PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064384

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064384

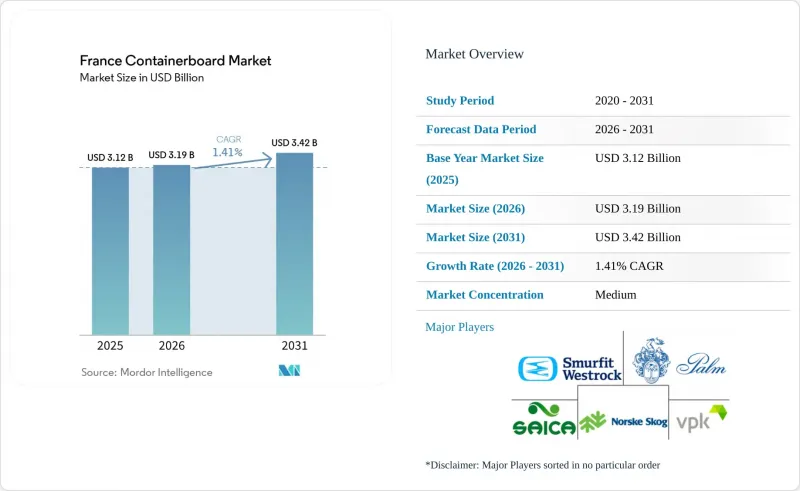

France Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the france containerboard market size is projected to expand from USD 3.12 billion in 2025 and USD 3.19 billion in 2026 to USD 3.42 billion by 2031, at a CAGR of 1.41% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Containerboard Market Trends and Insights

Plastic-To-Fiber Substitution Under AGEC And PPWR

France's AGEC framework and the EU Packaging and Packaging Waste Regulation adopted in 2025 remain the clearest medium-term support for the France containerboard market. Decree No. 2022-748 requires producers and importers above the stated thresholds to disclose recyclability characteristics and recycled-content percentages from January 1, 2025, thereby making packaging composition more visible to buyers and regulators. The same policy direction increases the commercial appeal of recyclable fiber grades in secondary and transit packaging, especially where plastic formats face weaker compliance economics. It is also expanding the addressable space for higher-value grades, such as white-top testliner and coated containerboard, in food, cosmetics, and other presentation-sensitive uses. This keeps regulatory demand support in place even while the near-term volume picture for the France containerboard market remains restrained.

E-Commerce And Shelf-Ready Packaging Optimization

Online retail continues to support the France containerboard market because corrugated use per shipment is higher than in traditional store-led distribution. E-commerce accounted for 13% of French retail sales in 2025, and parcel volumes exceeded 1 billion units, while packaging intensity per shipment was up to 60% above in-store requirements. VPK Group has already aligned part of its Alizay strategy with that demand by deploying a high-definition digital printing platform for fanfold corrugated formats used in right-sized shipping. Shelf-ready packaging is also gaining ground in French food retail, and that shift favors higher-specification liner grades that combine better print performance with recyclability. Over time, this channel mix is likely to support value growth in the France containerboard market more than simple tonnage growth.

European Recycled Containerboard Overcapacity

European supply additions have outpaced demand recovery, and this remains the main brake on the French containerboard market. Industry reporting shows that containerboard operating rates across Europe fell below historical norms after 2022 as new capacity arrived before the market had fully recovered from destocking. In France, the Alizay and Golbey start-ups intensified domestic competition in recycled grades and kept brown corrugated case material prices under pressure through 2025. Norske Skog confirmed that Golbey PM1 posted negative EBITDA during the ramp-up phase in 2025 because lower sales prices were only partly offset by lower OCC costs. This means the France containerboard market is unlikely to regain healthier pricing conditions until demand improves materially or more capacity exits the broader European system.

Other drivers and restraints analyzed in the detailed report include:

- Food And Beverage Corrugated Demand Resilience

- Alizay And Golbey Capacity Reshaping Domestic Supply

- EPR, EUDR, And Traceability Cost Stack

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 58.41% of the French containerboard market share in 2025, supported by France's established recovered-paper system and the usual cost advantage that recycled feedstock provides under normal conditions. Recycled grades remain central to the French containerboard industry because testliners and corrugating media still form the core of supply for food, retail, and e-commerce corrugated applications. The rapid start-up of Alizay and Golbey increased the domestic supply of recycled containerboard and prolonged price pressure on brown grades during 2025. Blue Paper SAS also showed how mid-sized mills are adjusting by changing procurement and transport choices, after adopting river transport for recovered paper shipments in partnership with Voies Navigables de France in April 2026.

Virgin fibers are projected to grow at a 1.68% CAGR in the France containerboard market size outlook through 2031, even though they remained the smaller material segment in 2025. That growth is tied to stronger demand for premium kraftliner in e-commerce outer boxes and shelf-facing applications where strength, print quality, and lower basis weight matter more than lowest-cost input selection. Smurfit Westrock described its Facture site in France as one of the group's largest and lowest-cost kraftliner mills globally, providing a useful platform for premium linerboard supply. EUDR-related traceability requirements can also make sourcing and documenting some non-EU virgin-fiber imports less straightforward. That could leave French and other EU producers with certified supply chains in a stronger position as buyers place more weight on traceability and compliance.

List of Companies Covered in this Report:

- Saica Group

- VPK Group

- Smurfit Westrock plc

- Norske Skog ASA

- Palm Group

- Papeteries Palm SAS

- International Paper Company

- Blue Paper SAS

- Klingele Paper & Packaging Group

- Cartonnerie Gondardennes

- CGW Packaging Group

- Lacaux Freres

- Gemdoubs SAS

- NorPaper SAS

- Allard Emballages

- Seyfert Packaging SAS

- Papeterie de Giroux

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Plastic-to-fiber substitution under AGEC and PPWR

- 4.2.2 Food and beverage corrugated demand resilience

- 4.2.3 E-commerce and shelf-ready packaging optimization

- 4.2.4 Alizay and Golbey capacity reshaping domestic supply

- 4.2.5 Biomass-led decarbonized mill economics

- 4.2.6 Rising Demand for Sustainable Packaging Solutions

- 4.3 Market Restraints

- 4.3.1 European recycled containerboard overcapacity

- 4.3.2 EPR, RDUE, and traceability cost stack

- 4.3.3 Energy-price volatility and weak industrial output

- 4.3.4 Margin Pressure From Imported Brown Recycled Fiber

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Saica Group

- 6.4.2 VPK Group

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Norske Skog ASA

- 6.4.5 Palm Group

- 6.4.6 Papeteries Palm SAS

- 6.4.7 International Paper Company

- 6.4.8 Blue Paper SAS

- 6.4.9 Klingele Paper & Packaging Group

- 6.4.10 Cartonnerie Gondardennes

- 6.4.11 CGW Packaging Group

- 6.4.12 Lacaux Freres

- 6.4.13 Gemdoubs SAS

- 6.4.14 NorPaper SAS

- 6.4.15 Allard Emballages

- 6.4.16 Seyfert Packaging SAS

- 6.4.17 Papeterie de Giroux

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment