PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063884

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063884

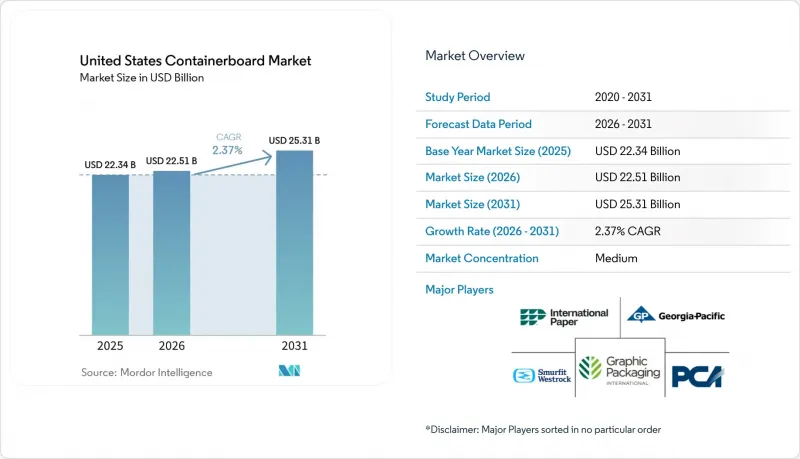

United States Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states containerboard market size was valued at USD 22.34 billion in 2025 and estimated to grow from USD 22.51 billion in 2026 to reach USD 25.31 billion by 2031, at a CAGR of 2.37% during the forecast period 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Containerboard Market Trends and Insights

Rising E-Commerce and Omnichannel Box Demand

Online retail continues to support a broad demand floor for the United States containerboard market, even though parcel growth no longer converts into box demand on a one-to-one basis. Corrugated boxes still account for more than 90% of goods shipped in the country, keeping fiber-based transport packaging central to domestic commerce. The mix inside fulfillment networks is changing, with more die-cut formats, single-wall structures, and microflute designs replacing simpler runs. That shift favors producers who can supply stronger and lighter grades rather than just the commodity-grade medium. Rabobank noted in early 2026 that demand should remain broadly flat through late 2027, with e-commerce gains partly offset by parcel-level lightweighting. In the United States containerboard market, that means omnichannel demand is supporting plant utilization, while product mix is doing more of the work on margins.

Growing Recycled-Content and Pauperization Mandates

Brand owners are directing more packaging specifications toward paper-based formats, which is reinforcing demand for the United States containerboard market. Amazon removed 95% of plastic air pillows from North American fulfillment centers and replaced them with paper filler made from 100% recycled content, avoiding 15 billion plastic air pillows each year. That move shows how packaging redesign at one large shipper can alter fiber demand across broad supply chains. It also supports recycled-fiber grades, as post-consumer content is increasingly part of procurement requirements rather than a branding option. The United States containerboard market benefits from this shift because corrugated packaging already fits existing recovery systems and can more easily meet recyclability expectations than many competing materials. A related effect is that more paper-based packaging eventually returns to the OCC stream, which helps replenish recycled feedstock even as demand for recovered fiber rises.

Flexible Mailers and Ships-In-Own-Container Substitution

Flexible mailers and ship-in-own-container programs are reducing part of the box demand that would otherwise support the United States containerboard market. Amazon reported that corrugated boxes fell from 43% to 40% of deliveries while ship-in-own-container participation increased from 8% to 11%. The effect is most visible in small-parcel e-commerce, where padded mailers and product-ready packs can bypass the need for an additional corrugated box. This does not remove parcel demand from the system, but it does reduce the square footage per shipment. At the same time, the remaining corrugated shipments often require stronger, more specialized board, which partly offsets the lost volumes from the mix. Even so, the United States containerboard market faces a real ceiling on growth if major platforms continue shifting more qualified items into non-box or no-overbox formats.

Other drivers and restraints analyzed in the detailed report include:

- Stable Food and Beverage Shipment Demand

- Capacity Rationalization Tightening Industry Utilization

- OCC and Energy Cost Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 54.5% of the United States containerboard market share in 2025 and are also projected to post the fastest CAGR of 3.4% through 2031. This position reflects the long build-out of OCC recovery, sorting, and mill systems across the country. The United States containerboard market has relied on that infrastructure for years, and recent brand-owner requirements for post-consumer content have further reinforced it. Capacity closures at older virgin-fiber assets also tightened the supply base for unbleached kraft grades and increased the relative weight of recycled production in the system. Producers such as Cascades, Kruger, Pratt Industries, and ND Paper have been investing in stronger recycled liner and medium offerings rather than staying confined to commodity grades. Cascades said its extra-high-performance linerboard uses 100% recycled fiber, including 90% post-consumer content, and is designed for lightweight, high-speed corrugating. That product direction shows how the United States containerboard industry is pushing recycled material deeper into performance-sensitive uses.

Virgin fibers still matter in applications where surface quality, burst strength, and food-contact assurance remain harder to meet with recycled furnish alone. Premium kraftliner, export packaging, and some retail-ready formats continue to support a functional premium for virgin grades. The United States containerboard market still relies on virgin output for parts of the packaging mix where reliability and branding requirements are strict. Mordor Intelligence noted that 89% of North American corrugated output carried chain-of-custody certifications in 2024, up from 76% in 2023, which points to continued investment in certified virgin inputs as well as broader sustainability documentation. Georgia-Pacific also announced an USD 83 million expansion at its Palatka, Florida mill in 2025, which underlined ongoing capital support for kraft-based paper output. The result is a market where recycled fiber leads on scale and growth, while virgin fiber remains important in the premium end of the grade spectrum.

List of Companies Covered in this Report:

- International Paper Company

- Smurfit Westrock plc

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries, Inc.

- Cascades Inc.

- Graphic Packaging International LLC

- Hood Container Corporation

- Green Bay Packaging Inc.

- Atlantic Packaging, LLC

- Menasha Corporation

- Nine Dragons Paper Holdings

- New-Indy Containerboard LLC

- Kruger Inc.

- Saica Pack USA, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-commerce and Omnichannel Box Demand

- 4.2.2 Growing Recycled-Content and Paperization Mandates

- 4.2.3 Stable Food and Beverage Shipment Demand

- 4.2.4 Capacity Rationalization Tightening Industry Utilization

- 4.2.5 Eco-Modulated EPR Fees Favoring Recyclable Corrugated Formats

- 4.2.6 Lightweight Recycled Liner Innovation Expanding Substitution

- 4.3 Market Restraints

- 4.3.1 Flexible Mailers and Ships-in-Own-Container Substitution

- 4.3.2 OCC and Energy Cost Volatility

- 4.3.3 PFAS-Free Barrier Qualification Costs in Food Applications

- 4.3.4 State-by-State EPR and Compliance Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Packaging Corporation of America

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Pratt Industries, Inc.

- 6.4.6 Cascades Inc.

- 6.4.7 Graphic Packaging International LLC

- 6.4.8 Hood Container Corporation

- 6.4.9 Green Bay Packaging Inc.

- 6.4.10 Atlantic Packaging, LLC

- 6.4.11 Menasha Corporation

- 6.4.12 Nine Dragons Paper Holdings

- 6.4.13 New-Indy Containerboard LLC

- 6.4.14 Kruger Inc.

- 6.4.15 Saica Pack USA, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment