PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065496

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065496

Hyperscale Data Center Graphics Processing Unit (GPU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

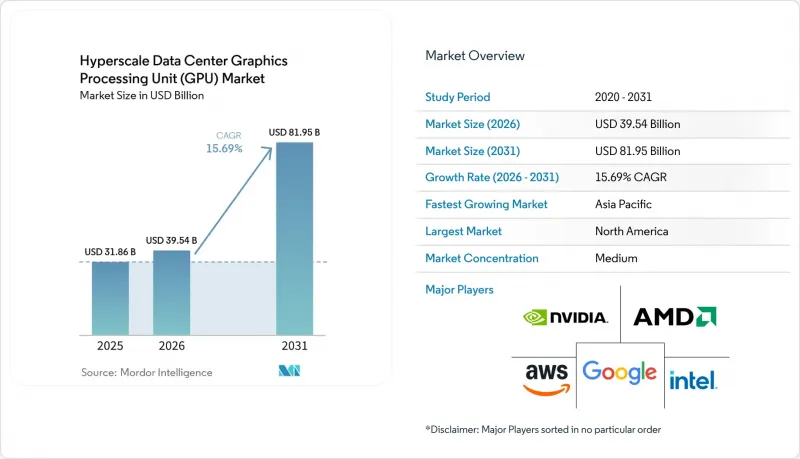

According to Mordor Intelligence, the hyperscale data center GPU market size is projected to expand from USD 31.86 billion in 2025 and USD 39.54 billion in 2026 to USD 81.95 billion by 2031, registering a 15.69% CAGR between 2026 and 2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Hyperscale Data Center Graphics Processing Unit (GPU) Market Trends and Insights

Proliferation Of AI And ML Workloads In Cloud Data Centers

Cloud platforms have converted GPUs from specialist accelerators into baseline infrastructure. New AI-optimized virtual machines on Microsoft Azure and Trainium2 instances on AWS lowered entry barriers for enterprise customers migrating legacy machine-learning pipelines. Capital allocations reflect permanence rather than experimentation; Meta reserved USD 65 billion for AI compute in 2026, chiefly for multimodal training clusters. Power density has surged 10-20-fold versus traditional servers, forcing data-center redesigns that integrate rack-level liquid cooling and revised power distribution. Workload diversity now spans vision, recommendation, and autonomy, each demanding a mix of inference-optimized cards and training-grade units, ensuring the Hyperscale data center GPU market remains on a structurally rising curve.

Rapid Scaling of Generative AI Model Training Clusters

Parameter growth from billions to trillions is compelling operators to assemble petaflop-scale clusters. xAI's Memphis complex is scaling toward 1 million GPUs by 2027, and Mistral AI's Paris facility replicates this model in Europe. Centralization maximizes equipment utilization and amortizes capex across successive model iterations, but only hyperscalers can fund the USD-billion class builds. Technically, liquid cooling and fabrics such as NVLink 5.0 cut inter-GPU latency below one microsecond, allowing 70-plus-GPU trays to appear as a single logical device. The result is a multiplier effect on the Hyperscale data center GPU market, with every uplift in model size translating to a disproportionate lift in cluster capacity.

High Capital Expenditure for Hyperscale GPU Clusters

A single rack of Blackwell GB200 NVL72 lists between USD 3 million and USD 4 million before facility costs. Oracle's USD 6.5 billion rollout underlines the minimum price of admission, while recurring power bills can hit USD 10 million per year for a 10 MW cluster. Utilization averaging 60%-70% obliges providers to overbuild capacity, extending payback periods, and squeezing mid-tier clouds. Consequently, only the largest operators with access to low-cost renewable energy can compete at the training frontier, tempering near-term growth for the Hyperscale data center GPU market.

Other drivers and restraints analyzed in the detailed report include:

- Transition Toward Heterogeneous Computing Architectures

- Growing Demand for Cloud Gaming And 3-D Graphics Workloads

- Supply Chain Bottlenecks in Advanced Packaging and HBM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities captured a 19.3% CAGR outlook versus mid-teens growth for centralized hyperscale hubs, reflecting the widening role of real-time inference in vehicles, smart-city sensors, and industrial robotics. The Hyperscale data center GPU market size linked to cloud sites remains dominant, yet its share inches lower as operators like AWS Outposts deliver cloud management on-premises. In practice, a dual-architecture equilibrium is emerging where 100-MW mega-facilities train trillion-parameter models while 1-MW micro-pods push decisions to within 10 ms of users.

Capital allocation favors both ends of the spectrum. Amazon's USD 200 billion through 2030 addresses mega-sites, whereas NVIDIA's IGX Orin shipments illustrate strong OEM appetite for edge appliances. Financial services and healthcare firms keep modest private clusters to satisfy data-sovereignty rules, a niche that still feeds the wider Hyperscale data center GPU market. As utilization analytics improve, some inference loads are expected to bounce between edge and core depending on regional demand curves.

Training-grade boards accounted for 56.7% of revenue in 2025, anchoring the cash flow engine for vendors. Yet inference-centric devices with lower precision and power budgets are growing rapidly, aided by hyperscaler in-house silicon. Inference GPUs should grow 18.5% annually, mirroring the doubling cadence of model sizes that force disaggregation across thousands of cards.

The Hyperscale data center GPU market size for inference hardware remains smaller but could exceed 40% of the total value by 2031 if conversational AI, retrieval-augmented generation, and real-time co-pilots permeate mainstream software. NVIDIA's L4, AWS Inferentia2, and Google TPU v5e exemplify the economics: fewer flops per watt but superior cost per request. Training clusters, then, reprioritize cutting-edge memory bandwidth, securing a two-tier product mix in which last-year silicon enjoys a lucrative afterlife as an inference workhorse.

Geography Analysis

North America retained a 42.8% revenue share in 2025 and continues to wield unparalleled purchase power as Amazon, Microsoft, Google, and Meta funnel USD-hundreds-of-billions into AI capacity. Export controls that restrict top-tier GPU shipments to China inadvertently redirect a larger slice of the limited supply toward domestic sites, bolstering the region's command of the Hyperscale data center GPU market. Canadian clusters in Toronto and Montreal enjoy low-cost hydroelectricity and university-sourced talent, while Mexico's budding near-shoring economy is catalyzing edge nodes tailored to logistics robotics.

Asia-Pacific is the fastest riser at a forecast 17.8% CAGR. China's home-grown Ascend 910C fills the void left by U.S. sanctions, allowing Alibaba, Tencent, and Baidu to keep pace in large language model rollouts. Japan's JPY 2 trillion subsidy pool (USD 13.4 billion) underwrites domestic clusters, and South Korea leverages HBM leadership for vertical integration spanning memory through accelerator. India's metro triad, Bangalore, Hyderabad, Mumbai, anchors sovereign AI ambitions, while Southeast Asian capitals harvest fresh edge deployments after Singapore partially lifted its data-center freeze.

Europe's prospects hinge on stringent energy directives that cap PUE at 1.3 for new builds. Germany and the Nordics retrofit facilities with immersion and rear-door cooling to host high-density racks. The United Kingdom's AI Safety Institute buys 5,000 GPUs to audit frontier models, while France's Mistral AI plants a Blackwell campus inside Paris's city limits. Renewable abundance lures operators to southern Spain and Italy, although deployment timelines remain tied to grid-upgrade schedules. Other regions, South America and the Middle East and Africa, collectively account for less than one-tenth of current value, yet Saudi Arabia's USD 20 billion NEOM blueprint and South Africa's Johannesburg edge pods foreshadow pockets of high-growth demand that will enrich the global Hyperscale data center GPU market footprint.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Alibaba Group Holding Limited (Alibaba Cloud)

- Tencent Holdings Ltd. (Tencent Cloud)

- Baidu, Inc.

- Oracle Corporation

- Huawei Technologies Co., Ltd.

- Graphcore Ltd.

- Super Micro Computer, Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Inspur Information Technology Co., Ltd.

- Gigabyte Technology Co., Ltd.

- ASUStek Computer Inc.

- Penguin Computing, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI and ML Workloads in Cloud Data Centers

- 4.2.2 Rapid Scaling of Generative AI Model Training Clusters

- 4.2.3 Transition Toward Heterogeneous Computing Architectures

- 4.2.4 Growing Demand for Cloud Gaming and 3-D Graphics Workloads

- 4.2.5 Emergence of Chiplet-Based Disaggregated GPU Designs

- 4.2.6 Adoption of Liquid Cooling for High-Density GPU Racks

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for Hyperscale GPU Clusters

- 4.3.2 Supply Chain Bottlenecks in Advanced Packaging and HBM

- 4.3.3 Rising Regulatory Pressure on Data-Center Energy Use

- 4.3.4 Geopolitical Export Controls Limiting GPU Availability

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC)

- 5.4.3 Data Analytics

- 5.4.4 Graphics and Visualization

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Amazon Web Services, Inc.

- 6.4.5 Microsoft Corporation

- 6.4.6 Google LLC

- 6.4.7 Alibaba Group Holding Limited (Alibaba Cloud)

- 6.4.8 Tencent Holdings Ltd. (Tencent Cloud)

- 6.4.9 Baidu, Inc.

- 6.4.10 Oracle Corporation

- 6.4.11 Huawei Technologies Co., Ltd.

- 6.4.12 Graphcore Ltd.

- 6.4.13 Super Micro Computer, Inc.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 Hewlett Packard Enterprise Company

- 6.4.16 Lenovo Group Limited

- 6.4.17 Inspur Information Technology Co., Ltd.

- 6.4.18 Gigabyte Technology Co., Ltd.

- 6.4.19 ASUStek Computer Inc.

- 6.4.20 Penguin Computing, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment