PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063903

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063903

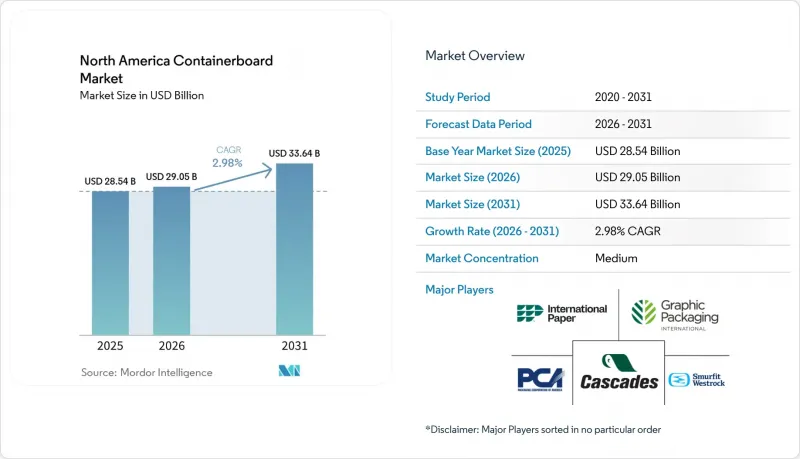

North America Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america containerboard market size is projected to expand from USD 28.54 billion in 2025 and USD 29.05 billion in 2026 to USD 33.64 billion by 2031, registering a CAGR of 2.98% between 2026 and 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Containerboard Market Trends and Insights

Growth In E-Commerce Packaging Demand

E-commerce remains the most durable volume driver for the North America containerboard market because direct shipment models require corrugated protection across fulfillment, sorting, and last-mile delivery. Packaging Corporation of America reported that corrugated shipments per shipping day were up 4.5% year over year in January 2026 and up 3% through mid-February, indicating that box demand was recovering faster than many broad retail indicators. This demand carries a built-in packaging intensity advantage because goods shipped to homes usually need more fiber per order than goods moved through store shelves. Smurfit Westrock said its addition of more than 600 new corrugated customers in Q1 2026 was driven by e-commerce and value-added formats, indicating that the North America containerboard market is benefiting from mix improvement as much as from simple shipment growth. The effect is stronger in grocery and fresh food delivery, where producers need thicker, more moisture-resistant board formats to protect temperature-sensitive, heavier products during transport.

Increasing Demand for Sustainable Packaging Solutions

Sustainability has become a basic buying requirement in the North America containerboard market rather than a premium feature that only a small set of customers seeks out. The Corrugated Packaging Alliance and Fiber Box Association reported in 2025 that corrugated containers outperformed reusable plastic containers across several environmental indicators under baseline US conditions, providing brand owners with a clearer basis for switching secondary packaging formats. The same assessment period showed that the average recycled fiber content in US containerboard reached 31.8%, indicating that recycled content is now built into regular-grade specifications rather than sitting in a narrow specialty tier. This matters commercially because mills that can blend recycled content into standard linerboard and medium grades can meet procurement targets across a wider customer base without expanding product complexity. As compliance rules tighten across states and provinces, the North America containerboard market is likely to reward producers that combine recycled furnish access, converting reach, and stable performance across mainstream packaging applications.

Volatility In Recovered Paper Prices

Recovered paper pricing remains the most visible input risk for recycled fiber producers in the North America containerboard market because old corrugated containers are the core furnish for many board grades. The market is exposed to abrupt price movement when supply from box recovery does not keep up with mill demand, since furnish availability depends on collection behavior and the pace at which used boxes return to the recycling stream. The Recycling Partnership estimated US residential curbside recovery rates for all recyclable materials at 20% in 2024, indicating a significant structural recovery gap that could tighten feedstock availability when demand improves. This gap matters because capacity management alone cannot solve furnish stress if recovered volumes remain inconsistent across cities and states. As a result, the North America containerboard market is likely to continue to see margin pressure and uneven pricing discipline until collection systems and recovery quality improve materially.

Other drivers and restraints analyzed in the detailed report include:

- Surge In Food and Beverage Takeaway and Delivery Services

- Replacement of Plastic Packaging Due to Regulatory Bans

- Energy Cost Fluctuations Impacting Production Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fibers held 32.15% of the North America containerboard market share in 2025 and are projected to grow at a 3.62% CAGR through 2031, keeping this grade in both the leading and fastest-growing positions within the material split. This lead reflects the stronger performance of kraft pulp-based linerboard, with higher burst strength, better print quality, and applications where consistency matters more than simple cost reduction. The North America containerboard industry still relies on virgin fiber, where export packaging, food contact needs, and heavier-duty transport formats leave limited room for substitution. That demand profile gives virgin grades a firmer pricing position, even as customers continue to expand recycled-content targets across broader packaging portfolios.

At the same time, the material picture is becoming more balanced as leading producers expand their recycled-grade capabilities alongside their virgin fiber assets. International Paper's April 2026 agreement to acquire NORPAC's Longview mill, which produces 1 million tons of containerboard annually and focuses on lightweight, high-performance recycled grades, shows that even large virgin fiber players are repositioning to meet recycled demand on the West Coast. The 31.8% average recycled fiber content already documented in US containerboard indicates that recycled furnish is now central to mainstream product design, not an edge case. Over time, that means the gap between virgin and recycled grades in the North America containerboard market may narrow at lower basis weights, while premium heavy duty applications continue to defend a clearer virgin fiber advantage.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- International Paper Company

- Packaging Corporation of America

- Georgia-Pacific LLC

- Cascades Inc.

- Domtar Corporation

- Kruger Inc.

- Pratt Industries Inc.

- Green Bay Packaging Inc.

- Sonoco Products Company

- Graphic Packaging Holding Company

- ND Paper LLC

- Mondi plc

- Kruger Packaging L.P.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in E-commerce Packaging Demand

- 4.2.2 Increasing Demand for Sustainable Packaging Solutions

- 4.2.3 Surge in Food and Beverage Takeaway and Delivery Services

- 4.2.4 Replacement of Plastic Packaging Due to Regulatory Bans

- 4.2.5 Advancements in High-Performance Lightweight Containerboard Grades

- 4.2.6 Strategic Capacity Expansions Near Regional Distribution Hubs

- 4.3 Market Restraints

- 4.3.1 Volatility in Recovered Paper Prices

- 4.3.2 Energy Cost Fluctuations Impacting Production Economics

- 4.3.3 Limited Railcar Availability Disrupting Intra-Regional Supply Chains

- 4.3.4 Growing Competition From Molded Fiber Packaging in Produce Sector

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 International Paper Company

- 6.4.3 Packaging Corporation of America

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Cascades Inc.

- 6.4.6 Domtar Corporation

- 6.4.7 Kruger Inc.

- 6.4.8 Pratt Industries Inc.

- 6.4.9 Green Bay Packaging Inc.

- 6.4.10 Sonoco Products Company

- 6.4.11 Graphic Packaging Holding Company

- 6.4.12 ND Paper LLC

- 6.4.13 Mondi plc

- 6.4.14 Kruger Packaging L.P.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment