PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064400

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064400

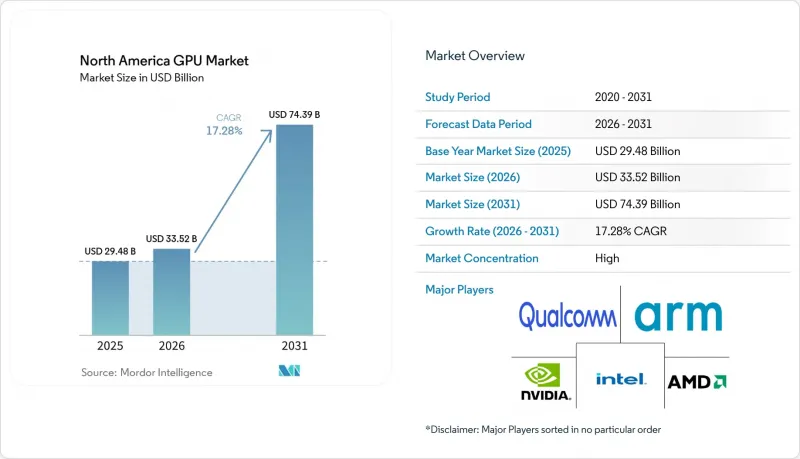

North America GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america gPU market size is projected to expand from USD 29.48 billion in 2025 and USD 33.52 billion in 2026 to reach USD 74.39 billion by 2031, registering a CAGR of 17.28% between 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and More), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America GPU Market Trends and Insights

Surging AI-Driven Datacenter GPU Procurement

Hyperscalers are compressing multi-year hardware refresh cycles to 18 months as AI model sizes grow. xAI commissioned the Colossus complex in Memphis, comprising 555,000 NVIDIA H100 GPUs that draw 150 MW and require USD 12,000 in liquid-cooling loops per rack. IREN's order for 150,000 GPUs in Texas leverages USD 0.018 kWh power, cutting operating costs by 70% relative to coastal sites. Amazon split a one-million-unit purchase between NVIDIA H200 and AMD MI325X parts to dilute supply risk and extract volume discounts. Such megablock deals raise average selling prices but make quarterly shipments volatile, as a single project delay can wipe out double-digit demand. This concentration gives the North America GPU market rapid topline growth alongside elevated forecasting risk.

Proliferation of High-Fidelity Cloud Gaming Services

Cloud platforms are shifting from shared virtualization to dedicated accelerators that sustain 4K 120 fps streams. NVIDIA's GeForce NOW Ultimate tier, built on RTX 5080 nodes, hit 15-minute queues within eight weeks, prompting a USD 400 million Oregon expansion. Microsoft's Xbox Cloud Gaming added 2.8 million regional subscribers in 2025, yet it needs 40% more GPUs per user than its rival, raising concerns about unit economics. Because each subscriber consumes disproportionate capital, operators restrain scaling until utilization models stabilize. Even so, enthusiast pricing at USD 24.99 per month keeps revenue per GPU attractive enough to sustain steady North America GPU market demand.

Supply-Chain Fragility for Advanced HBM and GDDR7 Memory

High-bandwidth memory is now the bottleneck, not lithography. SK Hynix's HBM4 yields stay below 60%, allowing only 12,000 wafer starts a month, roughly half of NVIDIA's demand for H200 accelerators. Samsung's contamination event in Q3 2025 delayed HBM3E qualification for AMD MI325X by three months. Micron's share is too small to ease shortages. GDDR7 debuted at USD 18 per GB, squeezing add-in-board margins. With three suppliers controlling the HBM market, any hiccup reverberates through the North America GPU market and curtails shipment growth.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Generative-AI PCs in Enterprise Fleets

- Expanding Automotive ADAS Compute Requirements

- Escalating Thermal-Design Power Limits in High-End GPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete accelerators captured 63.48% of the North America GPU market share in 2025 and are projected to expand at a 17.77% CAGR through 2031, underscoring their central role in hyperscale build-outs. NVIDIA's Blackwell GB200 NVL72 rack package bundles 72 GPUs and 36 Grace CPUs to deliver 1.4 exaflops of FP4 compute, a configuration that compresses cluster footprints while boosting average selling prices. AMD's MI325X, shipping since December 2025 with 192 GB of HBM3E, targets memory-bound inference tasks in which bandwidth above 5 TB s-1 becomes decisive. Intel's Ponte Vecchio seized 22% of U.S. national-lab high-performance-computing deployments during 2025, proving that an open-standard interconnect can coexist with proprietary CUDA clusters.

Beyond data centers, discrete GPUs power gaming and professional-visualization refreshes. Intel's Battlemage B580, priced at USD 249, captured a share of sub-USD 300 desktop units within 90 days, demonstrating price elasticity among cost-sensitive gamers. Rumors place NVIDIA's RTX 5090 at 24,576 CUDA cores and 28 GB of GDDR7, a 40% compute leap over the RTX 4090, widening the gap with integrated solutions. Apple's M-series iGPUs now offer hardware ray tracing, but thermal constraints limit their performance to workloads below 75 W, leaving high-end rendering and simulation to discrete GPUs. As a result, the discrete tier remains the revenue locomotive for the North America GPU market, even as integrated NPUs shoulder light generative AI tasks.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Arm Holdings plc

- Apple Inc.

- Samsung Electronics Co Ltd.

- Imagination Technologies Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co Ltd (MSI)

- Gigabyte Technology Co Ltd

- Zotac Technology Ltd

- Sapphire Technology Ltd

- PowerColor Technology Inc.

- Xilinx Inc. (AMD Adaptive Computing)

- Tenstorrent Inc.

- Graphcore Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI-Driven Datacenter GPU Procurement

- 4.2.2 Proliferation of High-Fidelity Cloud Gaming Services

- 4.2.3 Rapid Adoption of Generative-AI PCs in Enterprise Fleets

- 4.2.4 Expanding Automotive ADAS Compute Requirements

- 4.2.5 Advancements in Chiplet and 3D-Stacked GPU Architectures

- 4.2.6 Government Incentives for Domestic Semiconductor Capacity

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Fragility for Advanced HBM and GDDR7 Memory

- 4.3.2 Escalating Thermal-Design Power Limits in High-End GPUs

- 4.3.3 Intensifying US-China Tech Export Controls

- 4.3.4 Volatility in Esports and Consumer Upgrade Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Arm Holdings plc

- 6.4.6 Apple Inc.

- 6.4.7 Samsung Electronics Co Ltd.

- 6.4.8 Imagination Technologies Ltd.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star International Co Ltd (MSI)

- 6.4.11 Gigabyte Technology Co Ltd

- 6.4.12 Zotac Technology Ltd

- 6.4.13 Sapphire Technology Ltd

- 6.4.14 PowerColor Technology Inc.

- 6.4.15 Xilinx Inc. (AMD Adaptive Computing)

- 6.4.16 Tenstorrent Inc.

- 6.4.17 Graphcore Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment