PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065458

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065458

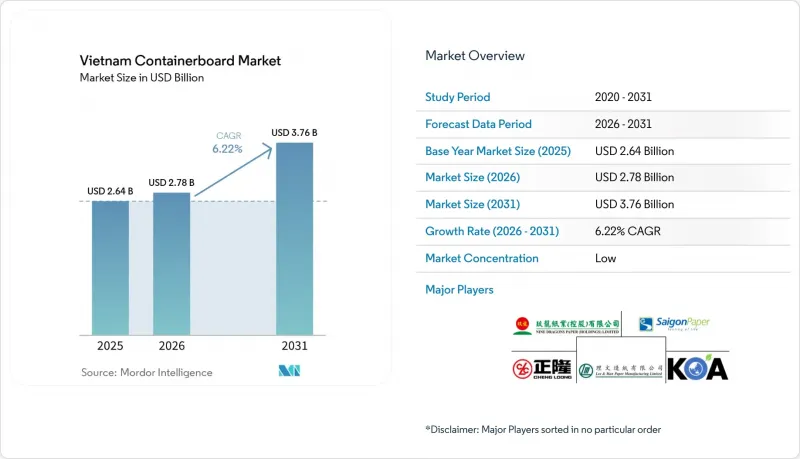

Vietnam Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vietnam containerboard market size was valued at USD 2.64 billion in 2025 and estimated to grow from USD 2.78 billion in 2026 to reach USD 3.76 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031).

This report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Containerboard Market Trends and Insights

E-Commerce Parcel Expansion And Last-Mile Box Intensity

Vietnam's leading e-commerce platforms generated VND 148.6 trillion (USD 5.7 billion) in gross merchandise value in Q1 2026, while sales volume reached 1.14 billion items, up 47% and 20% year over year, respectively. Vietnam's domestic e-commerce market reached USD 31 billion in 2025, placing the country among the world's top 10 and ASEAN's top 3 online retail markets. The important shift in the Vietnam containerboard market is that fulfillment is moving toward more individually boxed, better-protected shipments, which increases corrugated board usage per order even as item counts grow more slowly than sales value. This pattern is strongest in Ho Chi Minh City, Hanoi, and Binh Duong, where parcel density, warehousing, and last-mile activity are most concentrated. With the National E-commerce Development Master Plan for 2026-2030 targeting annual online retail growth of 15%-20%, the Vietnam containerboard market is set to receive a steady flow of shipment-driven demand over the next several years.

Export Manufacturing Relocation Boosting Industrial Carton Demand

Vietnam's manufacturing sector grew 10.6% in 2025, the strongest industrial output growth in 7 years, while electronics and computers exceeded USD 100 billion in exports, and textiles reached USD 46 billion in exports. A survey of Japanese firms showed that 56.9% of respondents in Vietnam planned capacity expansion over the next 1-2 years, the highest expansion intent rate in ASEAN. For the Vietnam containerboard market, this matters because each new factory adds several layers of packaging demand, including packaging for components, intermediate goods, and export master cartons. Electronics assembly also requires stronger corrugated formats, often using 3-layer and 5-layer box structures, which increases demand for higher-performance kraftliner and fluting grades. As more export-oriented production shifts to northern and southern industrial provinces, the Vietnam containerboard market continues to move toward a more industrial, specification-driven demand base.

OCC And Pulp Cost Volatility Squeezing Converter Margins

Vietnam-bound mills were paying USD 195-200 per ton for US double-sorted OCC in late 2024 before later price declines changed procurement economics across Southeast Asia. China's recycled pulp import restrictions, introduced in October 2025, disrupted the regional OCC-to-pulp chain and altered buying patterns for imported recovered fiber. Large integrated mills can handle this pressure better because they have scale, broader inventories, and stronger pricing leverage than smaller mills and converters. Vietnam's Pulp and Paper Association said domestic collection met only 56% of OCC demand in 2025, leaving the remaining 44% exposed to global recovered paper and freight swings. That exposure remains the biggest near-term brake on the Vietnam containerboard market because cost movements can pass through the supply chain faster than selling prices can be reset.

Other drivers and restraints analyzed in the detailed report include:

- Food And Beverage Cold-Chain And Modern Retail Expansion

- Plastic Substitution And EPR Compliance Favoring Fiber Packaging

- Import Dependence For Virgin Fiber And Premium Kraftliner Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 68.11% of the Vietnam containerboard market share in 2025, keeping them firmly in the leading position, as OCC-based board remained the most economical option for standard corrugated grades. Over 80% of local production historically relied on recovered paper feedstock, so recycled furnish stayed central to mill economics and converter sourcing patterns. Vietnam's domestic OCC recovery rate improved from 46% in 2021 to 58% in 2024, reducing but not eliminating import dependence for recycled fiber supply. Asia's total OCC capacity is expected to grow by 4.5 million tons by 2028, with Vietnam contributing close to half of that expansion, strengthening the country's role as a regional secondary fiber processor.

Virgin fibers accounted for 31.89% in 2025, and this segment of the Vietnam containerboard market is projected to grow at a 6.74% CAGR through 2031. Electronics and semiconductor assembly in provinces such as Thai Nguyen and Bac Ninh require packaging with more stable compression strength and lower moisture sensitivity, which supports demand for premium linerboard grades. Multinational buyers are also pushing local suppliers to increase recycled content because of Scope 3 reporting, but their packaging specifications still require performance standards that often favor virgin-furnish board. That conflict keeps a premium-grade supply gap in place and supports further investment interest in virgin-capable assets. The Vietnam containerboard industry is therefore moving toward a more mixed furnish structure, even though recycled board remains the largest base.

List of Companies Covered in this Report:

- Vina Kraft Paper Co., Ltd.

- Cheng Loong Binh Duong Paper Co., Ltd.

- Vietnam Lee & Man Paper Manufacturing Limited

- Nine Dragons Paper (Holdings) Limited

- Kraft of Asia Paperboard & Packaging Co., Ltd.

- Saigon Paper Corporation

- Dong Hai Ben Tre Joint Stock Company

- Miza Corporation

- HHP Global Joint Stock Company

- Minhan Paper Joint Stock Company

- Dong Tien-Long An Paper Joint Stock Company

- Vina Corrugated Packaging Co., Ltd.

- Bien Hoa Packaging Joint Stock Company

- Settsu Carton Vietnam Corporation

- Ojitex (Vietnam) Company Limited

- Song Lam Trading & Packaging Production Co., Ltd.

- Khang Thanh Manufacturing Co., Ltd.

- HC Packaging Vietnam Company Limited

- Starprint Vietnam Joint Stock Company

- United Packaging Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Parcel Expansion and Last-Mile Box Intensity

- 4.2.2 Export Manufacturing Relocation Boosting Industrial Carton Demand

- 4.2.3 Food and Beverage Cold-Chain and Modern Retail Expansion

- 4.2.4 Plastic Substitution and EPR Compliance Favoring Fiber Packaging

- 4.2.5 Scope 3 Procurement Rules Favoring Lightweight Local Recycled Board

- 4.2.6 AI-Led Box Optimization Improving Yield for Short-Run Orders

- 4.3 Market Restraints

- 4.3.1 OCC and Pulp Cost Volatility Squeezing Converter Margins

- 4.3.2 Import Dependence for Virgin Fiber and Premium Kraftliner Grades

- 4.3.3 Monsoon Humidity Weakening Compression Strength in Storage and Transit

- 4.3.4 Export-Market ESG Traceability and Carbon Disclosure Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Vina Kraft Paper Co., Ltd.

- 6.4.2 Cheng Loong Binh Duong Paper Co., Ltd.

- 6.4.3 Vietnam Lee & Man Paper Manufacturing Limited

- 6.4.4 Nine Dragons Paper (Holdings) Limited

- 6.4.5 Kraft of Asia Paperboard & Packaging Co., Ltd.

- 6.4.6 Saigon Paper Corporation

- 6.4.7 Dong Hai Ben Tre Joint Stock Company

- 6.4.8 Miza Corporation

- 6.4.9 HHP Global Joint Stock Company

- 6.4.10 Minhan Paper Joint Stock Company

- 6.4.11 Dong Tien-Long An Paper Joint Stock Company

- 6.4.12 Vina Corrugated Packaging Co., Ltd.

- 6.4.13 Bien Hoa Packaging Joint Stock Company

- 6.4.14 Settsu Carton Vietnam Corporation

- 6.4.15 Ojitex (Vietnam) Company Limited

- 6.4.16 Song Lam Trading & Packaging Production Co., Ltd.

- 6.4.17 Khang Thanh Manufacturing Co., Ltd.

- 6.4.18 HC Packaging Vietnam Company Limited

- 6.4.19 Starprint Vietnam Joint Stock Company

- 6.4.20 United Packaging Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment