PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064403

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064403

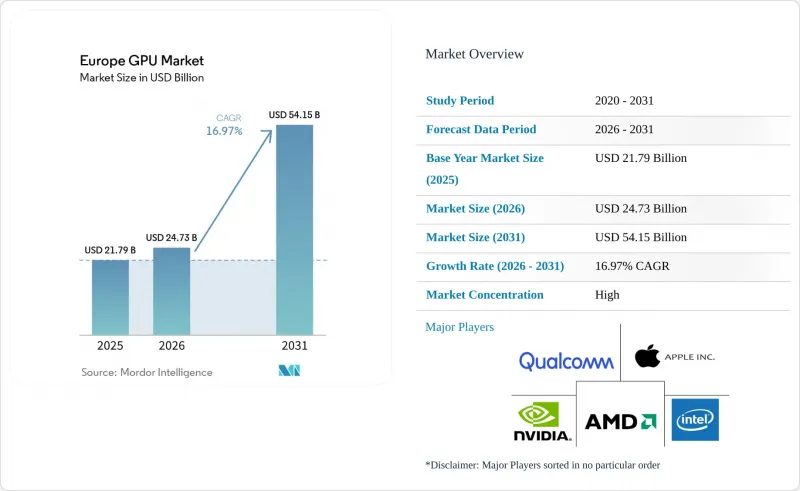

Europe GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe gPU market size is projected to be USD 21.79 billion in 2025, USD 24.73 billion in 2026, and reach USD 54.15 billion by 2031, growing at a CAGR of 16.97% from 2026 to 2031.

This report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and More), and Country (Germany, United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe GPU Market Trends and Insights

Accelerated Adoption of AI And ML Workloads in European Datacenters

Large-scale commitments totaling USD 42.3 billion from the United Kingdom, together with multi-gigawatt projects in France, are adding tens of thousands of NVIDIA Blackwell and AMD Instinct accelerators to regional server racks. OpenAI's Stargate UK, Microsoft's supercomputer build-out, and France-based deployments by Mistral AI and Sesterce illustrate how public and private investments align with data-sovereignty mandates. Operators favor liquid-cooled GPU clusters to meet power-usage-effectiveness thresholds and curb operating expenses driven by high electricity tariffs. The scale of these purchases is pulling forward demand that once sat in the second half of the decade, thereby raising near-term shipment forecasts. Collectively, these rollouts anchor the European GPU market on a trajectory in which datacenter accelerators account for a majority of regional revenue before 2028.

EU Chips Act Incentives Boosting Local GPU Manufacturing Investments

The EUR 43 billion (USD 46.4 billion) European Chips Act offers first-of-a-kind facility grants, tax credits, and pilot-line funding to revive continental semiconductor capacity. Although only two sub-5 nm projects have cleared approval, related packaging and heterogeneous-integration lines in Dresden, Grenoble, and Novara are underway. Silicon Box's EUR 3.2 billion (USD 3.5 billion) advanced-packaging plant in Italy and STMicroelectronics' wafer-fab expansions in France signal momentum on supporting infrastructure that discrete GPU vendors rely on for chiplet assembly. Fabless startups such as SiPearl tap these resources to pair European CPUs with imported accelerators, reinforcing a local supply chain that modestly buffers geopolitical risk. While volume output remains years away, the policy framework has already influenced sourcing strategies for hyperscalers planning 2028-2031 deployments.

Supply Chain Disruptions from Geopolitical Tensions on Advanced Nodes

The majority of leading-edge GPU wafers originate from Taiwanese fabs that rely on helium, high-NA EUV scanners, and advanced packaging capacity concentrated at a handful of subcontractors. Helium shortages tied to Gulf-region conflicts curtailed 3 nm wafer starts in late 2024, extending lead times for NVIDIA Blackwell and AMD MI300X shipments to European integrators. Scarcity of high-bandwidth memory further constrains board-level availability, forcing system vendors to pay 30%-50% premiums on the spot market. With no European fab expected to ship sub-5 nm volume before 2028, hyperscalers maintain contingency buffers yet still risk multi-month project delays should another geopolitical event disrupt Taiwanese foundries.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Cloud Gaming and Subscription Platforms

- Electric Vehicle Infotainment and ADAS Compute Demand

- Escalating Energy Costs in Europe Impacting GPU TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete devices captured 65.38% of Europe GPU market share in 2025 and continue to widen the gap as hyperscalers place bulk orders for NVIDIA Blackwell and AMD Instinct accelerators. Europe GPU market size for discrete units is projected to expand at a 17.74% CAGR to 2031, supported by sovereign-compute mandates that prioritize on-premises hardware capable of multi-petaflop training. Blackwell B200 and B300 cards, paired in NVLink racks, let operators shrink model training cycles from weeks to days, directly boosting time-to-market for European large language models. AMD's Instinct MI300X, with 192 GB of HBM3 at 5.2 TB/s, answers memory-bound inference challenges faced by broadcasters and defense agencies. Integrated GPUs remain critical in client PCs and handheld consoles, yet their share of the European GPU market size is projected to decline as compute-intensive workloads outpace their thermal budgets.

Intel's Meteor Lake system-on-chips, though prevalent in laptops, cannot match the architectural headroom of discrete boards that now ship with 600 W-class liquid-cooling loops. Pricing dynamics also favor discrete parts; despite a 10%-15% list-price increase announced for consumer cards, datacenter SKUs enjoy steady allocation priority and premium margins. This shift elevates discrete designs from a traditional graphics accessory to a cornerstone of Europe's digital-sovereignty strategy.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Arm Holdings plc

- Imagination Technologies Limited

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Apple Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Acer Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- Huawei Technologies Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Europe GPU Market

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of AI and ML Workloads in European Datacenters

- 4.2.2 EU Chips Act Incentives Boosting Local GPU Manufacturing Investments

- 4.2.3 Rise of Cloud Gaming and Subscription Platforms

- 4.2.4 Electric Vehicle Infotainment and ADAS Compute Demand

- 4.2.5 Migration to 4K/8K Content Creation Workflows Across Media Sector

- 4.2.6 Open-source GPU Drivers and Ecosystems Lowering TCO for Enterprises

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions from Geopolitical Tensions on Advanced Nodes

- 4.3.2 Escalating Energy Costs in Europe Impacting GPU TCO

- 4.3.3 Regulatory Scrutiny over GPU Power Consumption Standards

- 4.3.4 Talent Shortage in Advanced Semiconductor Design in Europe

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products or Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Geography

- 5.3.1 Europe

- 5.3.1.1 Germany

- 5.3.1.2 United Kingdom

- 5.3.1.3 France

- 5.3.1.4 Italy

- 5.3.1.5 Rest of Europe

- 5.3.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Arm Holdings plc

- 6.4.5 Imagination Technologies Limited

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star International Co. Ltd.

- 6.4.11 Sapphire Technology Limited

- 6.4.12 Palit Microsystems Ltd.

- 6.4.13 Acer Inc.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 Lenovo Group Limited

- 6.4.16 Huawei Technologies Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment