PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064392

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064392

Benelux Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

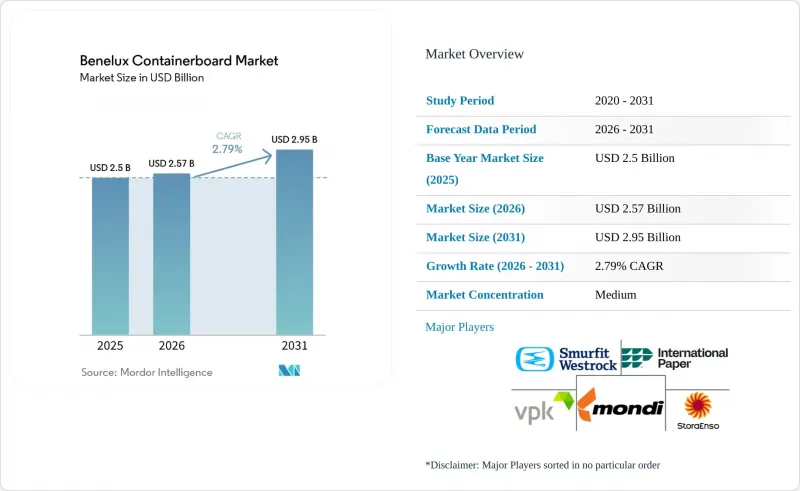

According to Mordor Intelligence, the benelux containerboard market size is expected to grow from USD 2.50 billion in 2025 to USD 2.57 billion in 2026 and is forecast to reach USD 2.95 billion by 2031 at 2.79% CAGR over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Benelux Containerboard Market Trends and Insights

Food Service And Grocery Fiber Substitution Under PPWR

The PPWR Article 5 PFAS restriction, effective August 12, 2026, is pushing food service operators and grocery supply chains to move away from fluoropolymer-coated plastic and laminated paper formats toward fiber-based transit packaging more quickly. The same regulation also prohibits selected single-use plastic packaging for fresh produce and hospitality food service from January 1, 2030, while cardboard boxes are excluded from the 40% transport packaging reuse target, which gives corrugated formats a clearer regulatory position than reusable plastic crate alternatives. Sabert launched its PFAS-free PulpUltra range across Europe in January 2026 and directly linked the move to PPWR Article 5 compliance, showing that the substitution cycle is already underway before the enforcement date. Belgium and the Netherlands are major hubs for food processing, retail, and hospitality distribution, so the pipeline for packaging reformulation is deeper here than in many other EU markets. That shifts food transit packs from a secondary source of board demand into an active redesign area for the Benelux containerboard market over the next few years. It also means demand is likely to be pulled forward into 2026-2028 instead of building gradually across the whole forecast period.

Benelux E-Commerce Parcel Density Supporting Box Throughput

The Netherlands' online trade surpassed EUR 36 billion (USD 40.6 billion) in 2024, and that scale continues to support high parcel throughput across the Benelux containerboard market. The Randstad corridor accounted for 62% of Dutch corrugated demand, which gives local box plants shorter runs, faster changeovers, and better utilization than many comparable Western European clusters. Secondary e-commerce packaging volumes for paper-based void fill and kraft paper materials in Western Europe are growing at 3.9% annually, which directly supports testliner and fluting demand at the mill level. VPK Group's new corrugator at Erembodegem lifted board capacity from 100 million m2 to 170 million m2, which shows that established regional players are still investing behind e-commerce demand. The Netherlands also ranked first in the EU for circular material use at 32.7%, which encourages online retailers to specify recycled-content packaging and raises the quality bar for recovered fiber supply. Together, those conditions keep parcel activity a near-term volume support for the Benelux containerboard market even as box design becomes more material efficient.

Energy And Recovered Paper Cost Volatility

Recycled testliner, the dominant grade by volume in the Benelux containerboard market, carries around 68% dependence on natural gas as a primary energy source, which leaves it highly exposed to TTF gas movements. In 2026, the Dutch TTF benchmark rose by more than 60% from the low EUR 30 (USD 33.8) per MWh to above EUR 68 (USD 76.7) per MWh, and each EUR 10 (USD 11.2) per MWh increase can raise testliner production costs by up to EUR 20 (USD 22.5) per tonne. OCC prices in the Rotterdam area also fluctuated between EUR 80 (USD 90.2) and EUR 140 (USD 158.01) per tonne during 2024 and 2025, making raw material planning difficult for non-integrated converters. That double cost pressure limits spending on coating reformulation, recyclability certification, and other upgrades that are becoming more important under PPWR. It also raises the pressure on mid-tier independents that do not have the same hedging and multi-mill balancing options as integrated groups. As a result, the Benelux containerboard market faces a cost-side squeeze that can slow investment even when end-market demand remains stable.

Other drivers and restraints analyzed in the detailed report include:

- High Paper And Cardboard Recovery Rates Supporting Recycled Fiber Supply

- Port-Centric Export Flows Supporting Heavy-Duty Containerboard Demand

- European Containerboard Overcapacity And Margin Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 62.71% of the Benelux containerboard market share in 2025, while the Benelux containerboard market size for virgin fibers is projected to expand at 3.04% CAGR between 2026 and 2031. That split shows a market where recycled grades still dominate, but cost inflation is changing how buyers compare performance and price. When gas prices lift recycled testliner conversion costs, procurement teams are more willing to shift selected volumes toward virgin-fiber grades for moisture-sensitive and export-critical uses. Stora Enso stated in its Q2 2025 presentation that kraftliner pricing held firmer than recycled grades during periods of operating-rate pressure, which fits the grade pattern seen across the Benelux containerboard market.

Belgium's 107.7% industrial paper and cardboard recycling rate in 2024 keeps domestic OCC supply structurally strong and explains why recycled fibers still hold the leading position. Even so, secondary fiber still faces performance limitations in heavy export applications, such as chemical transit packaging, agricultural machinery, and precision goods moving through the ARRRA corridor. That leaves virgin-fiber grades with a durable role where board consistency and moisture resistance cannot vary. Investments in better fiber cleaning and stock preparation should narrow the performance gap over time, but the premium for virgin specifications is likely to remain in the Benelux containerboard market through 2031.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- VPK Group NV

- Stora Enso Oyj

- International Paper Company

- Mondi plc

- Sociedad Anonima Industrias Celulosa Aragonesa

- Prinzhorn Holding GmbH

- Klingele Paper & Packaging SE & Co. KG

- Papierfabrik Palm GmbH & Co. KG

- Billerud Aktiebolag (publ)

- Svenska Cellulosa Aktiebolaget SCA (publ)

- Progroup AG

- LEIPA Georg Leinfelder GmbH

- Papierfabrik Adolf Jass GmbH & Co. KG

- Norske Skog ASA

- Model Holding AG

- Pacapime NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food Service and Grocery Fiber Substitution Under PPWR

- 4.2.2 Benelux E-Commerce Parcel Density Supporting Box Throughput

- 4.2.3 High Paper and Cardboard Recovery Rates Supporting Recycled Fiber Supply

- 4.2.4 Port-Centric Export Flows Supporting Heavy-Duty Containerboard Demand

- 4.2.5 PFAS-Free Barrier Redesign Favoring Fiber-Based Transit Packs

- 4.2.6 Lightweight Box Engineering Increasing High-Performance Fluting Intensity

- 4.3 Market Restraints

- 4.3.1 Energy and Recovered Paper Cost Volatility

- 4.3.2 European Containerboard Overcapacity and Margin Pressure

- 4.3.3 PPWR Empty-Space Caps Lowering Board Intensity per Shipment

- 4.3.4 Reusable Crate Lock-In in Fresh Produce Logistics

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 VPK Group NV

- 6.4.3 Stora Enso Oyj

- 6.4.4 International Paper Company

- 6.4.5 Mondi plc

- 6.4.6 Sociedad Anonima Industrias Celulosa Aragonesa

- 6.4.7 Prinzhorn Holding GmbH

- 6.4.8 Klingele Paper & Packaging SE & Co. KG

- 6.4.9 Papierfabrik Palm GmbH & Co. KG

- 6.4.10 Billerud Aktiebolag (publ)

- 6.4.11 Svenska Cellulosa Aktiebolaget SCA (publ)

- 6.4.12 Progroup AG

- 6.4.13 LEIPA Georg Leinfelder GmbH

- 6.4.14 Papierfabrik Adolf Jass GmbH & Co. KG

- 6.4.15 Norske Skog ASA

- 6.4.16 Model Holding AG

- 6.4.17 Pacapime NV

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment