PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065617

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065617

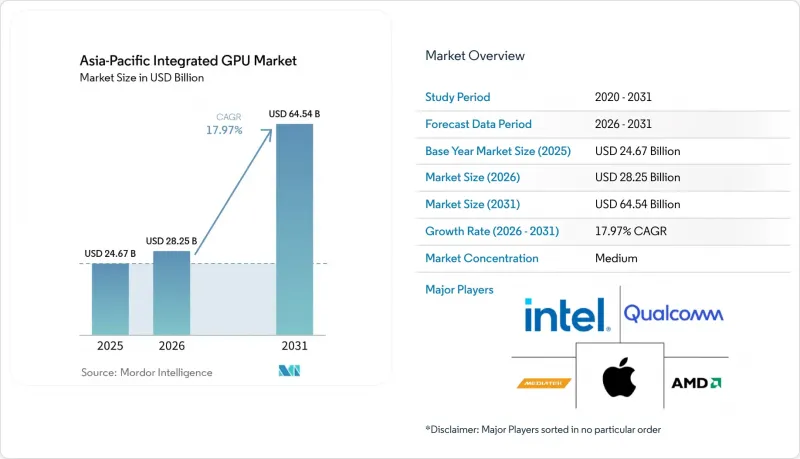

Asia-Pacific Integrated GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific integrated GPU market size is expected to grow from USD 24.67 billion in 2025 to USD 28.25 billion in 2026 and is forecast to reach USD 64.54 billion by 2031 at 17.97% CAGR over 2026-2031.

This report is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs (Smartphones and Tablets), Embedded and Industrial SoCs, and More), Performance Tier (Entry-Level (Less Than USD 50), Mainstream (USD 50 - USD 150), Performance (USD 150 - USD 300), and High-Performance (Greater Than USD 300)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Integrated GPU Market Trends and Insights

Windows 11 and AI PC Refresh Cycle in Commercial Notebooks

The Windows 10 support deadline became the clearest near-term trigger for the Asia-Pacific integrated GPU market in commercial PCs. Notebook replacement moved faster than in prior upgrade cycles because enterprise buyers had to align operating system migration with new AI-ready hardware specifications. HP said AI PC shipment mix increased from 35% to 44%, and the Windows 11 refresh cycle in APJ contributed a 2-3% commercial demand pull-forward, which shows that buyers were already moving toward higher-spec systems before the full migration wave had ended. Intel then reinforced that shift when it launched Core Ultra Series 3 in January 2026 with 180 TOPS of total platform AI compute, which turned the integrated graphics block into a practical AI workload enabler rather than a basic display component. As a result, the Asia-Pacific integrated GPU market is benefiting from a higher specification floor in commercial notebooks, especially in Japan, China, South Korea, India, and Australia.

5G Smartphone Premiumization and On-Device AI Graphics Demand

Smartphone graphics in the Asia-Pacific integrated GPU market are no longer being designed only for rendering and media playback. MediaTek said the Dimensity 9500 integrated the Arm G1-Ultra GPU with 33% higher peak performance and 42% better power efficiency than the prior generation, while also supporting 120fps ray-traced gaming.MediaTek also described an agentic AI framework that distributes generative AI tasks across GPU shader resources and dedicated neural acceleration, which expands local AI capability beyond the flagship tier. This changes how handset makers position premium and upper mid-range devices, because graphics performance now supports gaming, AI responsiveness, and power efficiency at the same time. The Asia-Pacific integrated GPU market therefore gains from 5G-led premiumization in China, India, South Korea, and Southeast Asia, where stronger on-device AI capability is becoming a selling point in mainstream consumer upgrades.

Advanced-Node Foundry Bottlenecks for Premium SoCs

Advanced-node supply remains a real constraint for the Asia-Pacific integrated GPU market because the same leading-edge wafers are needed by top smartphone, PC, and AI compute programs. Premium SoC vendors therefore face a more rigid allocation environment, especially when the largest customers lock in early access and smaller challengers depend on shorter planning windows. This raises wafer and packaging costs, which then feeds into device pricing and narrows the flexibility of vendors trying to scale new performance-tier designs. It also slows competitive rotation, because foundry access starts to matter almost as much as architecture quality in premium segments. The Asia-Pacific integrated GPU market can still grow under these conditions, but supply discipline is likely to keep the premium tier tighter than underlying demand through the current planning cycle.

Other drivers and restraints analyzed in the detailed report include:

- Ray Tracing and Console-Class Mobile Gaming Migration

- Unified Memory Architectures Expand Creator-Class iGPU Workloads

- Slow Monetization of AI PC Use Cases in Price-Sensitive Segments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile SoCs held 49.32% of Asia-Pacific integrated GPU market share in 2025, which kept the region's revenue base centered on smartphones and tablets. This leadership reflects the region's structural role in both smartphone manufacturing and consumption, with Chinese and Korean OEM ecosystems driving persistent demand for SoCs that integrate graphics, AI, and connectivity in the same package. Desktop and laptop processors formed the second-largest device category, supported by the commercial notebook refresh cycle and continued notebook-heavy buying patterns in work and education devices. The Asia-Pacific integrated GPU market therefore remained anchored in high-volume consumer electronics, even as PCs regained strategic importance because AI-readiness became a more visible purchase factor.

The Asia-Pacific integrated GPU market size for server and data center processors with integrated graphics is projected to expand at an 18.11% CAGR from 2026 to 2031, making this the fastest-growing device category. That growth is linked to rising interest in edge inference nodes, where operators want lower cost, easier deployment, and better power efficiency than purpose-built discrete accelerators can always provide. Intel said Core Ultra Series 3 delivered up to 1.9x higher large language model performance than NVIDIA Jetson Orin AGX 64GB and up to 4.5x higher vision language action model throughput in robotic workloads, which highlights why integrated server-class graphics are gaining attention beyond the PC space. As cloud and enterprise users across China, Japan, and South Korea expand localized AI processing, this category is reshaping the Asia-Pacific integrated GPU market from a primarily client-device story into a broader compute platform story.

List of Companies Covered in this Report:

- Intel Corporation

- Advanced Micro Devices, Inc.

- Qualcomm Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- HiSilicon (Shanghai) Technologies Co., LTD.

- UNISOC (Shanghai) Technologies Co., Ltd.

- Xiaomi Corporation

- Arm Holdings plc

- Imagination Technologies Group plc

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Rockchip Electronics Co., Ltd.

- Amlogic Co., Ltd.

- Socionext Inc.

- STMicroelectronics N.V.

- Broadcom Inc.

- Allwinner Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

5 Market Overview

- 5.1 Market Drivers

- 5.1.1 Windows 11 and AI PC Refresh Cycle in Commercial Notebooks

- 5.1.2 5G Smartphone Premiumization and On-Device AI Graphics Demand

- 5.1.3 Ray Tracing and Console-Class Mobile Gaming Migration

- 5.1.4 Unified Memory Architectures Expand Creator-Class iGPU Workloads

- 5.1.5 Education Device Procurement in India and Southeast Asia

- 5.1.6 Local Assembly and Semiconductor Incentives Improve SoC Economics

- 5.2 Market Restraints

- 5.2.1 Advanced-Node Foundry Bottlenecks for Premium SoCs

- 5.2.2 Slow Monetization of AI PC Use Cases in Price-Sensitive Segments

- 5.2.3 Advanced Packaging Capacity Prioritizes AI Accelerators Over iGPUs

- 5.2.4 China Export Controls and Localization Friction

- 5.3 Industry Value Chain Analysis

- 5.4 Regulatory Landscape

- 5.5 Technological Outlook

- 5.6 Porter's Five Forces Analysis

- 5.6.1 Threat of New Entrants

- 5.6.2 Bargaining Power of Suppliers

- 5.6.3 Bargaining Power of Buyers

- 5.6.4 Threat of Substitutes

- 5.6.5 Intensity of Competitive Rivalry

- 5.7 Impact of Macroeconomic Factors on the Market

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Device Category

- 6.1.1 Desktop and Laptop Processors

- 6.1.2 Mobile SoCs (Smartphones and Tablets)

- 6.1.3 Embedded and Industrial SoCs

- 6.1.4 Server and Data Center Processors with Integrated Graphics

- 6.2 By Performance Tier

- 6.2.1 Entry-Level (Less than USD 50)

- 6.2.2 Mainstream (USD 50 - USD 150)

- 6.2.3 Performance (USD 150 - USD 300)

- 6.2.4 High-Performance (Greater than USD 300)

- 6.3 By Geography

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 South Korea

- 6.3.5 Taiwan

- 6.3.6 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 7.4.1 Intel Corporation

- 7.4.2 Advanced Micro Devices, Inc.

- 7.4.3 Qualcomm Incorporated

- 7.4.4 Apple Inc.

- 7.4.5 MediaTek Inc.

- 7.4.6 Samsung Electronics Co., Ltd.

- 7.4.7 HiSilicon (Shanghai) Technologies Co., LTD.

- 7.4.8 UNISOC (Shanghai) Technologies Co., Ltd.

- 7.4.9 Xiaomi Corporation

- 7.4.10 Arm Holdings plc

- 7.4.11 Imagination Technologies Group plc

- 7.4.12 NXP Semiconductors N.V.

- 7.4.13 Renesas Electronics Corporation

- 7.4.14 Texas Instruments Incorporated

- 7.4.15 Rockchip Electronics Co., Ltd.

- 7.4.16 Amlogic Co., Ltd.

- 7.4.17 Socionext Inc.

- 7.4.18 STMicroelectronics N.V.

- 7.4.19 Broadcom Inc.

- 7.4.20 Allwinner Technology Co., Ltd.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment