PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064394

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064394

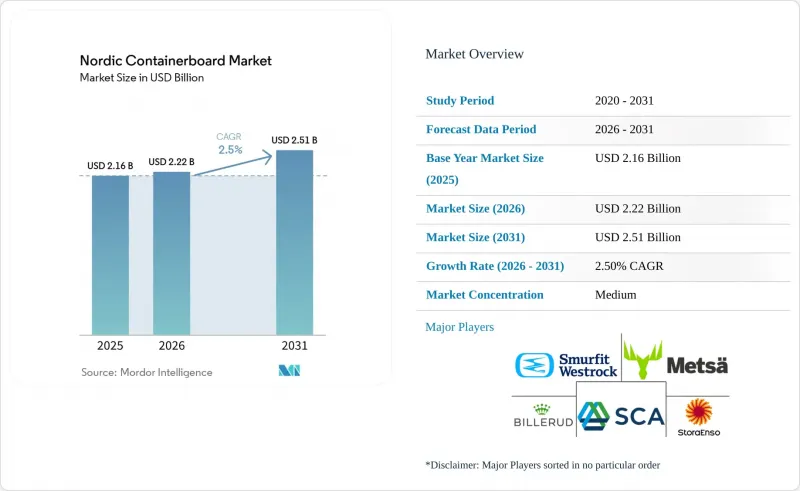

Nordic Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the nordic containerboard market size is projected to expand from USD 2.16 billion in 2025 and USD 2.22 billion in 2026 to USD 2.51 billion by 2031, registering a CAGR of 2.50% between 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Nordic Containerboard Market Trends and Insights

Shift From Plastic to Recyclable Fiber Packaging

The shift from plastic to recyclable fiber formats is one of the clearest supports for the Nordic containerboard market. Regulation EU 2025/40 entered into force on February 11, 2025, and its main provisions began applying from August 12, 2026, which has already changed how packaging buyers plan future material choices. Annex V of the regulation bans several single-use plastic packaging formats from January 1, 2030, including packaging for fresh produce under 1.5 kg, HORECA food service disposables, and grouped collation films, which opens more space for corrugated fiber-based substitutes. Cost-effectiveness is also important because Articles 6 and 44 tie future fee modulation to recyclability performance, creating a disadvantage for complex plastic formats that corrugated packaging does not face to the same degree. FEFCO reported in March 2026 that corrugated cardboard recycling in Europe exceeded 90%, which gives paper-based formats a strong compliance position as recyclability becomes a market-access condition. Stora Enso has also stated that customer requests for plastic-to-fiber switching are increasingly linked to PPWR recyclability rules and related single-use plastics requirements, which shows that this change is already shaping procurement decisions rather than remaining a distant policy theme.

Growth in Food and Beverage Packaging Demand

Food and beverage packaging remains a durable volume base for the Nordic containerboard market because demand in this area is less exposed to swings in discretionary spending. SCA stated in its April 2026 investor presentation that fresh food and industrial applications together account for around 25% of global containerboard demand, which supports the importance of food-related packaging in the Nordic production mix. The same presentation highlighted food-contact certified kraftliner grades at Obbola, including ISEGA-certified output, which helps preserve premium positioning in food processors' procurement. Metsa Board reported that the global packaging market grew by 3.9% annually, while paperboard was the fastest-growing material class at 4.2% over 2023 to 2028, supporting continued substitution toward fiber-based formats in packaged food applications. PPWR also bans PFAS-containing food-contact packaging from August 12, 2026, pushing buyers toward uncoated, intrinsically moisture-managed fiber substrates in categories where direct food-contact performance matters. Metsa Board further noted the weaker availability of high-quality de-inkable recycled fiber, which makes fresh fiber grades more attractive where contamination risk cannot be accepted.

Oversupply and Redirected Trade Flows in European Board Markets

The biggest near-term constraint on the Nordic containerboard market is still structural oversupply across European board markets. Billerud described this imbalance in its Q3 2025 reporting as structural rather than cyclical, indicating the company viewed the issue as driven by industry capacity conditions rather than a short-lived demand dip. The company also linked pressure in Europe to redirected trade flows after tariffs changed export routes, pushing volumes that had been targeted for North America back into the European supply base. Billerud's containerboard net sales in Europe fell to SEK 4,982 million (USD 478 million) in 2025, from SEK 5,470 million (USD 525 million) in 2024, highlighting the oversupply's impact on both prices and volume realization. The Nordic containerboard market still has advantages in forest integration and higher-performance grades, but those strengths do not fully shield producers when too much board is chasing limited demand across Europe. Recovery is likely to depend on broader capacity discipline and a firmer industrial backdrop, which means pricing relief may come later than end-market demand stabilization.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce and Parcel-Shipment Growth

- Demand for Recycled-Content Packaging in Europe

- Recovered Paper and Energy Cost Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fiber held 54.19% of the Nordic containerboard market share in 2025, maintaining its leading position. That lead rests on the region's vertically integrated forest-to-board chains and on food-contact applications, where recycled grades still face more stringent acceptance tests. In seafood, fresh produce, and chilled food packaging, contamination concerns tied to mineral oils and printing ink residues continue to limit the extent to which recovered fiber can replace fresh fiber in direct-contact or moisture-sensitive applications. SCA's kraftliner deliveries increased by 6% to 948,000 tonnes in 2025, despite a difficult European market, demonstrating that premium virgin-fiber demand remained resilient where performance and certification mattered most. Metsa Board also stated that its white kraftliners serve a top-quality niche within the 12.5 million tonne global white linerboard category, with European deliveries up 4% in 2025.

Recycled fibers remain the fastest-moving material category, with the Nordic containerboard market for recycled fibers projected to expand at a 2.81% CAGR from 2026 to 2031. Growth is centered on secondary packaging and e-commerce outer packaging, where performance needs are lower, and buyers place greater value on circularity claims. This part of the Nordic containerboard industry is benefiting from procurement standards that increasingly ask for post-consumer fiber content in transport packaging sold into European retail and distribution chains. FEFCO's March 2026 assessment confirmed that corrugated cardboard recycling in Europe already exceeds 90%, providing recycled-grade suppliers with a strong, measurable circularity message in customer discussions. The result is a clear split in the Nordic containerboard market, with recycled grades gaining traction in secondary and transit formats, while virgin fiber remains the preferred choice for food-contact, export, and higher-risk packaging conditions.

List of Companies Covered in this Report:

- Stora Enso Oyj

- Svenska Cellulosa Aktiebolaget SCA (publ)

- Smurfit Westrock plc

- Metsa Board Corporation

- Billerud Aktiebolag (publ)

- Mondi plc

- International Paper Company

- VPK Group NV

- VPK Packaging AS

- Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- Klingele Paper & Packaging SE & Co. KG

- Prinzhorn Holding GmbH

- Progroup AG

- Model Holding AG

- Ranheim Paper and Board AS

- Walki Group Oy

- Holmen AB

- Papierfabrik Palm GmbH & Co. KG

- LEIPA Georg Leinfelder GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift From Plastic to Recyclable Fiber Packaging

- 4.2.2 Growth in Food and Beverage Packaging Demand

- 4.2.3 E-Commerce and Parcel-Shipment Growth

- 4.2.4 Demand for Recycled-Content Packaging in Europe

- 4.2.5 Nordic Seafood Export Packaging Needs for Wet-Strength and Moisture-Stable Grades

- 4.2.6 Lightweighting Economics From High-Strength Nordic Virgin Fiber Grades

- 4.3 Market Restraints

- 4.3.1 Recovered Paper and Energy Cost Volatility

- 4.3.2 Packaging Minimization and Right-Sizing Under PPWR

- 4.3.3 EUDR Traceability Burden on Virgin-Fiber and Packaging Supply Chains

- 4.3.4 Oversupply and Redirected Trade Flows in European Board Markets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stora Enso Oyj

- 6.4.2 Svenska Cellulosa Aktiebolaget SCA (publ)

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Metsa Board Corporation

- 6.4.5 Billerud Aktiebolag (publ)

- 6.4.6 Mondi plc

- 6.4.7 International Paper Company

- 6.4.8 VPK Group NV

- 6.4.9 VPK Packaging AS

- 6.4.10 Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- 6.4.11 Klingele Paper & Packaging SE & Co. KG

- 6.4.12 Prinzhorn Holding GmbH

- 6.4.13 Progroup AG

- 6.4.14 Model Holding AG

- 6.4.15 Ranheim Paper and Board AS

- 6.4.16 Walki Group Oy

- 6.4.17 Holmen AB

- 6.4.18 Papierfabrik Palm GmbH & Co. KG

- 6.4.19 LEIPA Georg Leinfelder GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment