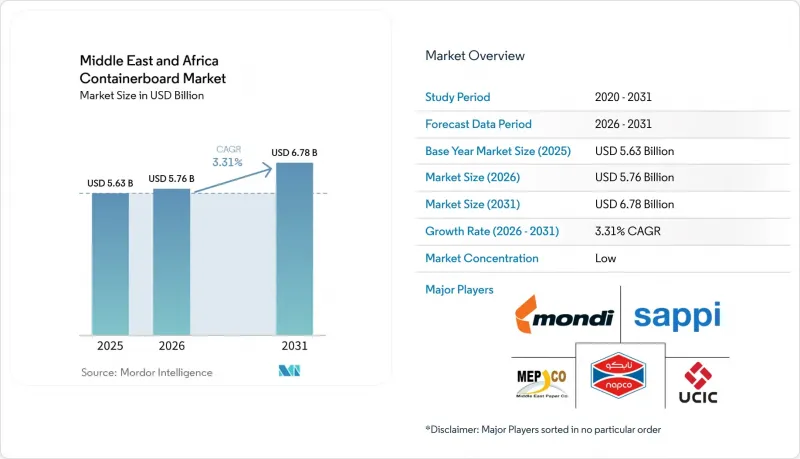

Middle East And Africa Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east and Africa containerboard market size is projected to expand from USD 5.63 billion in 2025 and USD 5.76 billion in 2026 to USD 6.78 billion by 2031, registering a CAGR of 3.31% between 2026 and 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East, South Africa, Egypt, Nigeria, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Containerboard Market Trends and Insights

E-Commerce and Omnichannel Parcel Growth

Online retail is changing corrugated demand in the GCC faster than broader output indicators would usually suggest, and the Middle East and Africa containerboard market is now seeing a clearer shift toward fulfillment-driven packaging demand. Saudi Arabia's non-oil private sector PMI remained above 53 for most of 2025, indicating sustained activity in commerce and logistics, which typically consume large volumes of corrugated packaging. The more meaningful change is in parcel design, because e-commerce operators in Saudi Arabia and the UAE are requesting right-sized, die-cut corrugated formats that reduce cubic weight for last-mile deliveries. That requirement is lifting demand for lightweight fluting media and stronger testliners simultaneously, which is one reason the Middle East and Africa containerboard market is showing faster momentum in flutings than in more mature grades. Working capital pressure among corrugators has at times slowed the conversion of parcel demand into actual board offtake, so mills that can support customers on service, flexibility, and credit terms are in a better position to hold share.

Food Delivery and Fresh-Produce Export Intensity

Agricultural packaging remains one of the most resilient demand pools in the Middle East and Africa containerboard market, as fresh-produce exports create concentrated, recurring demand for high-performance corrugated trays and boxes. South Africa's citrus and pome fruit export cycle, which peaks from February to July, drives predictable demand for packaging that meets EU phytosanitary and food-contact requirements while also protecting produce during long transit. Sappi reported that packaging and specialty paper sales volumes rose 8% year on year in FY2025, with improved containerboard demand driven mainly by a strong citrus season. MPact also reported strong volume growth in containerboard and agricultural packaging, and described the agricultural segment as structurally attractive due to export-oriented growth. Because these mills plan around Northern Hemisphere retail and harvest calendars as much as domestic cycles, the Middle East and Africa containerboard market benefits from export-linked food packaging that is not fully tied to local consumer sentiment.

Imported OCC, Pulp, And Kraft Liner Price Volatility

Raw material risk remains the clearest constraint on the Middle East and Africa containerboard market because the region has almost no domestic virgin wood fiber pulp base and still depends heavily on imported OCC bales and kraft liner. This exposure became more visible in 2025 when higher recovered paper costs hit margins even as shipment volumes improved for major regional players. MPact said recovered paper prices rose significantly in the first half of 2025, and that cost pressure contributed to a 14.5% decline in EBITDA even though containerboard sales volumes increased 20.3% in the same period. The feedback loop is important because new recycled machine capacity improves local availability of board, but it can also intensify competition for the same OCC pool and raise input prices again. That means the Middle East and Africa containerboard market can gain from domestic scale while still struggling to convert that scale into stable margin expansion.

Other drivers and restraints analyzed in the detailed report include:

- Plastic Substitution and Packaging EPR Momentum

- Lightweight Low-Basis-Weight Board Upgrades

- Red Sea and Gulf Shipping-Disruption Cost Shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 53.7% of the Middle East and Africa containerboard market share in 2025, which reflects the region's practical dependence on OCC-based testliner and fluting in a fiber-deficient environment. The dominance of recycled grades is reinforced by the production profile in Saudi Arabia, the UAE, and Kuwait, where domestic containerboard capacity is centered on recycled fiber rather than virgin pulp. Cost discipline and sustainability requirements are both supporting this pattern, so buyers often see recycled board as the most workable balance between availability and economics. That is why the Middle East and Africa containerboard market continues to rely on recovered fiber even when imported OCC costs become more volatile.

Virgin fibers are projected to grow at a 4.4% CAGR through 2031, and that faster pace reflects a quality premium rather than a broad shift away from recycled grades. Mondi's Duino mill in Italy added 420,000 tonnes per year of recycled containerboard capacity designed to serve European customers and international routes, including flows connected to the Middle East and Africa containerboard market, which underlines the continued competitive pressure from well-capitalized exporters. Food-contact applications, stronger burst-strength needs, and pharma-adjacent packaging still favor virgin-based linerboard, where recycled input cannot deliver consistent performance at scale. Multinational customers are also placing greater weight on chain-of-custody and certification standards, and that creates a specification gap for some regional recycled-fiber suppliers.

List of Companies Covered in this Report:

- Mondi plc

- Mpact Limited

- Middle East Paper Company

- Arab Paper Manufacturing Company

- Sappi Limited

- United Carton Industries Company

- Arabian Packaging Co. LLC

- Industrial Development Company s.a.l.

- Napco National CJSC

- Obeikan Investment Group

- Gulf Paper Manufacturing Company K.S.C.

- Omani Packaging Company SAOG

- Queenex Corrugated Carton Factory

- RAK Packaging Company Ltd.

- UNIPAKNILE Ltd.

- Cairo Egyptian Packaging and Containers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce and Omnichannel Parcel Growth

- 4.2.2 Food Delivery and Fresh-Produce Export Intensity

- 4.2.3 Plastic Substitution and Packaging EPR Momentum

- 4.2.4 Lightweight Low-Basis-Weight Board Upgrades

- 4.2.5 AFCFTA-Led Need for Stronger Transit Packaging

- 4.2.6 Digital Print Adoption Enabling High-Margin Short Runs

- 4.3 Market Restraints

- 4.3.1 Imported OCC, Pulp, and Kraft Liner Price Volatility

- 4.3.2 Water Scarcity and Mill-Effluent Constraints

- 4.3.3 Red Sea and Gulf Shipping-Disruption Cost Shocks

- 4.3.4 Water-Use Restrictions Affecting Pulp Mills

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 Middle East

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Turkey

- 5.4.1.4 Rest of Middle East

- 5.4.2 Africa

- 5.4.2.1 South Africa

- 5.4.2.2 Egypt

- 5.4.2.3 Nigeria

- 5.4.2.4 Rest of Africa

- 5.4.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mondi plc

- 6.4.2 Mpact Limited

- 6.4.3 Middle East Paper Company

- 6.4.4 Arab Paper Manufacturing Company

- 6.4.5 Sappi Limited

- 6.4.6 United Carton Industries Company

- 6.4.7 Arabian Packaging Co. LLC

- 6.4.8 Industrial Development Company s.a.l.

- 6.4.9 Napco National CJSC

- 6.4.10 Obeikan Investment Group

- 6.4.11 Gulf Paper Manufacturing Company K.S.C.

- 6.4.12 Omani Packaging Company SAOG

- 6.4.13 Queenex Corrugated Carton Factory

- 6.4.14 RAK Packaging Company Ltd.

- 6.4.15 UNIPAKNILE Ltd.

- 6.4.16 Cairo Egyptian Packaging and Containers

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment