PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064395

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064395

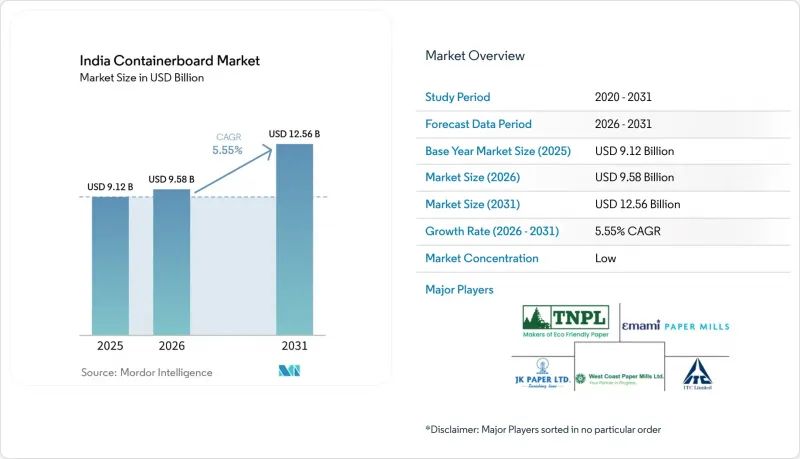

India Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india containerboard market size is expected to increase from USD 9.12 billion in 2025 to USD 9.58 billion in 2026 and reach USD 12.56 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Containerboard Market Trends and Insights

Rising E-Commerce And Quick-Commerce Corrugated Demand

India's quick-commerce sector reached USD 3.35 billion in gross merchandise value in 2024 and is projected to grow to USD 8.83 billion by 2028 at a 27.42% CAGR, which is reshaping packaging demand across urban fulfillment networks. Blinkit operated more than 1,500 dark stores across more than 100 cities in 2025, while Zepto and Swiggy Instamart had also scaled to dense dark-store networks, which widened the addressable base for short-cycle corrugated consumption. These networks do not just need more boxes; they need compact and right-sized corrugated packs that can withstand repeated lateral handling from picking to dispatch. That requirement is pushing buyers toward testliner and fluting grades that meet short-span compression and edge-crush needs with greater consistency, rather than relying only on burst-factor thresholds. Mills that still compete mainly on low-cost recycled output are under pressure to upgrade their specification control, because automated, fast-turn delivery systems are exposing weak formations and uneven compression performance more quickly than traditional retail channels did. This change is important for the India containerboard market because it is shifting demand toward technically dependable grades even within high-volume, price-sensitive packaging formats.

Food And Beverage Packaging Premiumization

India's food processing and beverage value chains are steadily tightening packaging specifications as organized retail, food safety requirements, and commitments to recyclable formats all move in the same direction. Brand owners such as Coca-Cola, PepsiCo, and Parle Agro have been aligning their packaging portfolios toward recyclable formats, thereby increasing the use of mono-material and fiber-based secondary packaging in organized distribution channels. Food processors are also reducing pack weights by moving liner grammages from 150 GSM toward 120 GSM while still trying to preserve compression performance through stronger fiber design and better board engineering. In April 2026, the Food Safety and Standards Authority of India issued a draft notification proposing paper, paperboard, cellulose, or other naturally derived materials for pan masala and tobacco packaging, extending the regulatory push for fiber-based formats into a category that had long relied on multi-layer plastic structures. That change matters because southern and western India already has high demand density for these product categories, so that any format migration can flow quickly into regional requirements for testliner and kraft grades. For the India containerboard market, this premiumization trend is raising the baseline expectation for print quality, compression consistency, and recyclability across food-linked corrugated packaging.

Wastepaper And Imported Fiber Price Volatility

India still relies on seaborne recovered fiber for a meaningful share of recycled-board furnish, and that dependence leaves many producers exposed to sudden cost swings in imported OCC and other feedstock streams. The risk is amplified by currency movement, because INR weakness can push landed costs higher even when dollar-denominated international fiber prices appear stable. This creates a widening gap between integrated players with captive pulp or plantation support and recycled-fiber mills that depend heavily on imported furnish and short procurement cycles. Smaller mills are especially vulnerable because they lack the financial flexibility to build inventory buffers when import conditions turn unfavorable, which can force abrupt production cuts or local price increases. The pressure also changes sourcing behavior, as mills seeking higher-purity recovered inputs compete more directly for premium grades rather than relying on mixed domestic scrap streams. For the India containerboard market, fiber volatility remains the most immediate profitability risk for producers that lack integration and scale.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Toward Recyclable Fiber-Based Packaging

- Manufacturing And Export Logistics Expansion

- Power, Fuel, And Freight Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 64.53% of the India containerboard market in 2025, reflecting the cost logic of a manufacturing base that still depends heavily on recovered fiber to remain competitive. India recycled 50% of used paper and boards, compared with 85% in developed economies, which shows that domestic recovery efficiency is still far below the level needed to fully support mill furnish needs. That gap affects both availability and quality, because weaker collection systems produce a more uneven domestic recovered-fiber stream and keep many mills dependent on imported OCC. Virgin fiber grades remained the smaller material segment, but they are projected to grow at a 6.02% CAGR through 2031, as brand premiumization and investment in import substitution support higher-performance kraftliner demand. The India containerboard market is therefore seeing a two-speed material transition, where recycled grades still dominate volume while virgin grades are becoming more attractive for applications that require higher compression strength, smoother surfaces, and greater consistency.

Virgin grades are also benefiting from trade action, as the Directorate General of Trade Remedies recommended anti-dumping duties of USD 152.27 per metric ton on Chinese virgin paperboard and USD 123.18 per metric ton on Chilean virgin paperboard, which could improve the economics for domestic mills if those measures hold. FSC certification and EPR compliance are becoming commercial entry requirements in the Indian containerboard industry, especially for FMCG and pharmaceutical exporters, who are now screening packaging suppliers more closely for traceability and sustainability credentials. Paswara Papers illustrates the balancing act within the segment, as it has shifted from a 60:40 kraft-to-kraftliner mix toward a more liner-led output profile while prioritizing high-quality DSOCC imports from the United States over mixed-grade recovered fiber. That move shows how even mid-tier producers are separating commodity recycled output from higher-specification grades, and it also suggests that demand for premium imported recovered fiber can remain firm even if there is only a slow improvement in lower-grade domestic collection.

List of Companies Covered in this Report:

- ITC Limited

- JK Paper Limited

- West Coast Paper Mills Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- B&B Triplewall Containers

- Pakka Limited

- N R Agarwal Industries Limited

- Khanna Paper Mills Limited

- Paswara Papers Limited

- Bell Multi Kraft Private Limited

- Laxmi Board and Paper Mills Private Limited

- Apollo Papers LLP

- Venkraft Paper Mills Private Limited

- Aryan Paper Mills Private Limited

- Ruchira Papers Limited

- Star Paper Mills Limited

- Shree Ajit Pulp and Paper Limited

- Caliber Papers LLP

- Gauranga Papers LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce and Quick-Commerce Corrugated Demand

- 4.2.2 Food and Beverage Packaging Premiumization

- 4.2.3 Regulatory Push Toward Recyclable Fiber-Based Packaging

- 4.2.4 Manufacturing and Export Logistics Expansion

- 4.2.5 Lightweighting and Strength Engineering for Automated Corrugation

- 4.2.6 Premium Kraftliner Import Substitution

- 4.3 Market Restraints

- 4.3.1 Wastepaper and Imported Fiber Price Volatility

- 4.3.2 Power, Fuel, and Freight Cost Inflation

- 4.3.3 Quality Variability in Domestic Recovered Fiber Streams

- 4.3.4 Post-2027 EU Waste Shipment Regulation Exposure

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ITC Limited

- 6.4.2 JK Paper Limited

- 6.4.3 West Coast Paper Mills Limited

- 6.4.4 Tamil Nadu Newsprint and Papers Limited

- 6.4.5 Emami Paper Mills Limited

- 6.4.6 B&B Triplewall Containers

- 6.4.7 Pakka Limited

- 6.4.8 N R Agarwal Industries Limited

- 6.4.9 Khanna Paper Mills Limited

- 6.4.10 Paswara Papers Limited

- 6.4.11 Bell Multi Kraft Private Limited

- 6.4.12 Laxmi Board and Paper Mills Private Limited

- 6.4.13 Apollo Papers LLP

- 6.4.14 Venkraft Paper Mills Private Limited

- 6.4.15 Aryan Paper Mills Private Limited

- 6.4.16 Ruchira Papers Limited

- 6.4.17 Star Paper Mills Limited

- 6.4.18 Shree Ajit Pulp and Paper Limited

- 6.4.19 Caliber Papers LLP

- 6.4.20 Gauranga Papers LLP

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment