PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065459

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065459

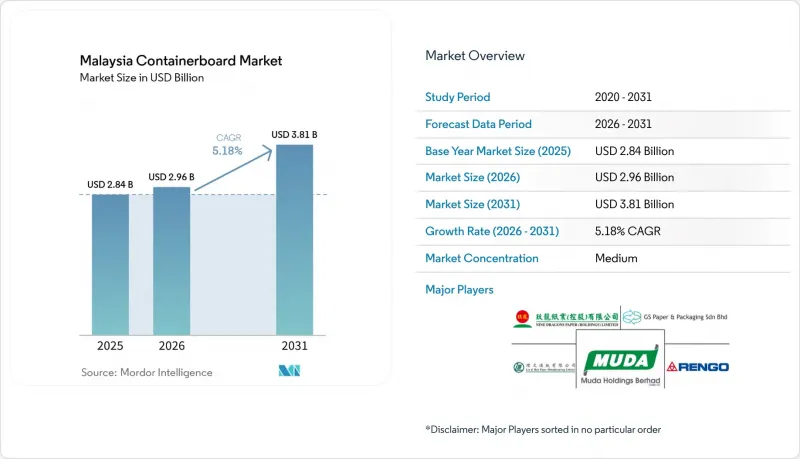

Malaysia Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the malaysia containerboard market size is projected to expand from USD 2.84 billion in 2025 and USD 2.96 billion in 2026 to USD 3.81 billion by 2031, registering a CAGR of 5.18% between 2026 to 2031.

This report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Containerboard Market Trends and Insights

Rising E-Commerce Parcel Volumes

Parcel demand continues to lift the Malaysian containerboard market, as online retail creates a steady flow of secondary and transit packaging across urban and suburban delivery networks. Ninja Van Malaysia projected 5% to 10% growth in domestic parcel volumes in 2026 versus 2025, after already reaching more than 20 million parcel recipients nationwide. Malaysia's courier market was valued at MYR 6.8-6.9 billion (USD 1.6-1.7 billion) in 2025, underscoring the growing role of delivery services in the local packaging flow. This is changing box specifications as well, because many marketplace sellers now want single-wall corrugated boxes with cleaner print surfaces that improve shelf appeal and the delivery experience. E-commerce demand also supports shorter production runs and more frequent design changes, giving mills and converters an edge by pairing consistent board quality with fast turnaround.

Food And Beverage Packaging Premiumization

Food and beverage remains a core volume base for the Malaysia containerboard market, but the mix is moving toward higher-value box formats rather than simple brown transit packaging. Malaysia was described as a stable market that targets 2% to 3% annual value growth within the broader regional food and beverage opportunity. Retail-ready corrugated formats with pre-printed surfaces and controlled-tear features command clear pricing premiums over standard regular slotted containers, which means board consumption per unit can rise even when shipment volume grows at a slower pace. The demand pattern is also supported by chilled products, premium snacks, and branded grocery distribution, all of which require better presentation and more consistent performance in humid conditions. Cold-chain activity adds another layer, because moisture resistance and surface quality matter more when food packaging must move through longer logistics chains.

Old Corrugated Container Price And Supply Volatility

Old corrugated container volatility remains the clearest short-term pressure point for the Malaysian containerboard market, as recycled-grade mills are exposed to swings in imported fiber costs. Industry coverage in 2025 described volatility in OCC and mixed paper markets as a persistent condition rather than a temporary disruption, with supply and demand often falling out of step for several months. This creates planning difficulties for mills that buy heavily in the spot market and then struggle to quickly pass higher costs through to box customers. The issue becomes more serious when energy costs also rise, because recycled-board economics then come under pressure from both fiber and utilities simultaneously. In practice, mills with stronger domestic collection ties or longer procurement contracts have a more durable margin position than mills that depend mainly on imported OCC cargoes.

Other drivers and restraints analyzed in the detailed report include:

- Electronics And E&E Export Strength

- Shift Away From Single-Use Plastics

- Competition From Low-Cost Plastic Packaging Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 66.18% of the Malaysian containerboard market share in 2025, confirming that the local system still relies on long-established OCC collection, recycled-medium production, and testliner capacity. The Malaysian containerboard industry has spent years building mill economics around recycled inputs, keeping recycled grades central to volume demand even as product requirements become more complex. Malaysia's recovered paper trade also reflected improving quality premiums for sorted domestic grades relative to mixed household collections in recent periods. This part of the Malaysia containerboard market benefits from cost efficiency, shared fiber lines, and established downstream acceptance across standard box applications. It also fits the country's role as a converting and consuming base, where broad domestic box demand supports a steady pull for recycled liners and mediums.

Virgin fibers are the fastest-growing material segment, with a forecast CAGR of 5.63% from 2026 to 2031, driven by increased demand from electronics exports, cold-chain food packaging, and retail-ready formats that require stronger, cleaner board surfaces. GS Paperboard and Packaging's PM3 in Selangor, built with a MYR 1.2 billion (USD 0.29 billion) investment, produces lightweight testliner grades from 100% recycled material at up to 450,000 tonnes annually, demonstrating that domestic producers are still raising the performance ceiling of recycled board. At the same time, Nextgreen IOI Pulp and Xiamen C&D Paper and Pulp Group announced Malaysia's first 150,000-tonne integrated pulp facility in Pahang in April 2025, with Phase 1 capital expenditure of MYR 900 million (USD 202 million) using palm biomass feedstock. If that project scales well, it could ease import dependence in the Malaysia containerboard market and improve the local cost base for kraftliner production over time.

List of Companies Covered in this Report:

- GS Paperboard & Packaging Sdn Bhd

- Muda Paper Mills Sdn. Bhd.

- ND Paper (Malaysia) Sdn. Bhd.

- Lee & Man Paper Manufacturing Ltd.

- Rengo Packaging Malaysia Sdn Bhd

- Can-One Berhad

- KYM Industries (M) Sdn Bhd

- Ornapaper Industry (M) Sdn. Bhd.

- Box-Pak (Malaysia) Bhd

- Golden Corrugated Box (M) Sdn Bhd

- Avapac Sdn Bhd

- PD Pac Sdn. Bhd.

- Fibre Pak (Malaysia) Sdn. Bhd.

- YCN Carton Sdn Bhd

- Bintang Packaging Industries (M) Sdn Bhd

- Pine Packaging (M) Sdn. Bhd.

- Honwee Packaging Sdn. Bhd.

- Century Bond Bhd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce Parcel Volumes

- 4.2.2 Food and Beverage Packaging Premiumization

- 4.2.3 Electronics and E&E Export Strength

- 4.2.4 Shift Away From Single-Use Plastics

- 4.2.5 China-Plus-One Manufacturing Spillover Into Malaysia

- 4.2.6 Lightweight Recycled Board Upgrades at Domestic Mills

- 4.3 Market Restraints

- 4.3.1 Old Corrugated Container Price and Supply Volatility

- 4.3.2 Competition From Low-Cost Plastic Packaging Formats

- 4.3.3 Chinese Capacity Influx and Regional Oversupply Pressure

- 4.3.4 Mill Automation and Technical Talent Gaps

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GS Paperboard & Packaging Sdn Bhd

- 6.4.2 Muda Paper Mills Sdn. Bhd.

- 6.4.3 ND Paper (Malaysia) Sdn. Bhd.

- 6.4.4 Lee & Man Paper Manufacturing Ltd.

- 6.4.5 Rengo Packaging Malaysia Sdn Bhd

- 6.4.6 Can-One Berhad

- 6.4.7 KYM Industries (M) Sdn Bhd

- 6.4.8 Ornapaper Industry (M) Sdn. Bhd.

- 6.4.9 Box-Pak (Malaysia) Bhd

- 6.4.10 Golden Corrugated Box (M) Sdn Bhd

- 6.4.11 Avapac Sdn Bhd

- 6.4.12 PD Pac Sdn. Bhd.

- 6.4.13 Fibre Pak (Malaysia) Sdn. Bhd.

- 6.4.14 YCN Carton Sdn Bhd

- 6.4.15 Bintang Packaging Industries (M) Sdn Bhd

- 6.4.16 Pine Packaging (M) Sdn. Bhd.

- 6.4.17 Honwee Packaging Sdn. Bhd.

- 6.4.18 Century Bond Bhd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment