PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063883

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063883

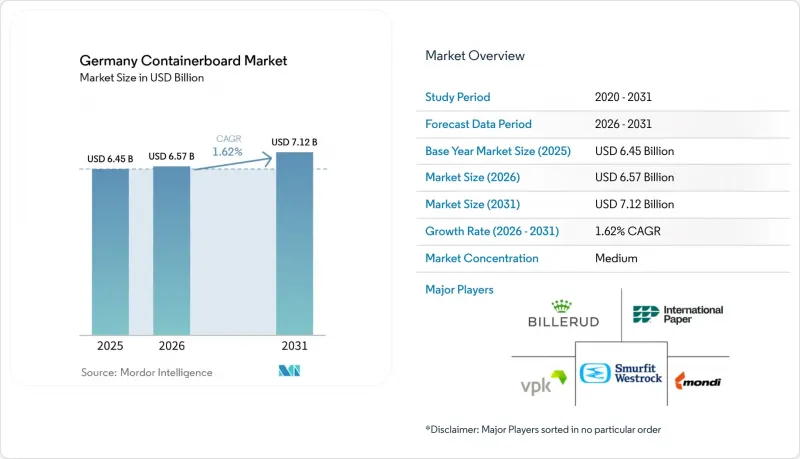

Germany Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany containerboard market size is expected to increase from USD 6.45 billion in 2025 to USD 6.57 billion in 2026 and reach USD 7.12 billion by 2031, growing at a CAGR of 1.62% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Containerboard Market Trends and Insights

Rising E-Commerce and Omnichannel Fulfillment Demand

Germany's online retail sector rose to EUR 92.4 billion (USD 100 billion) in 2025, up 4% from 2024, with marketplace platforms driving growth while non-marketplace channels declined on average by 5.4%. This pattern is concentrating corrugated demand around a smaller set of large logistics operators, which raises the value of short lead times and tightly configured lightweight formats in the German containerboard market. Corrugated board held a 90% share of German e-commerce packaging in 2024 because it remained strong in protection, recyclability, and automation compatibility. Germany's e-commerce penetration reached 87% in 2024, average parcel deliveries were 54 per resident, and the courier, express, and parcel segment is projected to expand at a 3.4% CAGR through 2031. The German containerboard market is therefore seeing a stronger pull for right-size recycled medium and testliner formats than for heavier parcel grades used in earlier shipping models.

Plastic-to-Paper Substitution in Secondary and Transit Packaging

The move from plastic transport formats to paper-based alternatives is advancing in Germany as commercial buyers and regulators both push for easier recycling and lower compliance costs. Across Europe, paper and cardboard reached a 87% recycling rate in 2023, while plastics stood at 42.1%, strengthening the economic case for fiber-based packaging under EPR systems. The Heidelberger Druckmaschinen AG and DHBW Heilbronn study on packaging to 2030 projected that flexible paper packaging will grow by more than 4.5% annually through the decade. Hugo Beck and Mondi showcased a commercial example at Interpack 2026 featuring the Paper S sleeve wrapper, which uses 70 gsm kraft paper instead of plastic shrink film for secondary packaging. In the German containerboard market, this shift supports greater demand for medium-weight kraft and specialty fluting grades than for heavyweight linerboard in transit applications.

Volatile Energy, Gas, and OCC Costs

Energy cost volatility is still the clearest structural restraint on the Germany containerboard market because German recycled grades remain highly exposed to natural gas costs. Fastmarkets reported that testliner production draws 68% of its energy from natural gas, while white-lined chipboard can reach 92%. German natural gas prices rose 18% in Q2 2025 versus Q2 2024, and producers were still pursuing further hikes in early 2026 as energy pressure persisted. The German containerboard market feels this most sharply at non-integrated converters and recycled-grade mills, as they have less room to hedge costs or absorb concurrent spikes in energy and fiber input prices.

Other drivers and restraints analyzed in the detailed report include:

- Food and Beverage Shipment Hygiene and Shelf-Ready Needs

- High Recycled-Fiber Acceptance in German Packaging Procurement

- Weak Industrial Production and Cautious Ordering

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fibers held 62.5% of the Germany containerboard market share in 2025, while recycled grades are projected to grow at a 2.1% CAGR through 2031. Recycled-furnish growth is strongest in consumer goods, retail logistics, and FMCG applications where procurement teams are comfortable with high-quality recovered fiber. Germany's closed-loop collection structure supports this shift because corrugated board makes up 88% by mass of commercial transport packaging collected as paper, paperboard, and cardboard. The move is especially visible in parcel and shelf-ready formats where automated corrugators favor improved dimensional consistency from better stock preparation and cleaner OCC streams.

Virgin-fiber board still keeps a structural role in pharmaceutical secondary packaging, fresh produce, and heavy-wall industrial corrugated because those uses still value burst strength, print surface, and moisture resistance. The 2024 German practitioner survey showed that 80% of respondents see virgin fiber in incoming packaging as a positive input to recycled pulp quality. That is why the German containerboard market is moving toward a more balanced raw-material mix rather than a full shift to mono-recycled fiber.

List of Companies Covered in this Report:

- Progroup AG

- Papierfabrik Palm GmbH & Co. KG

- Hamburger Rieger GmbH

- LEIPA Georg Leinfelder GmbH

- Klingele Paper & Packaging SE & Co. KG

- Papierfabrik Adolf Jass GmbH & Co. KG

- THIMM Group GmbH + Co. KG

- Dunapack Spremberg GmbH & Co. KG

- Mondi plc

- Smurfit Westrock plc

- Saica, S.A.

- VPK Group NV

- Model GmbH

- Rondo Ganahl AG

- Billerud AB

- Metsa Board Corporation

- Schumacher Packaging GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce and Omnichannel Fulfillment Demand

- 4.2.2 Plastic-to-Paper Substitution in Secondary and Transit Packaging

- 4.2.3 Food and Beverage Shipment Hygiene and Shelf-Ready Needs

- 4.2.4 High Recycled-Fiber Acceptance in German Packaging Procurement

- 4.2.5 Lightweight Sub-100 gsm Grade Adoption on Automated Corrugators

- 4.2.6 Alternative-Fiber Blending for White-Top and Specialty Liner Innovation

- 4.3 Market Restraints

- 4.3.1 Volatile Energy, Gas, and OCC Costs

- 4.3.2 Weak Industrial Production and Cautious Ordering

- 4.3.3 Recovered-Fiber Export Disruptions Distorting Domestic Supply Economics

- 4.3.4 PPWR Compliance and Documentation Costs Ahead of Full Monetization

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Progroup AG

- 6.4.2 Papierfabrik Palm GmbH & Co. KG

- 6.4.3 Hamburger Rieger GmbH

- 6.4.4 LEIPA Georg Leinfelder GmbH

- 6.4.5 Klingele Paper & Packaging SE & Co. KG

- 6.4.6 Papierfabrik Adolf Jass GmbH & Co. KG

- 6.4.7 THIMM Group GmbH + Co. KG

- 6.4.8 Dunapack Spremberg GmbH & Co. KG

- 6.4.9 Mondi plc

- 6.4.10 Smurfit Westrock plc

- 6.4.11 Saica, S.A.

- 6.4.12 VPK Group NV

- 6.4.13 Model GmbH

- 6.4.14 Rondo Ganahl AG

- 6.4.15 Billerud AB

- 6.4.16 Metsa Board Corporation

- 6.4.17 Schumacher Packaging GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment