PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064542

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064542

India GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

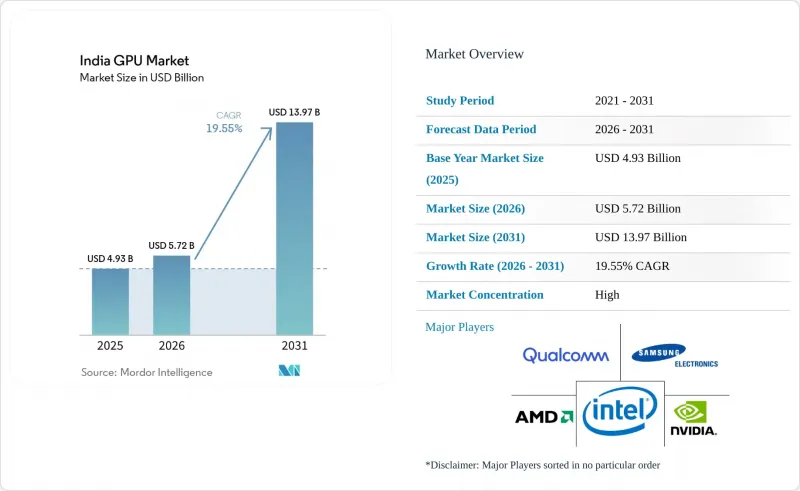

According to Mordor Intelligence, the india gPU market size is expected to increase from USD 4.93 billion in 2025 to USD 5.72 billion in 2026 and reach USD 13.97 billion by 2031, growing at a CAGR of 19.55% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, and Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded, and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

India GPU Market Trends and Insights

Growing Cloud Service Provider Investments in Indian Hyperscale DCs

Hyperscale operators now treat India as a strategic compute region rather than a cost-arbitrage outpost. Microsoft's multi-region rollout features NVIDIA H100 and forthcoming Blackwell GPUs, while Google is expanding TPU- and GPU-accelerated infrastructure for enterprise AI workloads. Domestic provider Yotta Infrastructure is deploying more than 32,000 H100 units with an upgrade path to Blackwell Ultra, signaling a pivot from general-purpose cloud to inference-optimized clusters. The IndiaAI Mission sets aside public funding for 34,000 sovereign GPUs, reducing reliance on foreign clouds. Collectively, these moves underpin sustained double-digit growth for the India GPU market.

Proliferation of AI Workloads in Edge Devices

Edge inference has graduated from proof-of-concept to volume rollout across retail analytics, industrial vision, and public safety. Qualcomm's Snapdragon 8 Elite Gen 5 delivers a 23% graphics uplift, enabling on-device generative AI for flagship smartphones, while MediaTek's Dimensity 9500s brings ray-tracing hardware to mid-premium tiers. Tier-2 smart-city projects leverage edge GPU nodes to meet sub-50 ms latency budgets. The National Payments Corporation of India uses GPU-accelerated models to screen 12 billion monthly payment transactions, demonstrating mission-critical edge inference at a national scale.

Chronic Import Dependence for Advanced Nodes

India lacks sub-28 nm fabrication, so datacenter GPUs manufactured on 4 nm and below must be imported. GPUs represent roughly 90% of AI server bills of materials, making supply allocation decisions by overseas foundries a critical bottleneck. Long lead times, coupled with limited local high-bandwidth memory packaging, amplify vulnerability to geopolitical shocks.

Other drivers and restraints analyzed in the detailed report include:

- Government PLI Schemes for Semiconductor Manufacturing

- Rapid Expansion of India's Gaming Ecosystem

- Global Supply Chain Disruptions Causing Allocation Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs accounted for 66.18% of the India GPU market share in 2025. Servers, gaming PCs, and professional workstations have gravitated to dedicated silicon that provides higher memory bandwidth and specialized tensor math. Large-scale installations, such as Yotta's 32,000-plus H100 cluster, illustrate enterprise appetite for top-bin accelerators. Enthusiast gamers are migrating from GTX 1060-class hardware to RTX 50-series cards, aided by board partners that bundle factory overclocks and extended warranties. On the professional side, CAD and media-creation suites exploit driver-certified Quadro and Radeon Pro lines, supporting higher average selling prices.

Integrated GPUs, holding the remaining 33.82%, dominate unit shipments in mainstream laptops and smartphones, where thermals and bill-of-materials ceilings are stringent. Intel Iris Xe and AMD Radeon 700M graphics meet everyday productivity and light creative workloads. In smartphones, Qualcomm Adreno and MediaTek Immortalis cores now handle on-device diffusion models and NPU-assisted photography. The India GPU market size for integrated silicon will continue to climb in absolute terms, although its slice of revenue tilts toward discrete devices because of rising datacenter volumes.

List of Companies Covered in this Report:

- Advanced Micro Devices Inc.

- Intel Corporation

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- Imagination Technologies Ltd.

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Colorful Technology Co. Ltd.

- Zotac Technology Ltd.

- Palit Microsystems Ltd.

- Sapphire Technology Ltd.

- InnoVision Multimedia Ltd.

- Ineda Systems Pvt. Ltd.

- Saankhya Labs Pvt. Ltd.

- ARM Ltd.

- Xilinx India Technology Services Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI Workloads in Edge Devices

- 4.2.2 Rapid Expansion of India's Gaming Ecosystem

- 4.2.3 Government PLI Schemes for Semiconductor Manufacturing

- 4.2.4 Rising Demand for High-Performance Computing in BFSI

- 4.2.5 Data-Driven Automotive ADAS Adoption

- 4.2.6 Growing Cloud Service Provider Investments in Indian Hyperscale DCs

- 4.3 Market Restraints

- 4.3.1 Chronic Import Dependence for Advanced Nodes

- 4.3.2 Electricity Cost Volatility Impacting Datacenter TCO

- 4.3.3 Limited Domestic IP for GPU Design Talent Pool

- 4.3.4 Global Supply Chain Disruptions Causing Allocation Shortages

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Advanced Micro Devices Inc.

- 6.4.2 Intel Corporation

- 6.4.3 NVIDIA Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Imagination Technologies Ltd.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 MediaTek Inc.

- 6.4.8 Apple Inc.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star International Co. Ltd.

- 6.4.11 Gigabyte Technology Co. Ltd.

- 6.4.12 Colorful Technology Co. Ltd.

- 6.4.13 Zotac Technology Ltd.

- 6.4.14 Palit Microsystems Ltd.

- 6.4.15 Sapphire Technology Ltd.

- 6.4.16 InnoVision Multimedia Ltd.

- 6.4.17 Ineda Systems Pvt. Ltd.

- 6.4.18 Saankhya Labs Pvt. Ltd.

- 6.4.19 ARM Ltd.

- 6.4.20 Xilinx India Technology Services Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment