PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064464

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064464

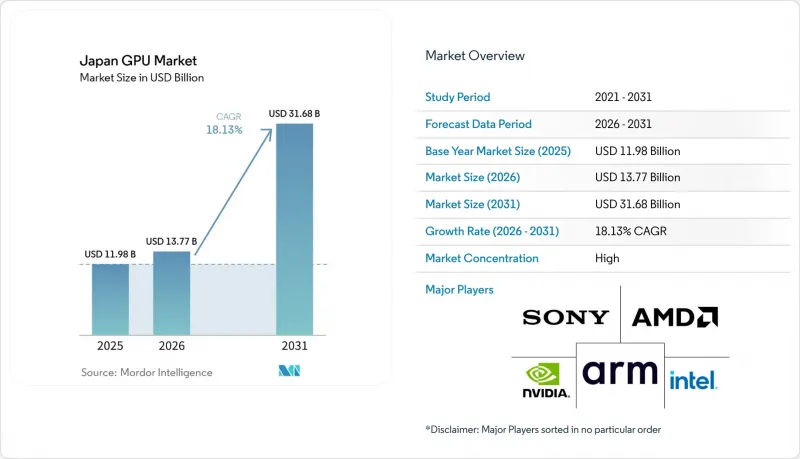

Japan GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan gPU market size is expected to increase from USD 11.98 billion in 2025 to USD 13.77 billion in 2026 and reach USD 31.68 billion by 2031, growing at a CAGR of 18.13% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Japan GPU Market Trends and Insights

Surging AI/ML Training Workloads Across Japanese Enterprises

Compliance with the Act on the Protection of Personal Information is steering banks, automakers, and life-science firms toward sovereign datacenters equipped with high-end accelerators. Subsidies under the GENIAC program cut capital outlays, letting regional cloud providers such as SAKURA Internet and KDDI deploy racks of NVIDIA H200 cards without offshoring sensitive data. SoftBank's 1,000-GPU cluster and Microsoft's USD 10 billion infrastructure pledge further anchor demand. Toyota's Woven City simulation hub alone consumed more than 500 A100S in 2025, underscoring how R&D workloads now hinge on domestic capacity.

Government Subsidies for Domestic Semiconductor Supply Chain Re-Shoring

The Ministry of Economy, Trade and Industry has earmarked JPY 1.23 trillion (USD 7.97 billion) for wafer fabs, channeling JPY 732 billion into TSMC's Kumamoto site and JPY 920 billion into Rapidus' 2-nm line. TSMC began 3-nm output in late 2025, shipping substrates for AMD Instinct MI300 cards, while Rapidus targets 2-nm production by 2027. JP. Although yields will take years to mature, the roadmap promises mid-decade relief from overseas dependency, positioning local integrators to capture supply closer to home.

Ongoing 2 nm/3 nm Process Node Capacity Shortages

TSMC's CoWoS lines now run at near-full load, stretching lead times for Blackwell and Hopper GPUs to as long as 78 weeks. Apple, NVIDIA, and AMD have already block-booked 2-nm slots through 2027, denying Japanese fabless start-ups early access. Samsung's 3-nm yields remain under 85%, deterring customers from diversifying supply. Until Rapidus ramps, integrators must elongate product cycles or revert to prior-generation silicon.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Automotive SoCs Integrating GPU-Based Vision for ADAS

- Rapid Uptake of Generative-AI-Enabled Mobile Apps

- Energy-Efficiency Regulations Limiting Datacenter Power Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs captured 67.59% of 2025 revenue, highlighting their primacy in large-scale AI training within the Japan GPU market share. Ongoing migration to NVIDIA's Blackwell platform, with 208 billion transistors and 10 TB/s NVLink, cements this lead as hyperscalers fill racks with upgradeable add-in boards. AMD's MI350X provides a cost-advantaged option for inference, helping cloud challengers diversify vendor exposure. Meanwhile, integrated GPUs prevail in thermally constrained environments such as ultraportable notebooks and automobiles. Renesas R-Car Gen 5 will propel integrated units into higher tiers of driver-assistance from 2027, albeit without threatening the performance gulf that datacenter workloads demand.

Budget-sensitive workstations and esports cafes still prefer discrete cards to hit 400-Hz frame rates, while mobile and tablet designs rely on SoC-embedded graphics to balance battery life. Apple's M4 and Qualcomm's Snapdragon X Elite chipsets now match entry-level discrete throughput, signaling eventual convergence in low-power segments. Nevertheless, memory bandwidth ceilings keep integrated architectures from replacing dedicated accelerators at the top end. Therefore, discrete units will remain the principal revenue engine for the Japan GPU market size through 2031.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Sony Group Corporation

- Nintendo Co., Ltd.

- Fujitsu Limited

- NEC Corporation

- Arm Ltd.

- Qualcomm Incorporated

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- ZOTAC Technology Limited

- Acer Incorporated

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Imagination Technologies Limited

- Renesas Electronics Corporation

- Broadcom Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI/ML Training Workloads Across Japanese Enterprises

- 4.2.2 Government Subsidies for Domestic Semiconductor Supply Chain Re-Shoring

- 4.2.3 Esports-Led Boom in High-Frame-Rate PC Gaming Cafes

- 4.2.4 Rapid Uptake of Generative-AI-Enabled Mobile Apps

- 4.2.5 Expansion of Automotive SoCs Integrating GPU-Based Vision for ADAS

- 4.2.6 Growth of Immersive 3D Design Tools in Japan's Manufacturing Sector

- 4.3 Market Restraints

- 4.3.1 Ongoing 2 nm/3 nm Process Node Capacity Shortages

- 4.3.2 Energy-Efficiency Regulations Limiting Datacenter Power Budgets

- 4.3.3 Yen Volatility Raising Imported GPU ASPs

- 4.3.4 Export-Control Restrictions on High-End AI Accelerators

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Existing Competitors

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Sony Group Corporation

- 6.4.5 Nintendo Co., Ltd.

- 6.4.6 Fujitsu Limited

- 6.4.7 NEC Corporation

- 6.4.8 Arm Ltd.

- 6.4.9 Qualcomm Incorporated

- 6.4.10 ASUSTeK Computer Inc.

- 6.4.11 Giga-Byte Technology Co., Ltd.

- 6.4.12 Micro-Star International Co., Ltd. (MSI)

- 6.4.13 Dell Technologies Inc.

- 6.4.14 Hewlett Packard Enterprise Company

- 6.4.15 Lenovo Group Limited

- 6.4.16 ZOTAC Technology Limited

- 6.4.17 Acer Incorporated

- 6.4.18 Apple Inc.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 Imagination Technologies Limited

- 6.4.21 Renesas Electronics Corporation

- 6.4.22 Broadcom Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment