PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063922

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063922

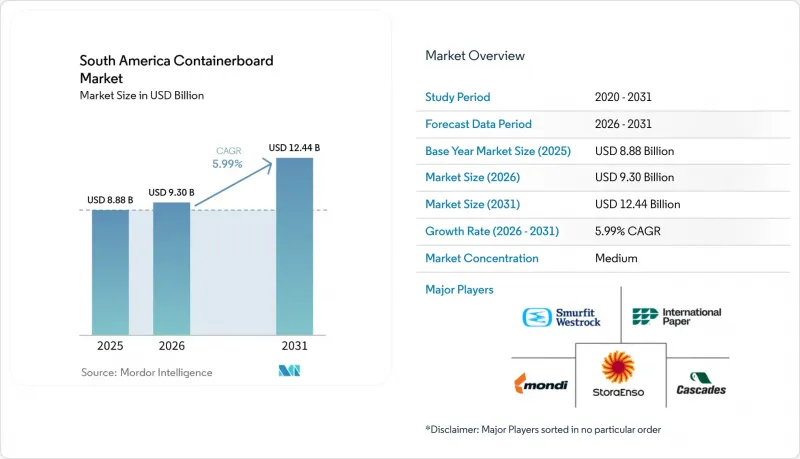

South America Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america containerboard market was valued at USD 8.88 billion in 2025 and is projected to reach USD 12.44 billion by 2031, expanding at a CAGR of 5.99% during 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Containerboard Market Trends and Insights

E-Commerce Boom Fueling Corrugated Packaging Demand

The South America containerboard market is seeing e-commerce compress the old gap between online retail growth and packaging conversion investment. Brazil opened 2026 with record corrugated board shipments of 343,000 tonnes in January, up 2.3% year over year, which showed that box demand remained firm at the start of the year. Animal protein and fast-moving consumer goods accounted for 30% of total corrugated demand in Brazil, keeping order flow active for producers tied to retail and fulfillment channels. Returns logistics is also changing design priorities, because shippers now want lighter boxes while still upgrading secondary packaging quality for repeat handling. Producers that invested in lightweight fluting and printable liner surfaces have been better placed to capture short-run, higher-margin work that standard kraft-focused mills struggle to match on turnaround time. Fastmarkets had already projected 5% full-year growth in corrugated box shipments in Brazil for 2024, so the South America containerboard market entered 2026 on top of a firm operating base rather than a weak rebound cycle.

Surging Agricultural Exports Requiring Robust Boxes

The South America containerboard market is benefiting from export agriculture, as these supply chains require stronger, moisture-resistant, and cold-chain-ready corrugated formats. Brazil's agribusiness exports reached a record USD 169.2 billion in 2025, and beef export value rose 39.9% while volume increased 20.4%, which reinforced demand for heavyweight corrugated boxes in long-distance protein trade. Those trade corridors to China, the European Union, and the Middle East stretch transport distance and handling intensity, which raises packaging requirements per shipment. Peru set a historic agricultural export record in 2025, shipping 540 products to 115 markets, including 767,230 tonnes of avocados and 343,537 tonnes of blueberries, keeping fresh-produce box demand on an upward trajectory. Chile also posted record fresh fruit and vegetable export revenue in 2025, and packaging is increasingly being used as a competitive tool in multimodal cold-chain movement to North American and European retailers. This is why the South America containerboard market is drawing support from agriculture in a steadier way than domestic fast-moving consumer goods demand, because export programs are tied to long-running trade flows and certification requirements.

Volatile Recovered Paper Prices Pressuring Margins

Recovered paper volatility remains one of the clearest cost risks in the South America containerboard market, especially for producers that rely on recycled fiber and cannot switch their mix toward virgin inputs. OCC imports resumed across the region in the third quarter of 2024 as converters secured supply for fruit export seasons, and price indices rose sharply as local currencies weakened against the USD. Domestic collection rates remain structurally low across much of the region, so local recovered fiber supply does not respond quickly when converter demand rises. Brazil's flexible plastic packaging sector was operating with only 5% recycled content, against a 2026 target of 22%, indicating broader weaknesses in collection and recovery systems and leaving less clean material available for the paper circuit. That leaves recycled-fiber producers exposed to a two-sided squeeze, because imported OCC becomes more expensive while domestic recovery quality also weakens. In the South America containerboard market, this cost pressure matters most for testliner and recycled-fluting suppliers, who are being asked by box makers to hold pricing steady while fiber inputs remain unstable.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Substitution of Plastic with Fiber-Based Packaging

- Capacity Expansions by Domestic Pulp and Paper Majors

- Limited Intermodal Logistics Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 64.35% of the South America containerboard market share in 2025, supported by integrated recovery networks and the cost efficiency of testliner and recycled-fiber fluting in domestic conversion. The South America containerboard market has long depended on recovered paper from industrial and commercial generators, especially in the Greater Sao Paulo and Curitiba belts, where integrated circuits have shaped procurement and production routines. MERCOSUR Resolution No. 02/25 updated technical requirements for cellulosic food-contact materials in 2025 and called for recycled-fiber articles to keep diisopropylnaphthalene, or DIPN, as low as technically feasible, which added a stronger food-safety dimension to sourcing decisions. That change is prompting some food-contact packaging buyers to scrutinize recycled content, particularly as export certifications and product-contact rules tighten.

Virgin fibers remain the smaller material category, but they are the fastest-growing segment with a 6.61% CAGR through 2031 in the South America containerboard market. Within the South America containerboard industry, this growth is tied to rising demand for premium kraft-grade liners for agricultural export packaging and boxes that must withstand moisture and stacking stress. Klabin's Ortigueira unit produces Eukaliner and has installed capacity above 900,000 tonnes per year across Paper Machines 27 and 28, giving it a strong position in higher-performance liner grades. Material choice in the South America containerboard industry is therefore moving away from a simple cost debate and toward a mix of compliance, strength, and surface quality requirements that favor premium virgin grades in selected end uses.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Klabin S.A.

- Mondi plc

- International Paper Company

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Stora Enso Oyj

- Sappi Limited

- Georgia-Pacific LLC

- Irani Papel e Embalagem S.A.

- Packaging Corporation of America

- Cascades Inc.

- Pratt Industries, Inc.

- Bio Pappel S.A.B. de C.V.

- Empresa CMPC S.A.

- Celulosa Arauco y Constitucion S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Boom Fueling Corrugated Packaging Demand

- 4.2.2 Surging Agricultural Exports Requiring Robust Boxes

- 4.2.3 Increasing Substitution of Plastic with Fiber-Based Packaging

- 4.2.4 Capacity Expansions by Domestic Pulp and Paper Majors

- 4.2.5 Rising Government Tariffs on Imported Old Corrugated Containers

- 4.2.6 Digital Print Adoption Enabling High-Margin Short Runs

- 4.3 Market Restraints

- 4.3.1 Volatile Recovered Paper Prices Pressuring Margins

- 4.3.2 Limited Intermodal Logistics Infrastructure

- 4.3.3 Slowdown in Consumer Spending Amid Currency Depreciation

- 4.3.4 Water-Use Restrictions Affecting Pulp Mills

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Klabin S.A.

- 6.4.3 Mondi plc

- 6.4.4 International Paper Company

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Stora Enso Oyj

- 6.4.8 Sappi Limited

- 6.4.9 Georgia-Pacific LLC

- 6.4.10 Irani Papel e Embalagem S.A.

- 6.4.11 Packaging Corporation of America

- 6.4.12 Cascades Inc.

- 6.4.13 Pratt Industries, Inc.

- 6.4.14 Bio Pappel S.A.B. de C.V.

- 6.4.15 Empresa CMPC S.A.

- 6.4.16 Celulosa Arauco y Constitucion S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment