PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063919

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063919

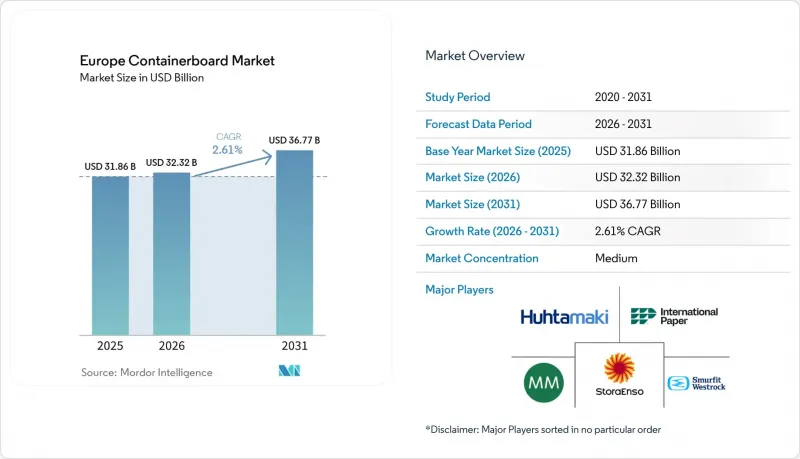

Europe Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the european containerboard market is projected to reach USD 31.86 billion in 2025, USD 32.32 billion in 2026, and USD 36.77 billion by 2031, growing at a CAGR of 2.61% from 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Germany, France, Italy, Spain, United Kingdom, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Containerboard Market Trends and Insights

Growth in E-Commerce and Online Retail

E-commerce continues to provide durable support for the Europe containerboard market, even though the pace now reflects a steadier logistics cycle rather than the earlier pandemic spike. The demand pattern is also changing because online retailers increasingly want right-sized boxes, stronger stacking performance, and better digital print-readiness rather than standard brown transit cases. That shift is important because it changes fiber mix and board specification, not only shipment volume. Germany already shows how this influence works in practice, with shipping packaging accounting for 6.7% of corrugated board revenue in 2024, even though its effect on quality standards extends well beyond that share. Early 2026 also opened with a better volume trend than many producers expected, which supports a more active restocking and packaging-conversion cycle in key markets. As a result, the Europe containerboard market is seeing demand shift toward lighter yet more capable board combinations that balance transport efficiency and brand presentation.

Stringent Sustainability Regulations Favoring Recyclable Packaging

Regulation is one of the clearest demand shapers for the Europe containerboard market, as the PPWR entered into force on February 11, 2025, and is scheduled to be broadly applied from August 12, 2026. The regulation requires all packaging placed on the EU market to be recyclable by 2030 and introduces a recyclability performance framework that will influence packaging choices across product categories. This creates a direct commercial advantage for fiber-based formats that already fit established collection and sorting systems better than many mixed-material packs. Italy provides a useful signal of readiness, as corrugated packaging recycling reached 92.5% in 2024, already above the EU's 2030 target of 85%. Germany also continued to report paper recovery rates above 90%, reinforcing the structural importance of recycled containerboard across the region. The Europe containerboard market therefore benefits not only from sustainability messaging, but also from a regulatory framework that increasingly rewards pack formats designed for high recovery and strong sorting outcomes.

Volatility in Wastepaper Collection Rates and Prices

Recovered-paper volatility remains the most immediate operating risk for the Europe containerboard market, especially for mills that rely fully on recycled fiber. In April 2025, OCC grades 1.04 and 1.05 rose by EUR 20-30 per ton (USD 22-33 per ton) across Europe as collection volumes weakened and export competition tightened supply. This pressure matters because recycled-fiber demand is being lifted by regulation at the same time that the feedstock base can tighten when consumer activity softens, or export demand improves. That mismatch creates a difficult margin structure for recycled containerboard producers, as higher raw-material costs do not always cleanly pass through to board pricing. It also explains why some mid-tier groups are seeking to secure asset collections and long-term feedstock channels rather than relying solely on open-market OCC purchases. The Europe containerboard market, therefore, faces a recurring tension in which circular-economy targets support demand, but the economics of collected fiber can still limit how profitably that demand is served.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Shelf-Ready Packaging in Retail Chains

- Increasing Substitution of Plastic with Paper-Based Packaging

- High Energy Costs in Europe's Paper Mills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 62.83% of the Europe containerboard market share in 2025, reflecting the region's mature OCC collection systems, the policy premium on circularity, and the cost advantage recycled grades can retain when input conditions are stable. This leadership position is reinforced by the fact that Germany's corrugated board sector sourced more than 81.8% of its paper input from recycled fiber in 2024. The recycled-fiber base also aligns well with the direction of EU packaging policy, as it supports established recovery infrastructure and brand-owner sustainability targets. At the same time, the regional picture is not uniform, as Italy still relies heavily on higher-quality virgin grades for food-contact and export-oriented applications. That unevenness is important because it shows that the Europe containerboard market is not moving toward recycled content at the same pace or with the same performance trade-offs in every country.

Virgin fibers remain the smaller material segment, but they are forecast to grow at a 3.62% CAGR through 2031, as converters and brand owners still need performance certainty in moisture-sensitive, export, and food-grade applications. The issue is not only strength, because purity, barrier compatibility, and process consistency also matter where recycled input quality can vary from batch to batch. This creates a practical ceiling for recycled substitution in parts of the Europe containerboard industry, even as regulation continues to favor circular content. It also explains why producers continue to invest in premium kraftliner and hybrid solutions, even when product failure is more costly than a higher fiber bill. The Europe containerboard market will therefore keep a large recycled base, but growth in virgin-backed and performance-led grades will continue where reliability matters more than the lowest possible raw-material cost.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- International Paper Company

- Mondi plc

- Stora Enso Oyj

- Holmen AB

- Svenska Cellulosa AB SCA

- Metsa Board Oyj

- Klingele Paper & Packaging Group

- Pro-Gest S.p.A.

- Hamburger Containerboard

- VPK Packaging Group NV

- LEIPA Group GmbH

- SAICA Group

- Reno de Medici S.p.A.

- Burgo Group S.p.A.

- Cartiera del Chiese S.p.A.

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in E-Commerce and Online Retail

- 4.2.2 Stringent Sustainability Regulations Favoring Recyclable Packaging

- 4.2.3 Rising Demand for Shelf-Ready Packaging in Retail Chains

- 4.2.4 Increasing Substitution of Plastic with Paper-Based Packaging

- 4.2.5 Expanding Cross-Border Fruit Export Corridors Requiring Humidity-Resistant Containerboard

- 4.2.6 Adoption of Digital Watermarking in Containerboard for Enhanced Sortation

- 4.3 Market Restraints

- 4.3.1 Volatility in Waste Paper Collection Rates and Prices

- 4.3.2 High Energy Costs in Europe's Paper Mills

- 4.3.3 Growing Competition from Lightweight Microflute Solid Board

- 4.3.4 Potential Supply Squeeze of Tall Oil Rosin Affecting Virgin Kraftliner Strength Additives

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 Italy

- 5.4.4 Spain

- 5.4.5 United Kingdom

- 5.4.6 Russia

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 International Paper Company

- 6.4.3 Mondi plc

- 6.4.4 Stora Enso Oyj

- 6.4.5 Holmen AB

- 6.4.6 Svenska Cellulosa AB SCA

- 6.4.7 Metsa Board Oyj

- 6.4.8 Klingele Paper & Packaging Group

- 6.4.9 Pro-Gest S.p.A.

- 6.4.10 Hamburger Containerboard

- 6.4.11 VPK Packaging Group NV

- 6.4.12 LEIPA Group GmbH

- 6.4.13 SAICA Group

- 6.4.14 Reno de Medici S.p.A.

- 6.4.15 Burgo Group S.p.A.

- 6.4.16 Cartiera del Chiese S.p.A.

- 6.4.17 Huhtamaki Oyj

- 6.4.18 Mayr-Melnhof Karton AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment