PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063920

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063920

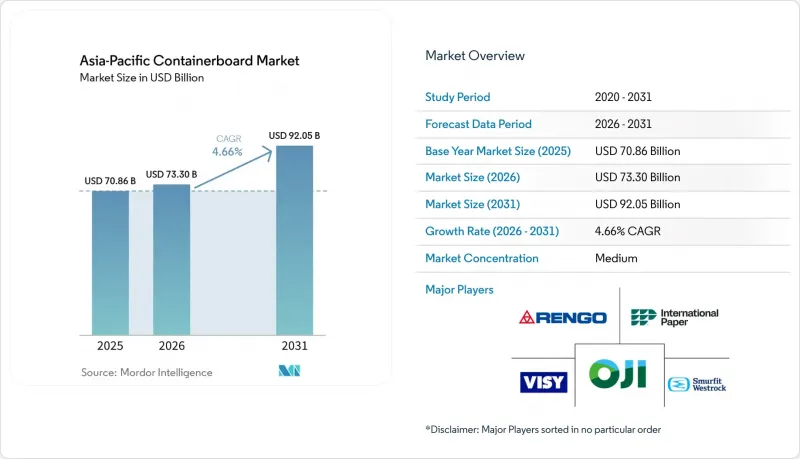

Asia-Pacific Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific containerboard market size is expected to grow from USD 70.86 billion in 2025 to USD 73.3 billion in 2026 and is forecast to reach USD 92.05 billion by 2031 at 4.66% CAGR over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (China, India, Japan, South Korea, Indonesia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Containerboard Market Trends and Insights

Growing E-Commerce Packaging Demand

Growing e-commerce activity remains the strongest immediate driver of the Asia-Pacific containerboard market, as corrugated formats already handle an estimated 80% of e-commerce parcels in major regional economies. The demand pattern is also changing in quality terms because algorithm-led packaging fitment systems can reduce corrugated board use per shipment by up to 30%, yet they increase the need for lighter and more consistent performance grades. This is pushing the Asia-Pacific containerboard market toward fluting and liner grades that can perform reliably in automated fulfillment, high-speed sortation, and dense parcel networks. It also favors converters that can turn short runs quickly near logistics clusters, where service speed now matters as much as board cost. Because parcel shipping remains a recurring logistics need rather than a one-time retail trend, the Asia-Pacific containerboard market keeps a firmer demand base than many other paper grades.

Government Bans on Single-Use Plastics

Plastic phase-out policies are steadily expanding the addressable demand base for the Asia-Pacific containerboard market into food service, fresh produce, pharmaceutical distribution, and seafood transport. In Australia, South Australia moved ahead with bans on additional single-use plastic items in September 2025, which strengthened the shift toward paper-based alternatives in food-related applications. Across the region, compliance rules are making traceability, recycled content, and food-safety certification more important in procurement decisions, which supports higher-value supply in the Asia-Pacific containerboard market. That changes competition because mills without certification infrastructure struggle to access regulated categories even if they remain cost-competitive in commodity grades. It also gives the Asia-Pacific containerboard market a source of demand that is less tied to trade swings or consumer spending cycles than traditional box demand.

Volatile Old Corrugated Container Prices

Old corrugated container price swings remain a direct margin risk for the Asia-Pacific containerboard market because recycled grades dominate regional supply and many mills still depend on purchased fiber. When recovered fiber costs move faster than finished board prices, smaller producers lose pricing flexibility, and working capital tightens quickly. Larger integrated groups are better protected because they can offset external price swings through collection systems, pulp integration, or a broader operating base. Nine Dragons Paper's FY2025 results showed that raw-material cost efficiency supported profits even as average selling prices declined, highlighting the advantage of scale during volatile input cycles. This keeps the Asia-Pacific containerboard market structurally uneven, with integrated leaders more able to defend margins than import-dependent commodity mills.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cold-Chain Logistics Infrastructure

- Rising Consumer Preference for Sustainable Packaging

- Supply Overhang from New Mega-Mills in China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers led with 67.83% of the Asia-Pacific containerboard market share in 2025, which reflects the region's dependence on secondary fiber for standard corrugated production. This position gives the Asia-Pacific containerboard market a cost advantage in large-volume box demand, especially in e-commerce and consumer staples, where price discipline remains important. Recycled grades also align with the region's growing circular packaging systems, as rising parcel volumes and retail distribution create a steady stream of recoverable board. At the same time, the Asia-Pacific containerboard industry still faces uneven fiber quality, exposure to imported pulp in several markets, and operating disruptions when recovered paper specifications are inconsistent.

Virgin fibers are forecast to grow at a 5.37% CAGR from 2026 to 2031, the fastest pace among material categories in the Asia-Pacific containerboard market. That growth reflects a quality upgrade rather than a broad replacement of recycled economics, with food-contact, pharmaceutical, and premium shipping formats demanding higher purity, printability, and consistency in strength. Nine Dragons Paper started production at new bleached folding boxboard lines at Jingzhou and Beihai in 2025, adding 1.2 million tonnes per annum of higher-value virgin-grade capacity as it diversified beyond its recycled corrugating base. The result is a two-track Asia-Pacific containerboard market where recycled fiber keeps volume leadership, while virgin grades capture the faster growth in premium and compliance-heavy uses.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- International Paper Company

- Nine Dragons Paper (Holdings) Limited

- Lee & Man Paper Manufacturing Ltd.

- Oji Holdings Corporation

- Rengo Co., Ltd.

- SCG Packaging Public Company Limited

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Anhui Shanying Paper Industry Co., Ltd.

- Asia Pulp & Paper (APP)

- Visy Industries Holdings Pty Ltd.

- Nippon Paper Industries Co., Ltd.

- Mondi plc

- Daio Paper Corporation

- ITC Limited

- JK Paper Ltd.

- Marubeni Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing E-commerce Packaging Demand

- 4.2.2 Expansion of Cold-Chain Logistics Infrastructure

- 4.2.3 Government Bans on Single-Use Plastics

- 4.2.4 Rising Consumer Preference for Sustainable Packaging

- 4.2.5 Integration of Smart Packaging Sensors in Corrugated Boxes

- 4.2.6 Capacity Expansion by Regional Mill Owners

- 4.3 Market Restraints

- 4.3.1 Volatile Old Corrugated Container (OCC) Prices

- 4.3.2 Supply Overhang From New Mega-Mills in China

- 4.3.3 Stringent Effluent Regulations Increasing Compliance Costs

- 4.3.4 Intensifying Competition From Flexible Packaging Formats

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 International Paper Company

- 6.4.3 Nine Dragons Paper (Holdings) Limited

- 6.4.4 Lee & Man Paper Manufacturing Ltd.

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 SCG Packaging Public Company Limited

- 6.4.8 Shandong Sun Paper Industry Joint Stock Co., Ltd.

- 6.4.9 Anhui Shanying Paper Industry Co., Ltd.

- 6.4.10 Asia Pulp & Paper (APP)

- 6.4.11 Visy Industries Holdings Pty Ltd.

- 6.4.12 Nippon Paper Industries Co., Ltd.

- 6.4.13 Mondi plc

- 6.4.14 Daio Paper Corporation

- 6.4.15 ITC Limited

- 6.4.16 JK Paper Ltd.

- 6.4.17 Marubeni Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment