PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064460

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064460

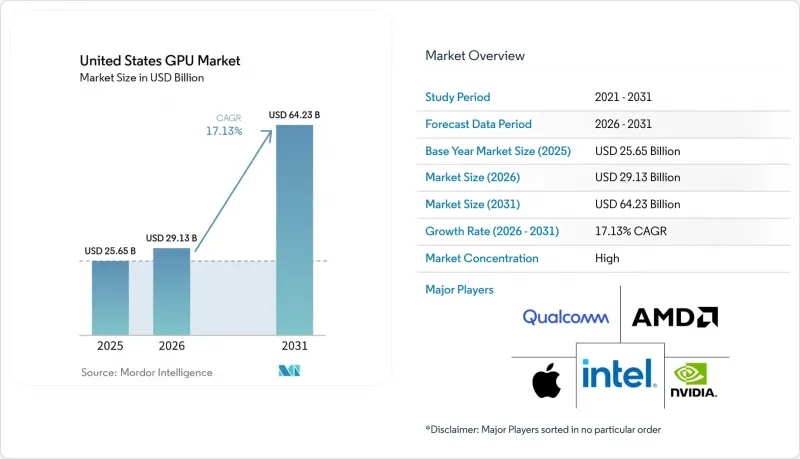

United States GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states gPU market size is projected to expand from USD 25.65 billion in 2025 and USD 29.13 billion in 2026 to USD 64.23 billion by 2031, registering a CAGR of 17.13% between 2026 and 2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

United States GPU Market Trends and Insights

Growth In AI And Data Center Acceleration Adoption

Hyperscale operators deployed more than one million accelerators domestically in 2025, with Microsoft Azure, AWS, and Google Cloud representing nearly four-fifths of shipments. Multi-year supply contracts now replace spot buys, locking in wafer and packaging capacity well before tape-out. Such commitments protect production priority but reduce availability for regional cloud providers and research labs, indirectly propelling the GPU-as-a-Service model. A single state-of-the-art training run can occupy tens of thousands of cards for months, requiring on-site generation or co-location near baseload power to manage 300- to 1,000-megawatt loads.

Expanding Demand For High-Performance Gaming PCs

U.S. shipments of discrete gaming cards climbed to 8.4 million units in Q4 2024, buoyed by ray-tracing titles and AI-driven upscaling that demand dedicated compute. Yet mid-range boards priced from USD 300 to USD 500 grabbed share from USD 1,000-plus flagships, trimming blended average prices. The entry-level market is being eroded by cloud gaming, while eSports enthusiasts still pay premiums for 240 fps hardware.

Supply Chain Constraints Of Advanced Nodes

Advanced packaging lags wafer output by roughly 18 months, restricting shipments even when plenty of 3 nm wafers are available. The supply of high-bandwidth memory is also tight, forcing smaller buyers to accept 40% spot-price premiums or defer projects. Domestic gigafab construction will close the gap only after 2028, so scarcity will keep prices elevated and allocate priority to hyperscalers with long-term contracts.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives For Domestic Semiconductor Manufacturing

- Rising Popularity Of Cloud Gaming Services

- High Power Consumption And Cooling Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete accelerators accounted for 66.29% of the United States GPU market in 2025, reflecting demand for dedicated memory stacks, independent power rails, and aggressive thermal solutions. Premium datacenter boards showcase 700-watt envelopes, 192 GB of HBM3E, and FP8 throughput exceeding 20 petaflops, enabling trillion-parameter model training. The United States GPU market size for discrete products is projected to grow at 17.53% CAGR as hyperscalers scale clusters by the million-accelerator level. Integrated designs hold 33.71% share and target laptop, tablet, and thin-client workloads where 15-watt budgets are paramount. Qualcomm, Apple, and Intel are closing the capability gap, offering 15-30 teraflops in battery-powered devices, which compresses entry-level discrete demand.

Integrated GPUs are capturing mid-tier consumer spend once served by cards below USD 300. Intel's forthcoming Panther Lake platform integrates ray tracing and matrix engines, while Qualcomm's Snapdragon X2 Elite delivers 80 TOPS neural throughput at sub-15-watt draw. Vendors of discrete boards, therefore, concentrate on high-margin datacenter, workstation, and enthusiast segments, where customers value peak performance per node and invest in liquid cooling infrastructure to unlock gains. This strategic pivot supports gross margins above 60% despite flat to declining unit volume in the consumer channel.

List of Companies Covered in this Report:

- Nvidia Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Arm Holdings plc

- Imagination Technologies Limited

- MediaTek Inc.

- Broadcom Inc.

- Matrox Electronic Systems Ltd.

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Graphcore Ltd.

- VIA Technologies, Inc.

- Rockchip Electronics Co., Ltd.

- Allwinner Technology Co., Ltd.

- Zhaoxin Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Demand for High-Performance Gaming PCs

- 4.2.2 Growth in AI and Data Center Acceleration Adoption

- 4.2.3 Rising Popularity of Cloud Gaming Services

- 4.2.4 Increasing Content Creation Workloads Among Prosumers

- 4.2.5 Government Incentives for Domestic Semiconductor Manufacturing

- 4.2.6 Emergence of GPU Virtualization for Enterprise Desktops

- 4.3 Market Restraints

- 4.3.1 Supply Chain Constraints of Advanced Nodes

- 4.3.2 High Power Consumption and Cooling Challenges

- 4.3.3 Market Cannibalization by Integrated GPUs in Mid-Range Segments

- 4.3.4 Rising Scrutiny Over GPU Energy Emissions in Data Centers

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value / Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nvidia Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Apple Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Arm Holdings plc

- 6.4.8 Imagination Technologies Limited

- 6.4.9 MediaTek Inc.

- 6.4.10 Broadcom Inc.

- 6.4.11 Matrox Electronic Systems Ltd.

- 6.4.12 Texas Instruments Incorporated

- 6.4.13 NXP Semiconductors N.V.

- 6.4.14 Renesas Electronics Corporation

- 6.4.15 Graphcore Ltd.

- 6.4.16 VIA Technologies, Inc.

- 6.4.17 Rockchip Electronics Co., Ltd.

- 6.4.18 Allwinner Technology Co., Ltd.

- 6.4.19 Zhaoxin Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment