PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064486

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064486

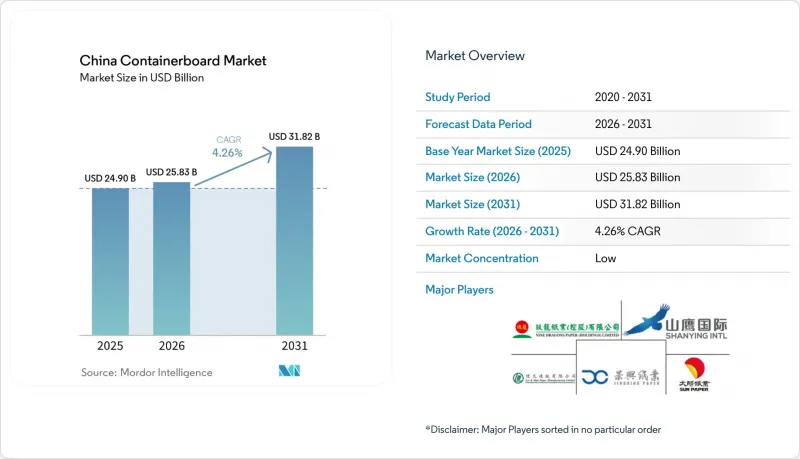

China Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china containerboard market size is projected to be USD 24.9 billion in 2025, USD 25.83 billion in 2026, and reach USD 31.82 billion by 2031, growing at a CAGR of 4.26% from 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Containerboard Market Trends and Insights

E-Commerce And Parcel Delivery Expansion

E-commerce remains the single strongest driver of demand for the China containerboard market because parcel movement is now embedded in daily consumption across urban and rural China. China's express network handled 175 billion parcels in 2024, making it the world's first for the 11th straight year. The amended Provisional Regulations on Express Delivery took effect on June 1, 2025, and pushed service quality and packaging durability into a firmer regulatory framework. That policy direction favors sturdier corrugated formats and supports a more reliable base of box demand for the China containerboard market. Corrugated demand from the express sector is on track to exceed 9 million tons in 2026, indicating that logistics demand is still rising even as mill pricing remains under pressure. The demand base is also spreading into lower-tier counties, widening the reach of the China containerboard market beyond traditional coastal manufacturing centers.

Food And Beverage Packaging Intensity

Food and beverage remains the largest demand center in the China containerboard market, accounting for 42.41% of end-user share in 2025 and still serving the broadest mix of packaging needs. The category is no longer driven only by shipment volume, because fresh produce, prepared meals, dairy, and beverage distribution all require more stable box performance than standard low-specification transport packaging. Cold-chain distribution is driving higher moisture resistance, stacking strength, and surface quality, raising the value profile of the board used in the Chinese containerboard market. China's GB 4806.8 food safety framework limits the use of recycled fiber in certain primary food-contact applications, redirecting part of premium food packaging demand toward virgin-fiber and coated grades. That shift is helping mills with certified material and compliance-ready product lines win stronger positions with major food brands in the China containerboard market. It also means that product mix improvement is being driven by compliance and performance needs, not just by higher shipment counts.

Persistent Overcapacity And Price Competition

Persistent overcapacity remains the main structural restraint on the China containerboard market because supply additions have continued to outpace real demand absorption. Capacity reached 38.19 million tons in 2025, while output stood at 28.2 million tons, which kept utilization in the 70-80% range across the sector. That mismatch left average industry net margins at 2.3% and kept many producers under pressure even when shipment volumes were stable. Around 140 small and medium production lines were shut or converted in 2025, but that still represented only a partial response to the scale of excess supply in the China containerboard market. Beijing's anti-innovation language points to a policy desire to curb destructive price competition, but pricing relief in the China containerboard market will still depend on slower new capacity additions over multiple investment cycles. Until that happens, the China containerboard market is likely to remain volume-supported but margin-constrained.

Other drivers and restraints analyzed in the detailed report include:

- Plastic-Substitution And Green Packaging Regulation

- Premiumization Toward Higher-Performance Containerboard

- Fiber And Energy Cost Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 69.14% of the China containerboard market share in 2025, which kept this material base clearly in the lead. That position came from China's deep OCC collection system and the long-established production infrastructure built around recycled fiber processing. Large mills in the Yangtze River Delta and Pearl River Delta still benefit from scale, converter proximity, and lower transport complexity for recovered paper flows, which supports the cost logic of this part of the China containerboard market. The recycled segment also fits the needs of high-volume testliner and fluting output, where consistent throughput matters more than premium pricing. This explains why recycled fiber remains the backbone of the China containerboard industry, even as margins in commodity grades stay under pressure.

Virgin fibers are projected to grow at a 4.68% CAGR through 2031, making them the fastest-growing material category in the China containerboard market. Food-contact rules, export-grade packaging requirements, and stronger specifications in cold-chain distribution are all lifting the role of virgin-based grades across the China containerboard market. China's GB 4806.8 framework supports that shift because it limits the use of recycled fiber in certain primary food-contact applications. Nine Dragons Paper is also targeting an additional 2.5 million tons of chemical pulp capacity across Chongqing, Tianjin, Beihai, and Dongguan, which shows how major players are building upstream support for this higher-value material mix. The result is a more divided China containerboard industry, where one tier focuses on scale-driven recycled grades and another moves toward virgin-fiber kraftliners and coated products with better pricing power.

List of Companies Covered in this Report:

- Nine Dragons Paper (Holdings) Limited

- Lee & Man Paper Manufacturing Limited

- Shanying International Holdings Co., Ltd.

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- Dongguan Jianhui Paper Co., Ltd.

- Shandong Chenming Paper Holdings Limited

- Shandong Bohui Paper Industry Co., Ltd.

- Longchen Paper & Packaging Co., Ltd.

- Liansheng Paper Industry (Longhai) Co., Ltd.

- Yuen Foong Yu Paper Manufacturing Co., Ltd.

- Jiangsu Rongsheng Pulp & Paper Co., Ltd.

- Guangzhou Paper Group Co., Ltd.

- Shandong Huatai Paper Industry Co., Ltd.

- Anhui Shanying Paper Industry Co., Ltd.

- Guangxi Jingui Pulp & Paper Co., Ltd.

- Zhejiang Yongtai Paper Co., Ltd.

- Zhejiang Zhengda Paper Co., Ltd.

- Hengfeng Paper Co., Ltd.

- Jiangsu Longchen Greentech Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 E-commerce and Parcel Delivery Expansion

- 4.3.2 Food and Beverage Packaging Intensity

- 4.3.3 Plastic-Substitution and Green Packaging Regulation

- 4.3.4 Premiumization Toward Higher-Performance Containerboard

- 4.3.5 Direct-From-Origin Shipping Needs Stronger Board

- 4.3.6 Inland Parcel Growth Rebalances Mill Footprints

- 4.4 Market Restraints

- 4.4.1 Fiber and Energy Cost Volatility

- 4.4.2 Persistent Overcapacity and Price Competition

- 4.4.3 Dry-Pulp Import Scrutiny Disrupts Low-Cost Fiber

- 4.4.4 Packaging Reduction Lowers Fiber Intensity per Parcel

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nine Dragons Paper (Holdings) Limited

- 6.4.2 Lee & Man Paper Manufacturing Limited

- 6.4.3 Shanying International Holdings Co., Ltd.

- 6.4.4 Shandong Sun Paper Industry Joint Stock Co., Ltd.

- 6.4.5 Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- 6.4.6 Dongguan Jianhui Paper Co., Ltd.

- 6.4.7 Shandong Chenming Paper Holdings Limited

- 6.4.8 Shandong Bohui Paper Industry Co., Ltd.

- 6.4.9 Longchen Paper & Packaging Co., Ltd.

- 6.4.10 Liansheng Paper Industry (Longhai) Co., Ltd.

- 6.4.11 Yuen Foong Yu Paper Manufacturing Co., Ltd.

- 6.4.12 Jiangsu Rongsheng Pulp & Paper Co., Ltd.

- 6.4.13 Guangzhou Paper Group Co., Ltd.

- 6.4.14 Shandong Huatai Paper Industry Co., Ltd.

- 6.4.15 Anhui Shanying Paper Industry Co., Ltd.

- 6.4.16 Guangxi Jingui Pulp & Paper Co., Ltd.

- 6.4.17 Zhejiang Yongtai Paper Co., Ltd.

- 6.4.18 Zhejiang Zhengda Paper Co., Ltd.

- 6.4.19 Hengfeng Paper Co., Ltd.

- 6.4.20 Jiangsu Longchen Greentech Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment