PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065493

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065493

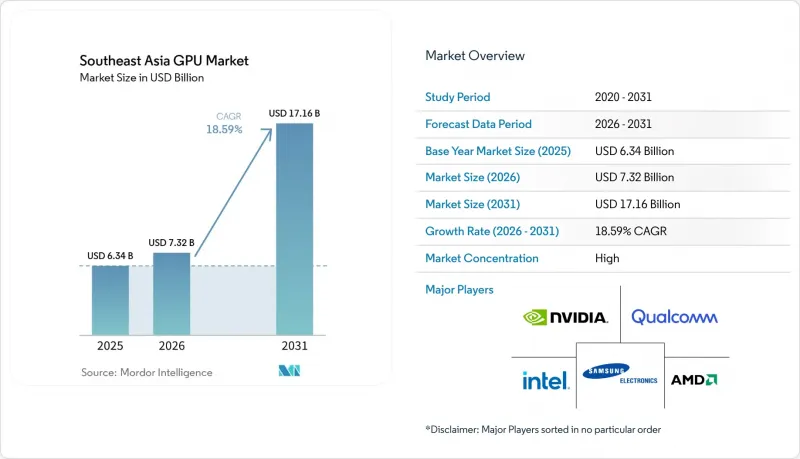

Southeast Asia GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the southeast asia gPU market size is expected to increase from USD 7.32 billion in 2026 to USD 17.16 billion by 2031, growing at a CAGR of 18.59% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs), and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Southeast Asia GPU Market Trends and Insights

Rising Demand for High-Performance Computing in Data Centers

Hyperscalers have started localizing compute clusters to satisfy data-residency mandates and reduce latency for generative AI inference. Microsoft Azure rolled out ND GB200-v6 instances in Malaysia and Indonesia in 2025, while Google Cloud launched a Bangkok region with A3 nodes powered by H100 GPUs the same year. YTL Power International broke ground on a 500 MW AI campus in Johor, scheduled for 2027 completion, and regional colocation providers are retrofitting halls with liquid cooling. These moves establish Southeast Asia as a first-tier inference hub rather than a spoke served out of Singapore.

Rapid Adoption of Cloud Gaming and Online Esports

Fiber-to-the-home penetration and nationwide 5G coverage have enabled sub-20 ms gameplay for subscription-based cloud gaming services. Radian Arc and Singtel-Razer pilots moved from trial to commercial launch during 2024-2025, with monthly pricing under USD 10 proving critical for scale. Esports' inclusion as a medal event in the Southeast Asian Games 2025 triggered public-sector investment in GPU-equipped training centers, spurring near-term purchases of workstation-class cards across Thailand and the Philippines.

Global GPU Supply Chain Disruptions and Chip Shortages

HBM3E memory remained constrained through 2025, compelling NVIDIA and AMD to ration flagship accelerators to hyperscalers on multi-year contracts. Lead times for regional cloud providers stretched beyond six months, and CoWoS packaging capacity at TSMC exceeded 90% utilization. U.S. export controls imposed a 50,000-unit ceiling on datacenter GPUs shipped to Indonesia for 2025-2027, forcing enterprises to emphasize inference over training.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of AI-Powered Content Creation for Social Commerce

- Growth of Mobile Gaming Ecosystem in Southeast Asia

- Rising Average Selling Prices Limiting Entry-Level Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete units controlled 67.85% of the Southeast Asia GPU market in 2025, a position amplified by datacenter clusters built around NVIDIA H200 and AMD MI325X accelerators. The Southeast Asia GPU market size for discrete units is on track to expand at a 19.11% CAGR through 2031 as hyperscalers lock in multi-year supply agreements. YTL Power International's 500 MW Johor facility alone plans to host tens of thousands of cards, while automotive OEMs such as Volvo integrate dual Drive AGX Orin boards that deliver 254 TOPS per vehicle.

Smaller but rising, integrated GPUs ride smartphone and AI PC shipments. MediaTek's 9500s embeds an Immortalis-G925 core with hardware ray tracing, trimming the gap with entry-level discrete boards. Qualcomm's Snapdragon 8 Gen 3 and MediaTek's 8500 sustain 60 fps on popular mobile titles, underscoring that integrated silicon now handles workloads once reserved for add-in cards.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- ARM Holdings plc

- Imagination Technologies Limited

- Apple Inc.

- Huawei Technologies Co., Ltd.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Acer Incorporated

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- EVGA Corporation

- Zotac Technology Limited

- Colorful Technology Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud Gaming and Online Esports

- 4.2.2 Rising Demand for High-Performance Computing in Data Centers

- 4.2.3 Growth of Mobile Gaming Ecosystem in Southeast Asia

- 4.2.4 Increasing Graphics Requirements for AAA PC and Console Titles

- 4.2.5 Government Incentives for Local Semiconductor Packaging and Testing

- 4.2.6 Expansion of AI-Powered Content Creation for Social Commerce

- 4.3 Market Restraints

- 4.3.1 Global GPU Supply Chain Disruptions and Chip Shortages

- 4.3.2 Rising Average Selling Prices Limiting Entry-Level Adoption

- 4.3.3 Energy Cost Sensitivity of Emerging Country Data Centers

- 4.3.4 Regulatory Scrutiny on Cryptocurrency Mining in Key Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Threat of New Entrants

- 4.8.3 Threat of Substitutes

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Bargaining Power of Buyers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 MediaTek Inc.

- 6.4.7 ARM Holdings plc

- 6.4.8 Imagination Technologies Limited

- 6.4.9 Apple Inc.

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Lenovo Group Limited

- 6.4.12 ASUSTeK Computer Inc.

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Gigabyte Technology Co., Ltd.

- 6.4.15 Acer Incorporated

- 6.4.16 Dell Technologies Inc.

- 6.4.17 Hewlett Packard Enterprise Company

- 6.4.18 EVGA Corporation

- 6.4.19 Zotac Technology Limited

- 6.4.20 Colorful Technology Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment