PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072487

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072487

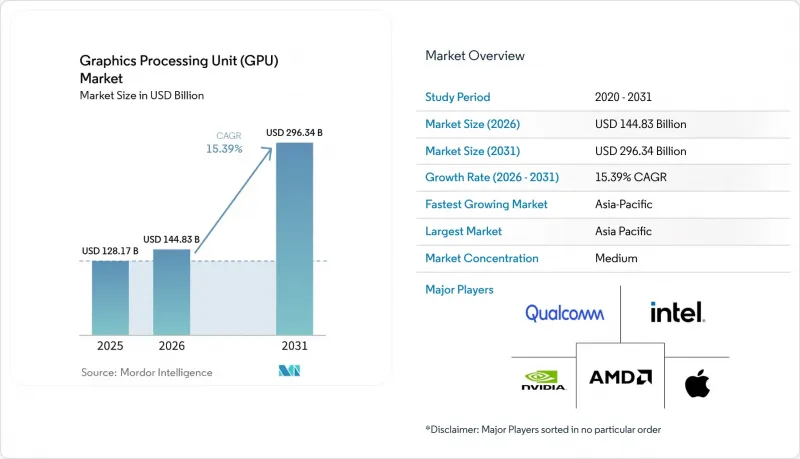

Graphics Processing Unit (GPU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the GPU market size is expected to increase from USD 128.17 billion in 2025 to USD 144.83 billion in 2026 and reach USD 296.34 billion by 2031, growing at a CAGR of 15.39% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and Other Embedded and Edge Devices), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Global Graphics Processing Unit (GPU) Market Trends and Insights

Hyperscale AI Training and Inference Cluster Expansion

The GPU market is being pushed higher by a shift from periodic model training to always-on AI factory operations that keep clusters busy across training, post-training, and inference. Amazon, Google, Meta, and Microsoft confirmed a combined 2026 capital expenditure of USD 725 billion, up from USD 410 billion in 2025, and most of that increase was directed toward AI infrastructure, where GPUs remain the main hardware cost item. Supply-side results pointed to the same pattern as NVIDIA's data center revenue reached USD 75.2 billion in Q1 FY2027, while compute revenue reached USD 60.4 billion, and networking revenue rose to USD 14.8 billion. The GPU market is therefore expanding to meet both compute and networking demand, as larger AI factories require dense interconnect fabrics and accelerators. NVIDIA also said hyperscalers accounted for only half of its data center revenue, indicating that demand had broadened to cloud specialists, enterprise deployments, and sovereign programs. This matters for the GPU market because it reduces dependence on a single buyer group and makes current demand more durable than a narrow hyperscaler cycle.

Enterprise AI Factory and Sovereign Compute Procurement

The GPU market gained another demand stream as national compute programs and enterprise AI factories began treating GPU clusters as strategic infrastructure rather than optional technology capacity. Procurement in the Middle East and Europe added a separate customer layer that sat outside the traditional hyperscaler channel, widening the geographic spread of high-end GPU buying. The EU AI Act and tighter data residency rules in regulated sectors also pushed more compute to remain within national borders, making local accelerator procurement a compliance issue as well as a performance decision. This shifted pricing behavior because sovereign buyers often operated outside hyperscaler volume frameworks and absorbed supply at or above list pricing. The GPU market also became harder for mainstream enterprises to access because allocation queues for top-end accelerators stayed long even as cloud access expanded. As a result, sovereign and regulated enterprises demand that the market's forward visibility be strengthened while also tightening the supply balance for smaller buyers.

Rising ADAS and In-Cabin Compute Content Per Vehicle

The GPU market also has a longer-cycle growth path in vehicles as ADAS perception, sensor fusion, and cockpit rendering move onto centralized compute platforms. NVIDIA's DRIVE Thor platform was positioned at 2,000 TOPS for Level 4 applications, which showed how automotive designs are moving toward much higher compute density per vehicle. Consolidating ADAS and cockpit workloads onto fewer, more capable processors raises semiconductor content per platform and supports sustained GPU demand across model generations. The same shift also favors suppliers with validated automotive-grade software and safety capabilities, because design wins depend on compliance as much as raw performance. Regulations tied to software-defined vehicles and vehicle safety are reinforcing that direction by increasing the need for continuous real-time inference in production fleets. In the GPU market, that means automotive revenue grows more slowly than datacenter revenue, but content growth per vehicle is becoming structurally stronger.

Other drivers and restraints analyzed in the detailed report include:

- Edge AI Upgrade Cycle in PCs and Mobile Devices

- Export Controls and Tariff Volatility

- Elevated GPU and Memory ASPs Slowing Mainstream Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs held 63.84% of the GPU market share in 2025, and this segment is projected to expand at a 15.78% CAGR through 2031. The segment's lead reflected the fit between dedicated memory, high bandwidth, and intensive AI workloads that shared system resources cannot match at the top end. NVIDIA's Blackwell generation raised on-package memory sharply, with the B200 carrying 192 GB of HBM3e versus 80 GB on the H100, underscoring how quickly memory requirements have risen within a single product cycle. NVIDIA also used a dual-die design connected via NV-HBI at 10 TB/s, demonstrating how high-end discrete designs are moving beyond monolithic limits to sustain compute density. The GPU market continued to favor discrete products in training and large-batch inference because those workloads remain constrained by memory bandwidth and local accelerator capacity.

Integrated GPUs improved materially in 2026, which widened their role in client AI systems and lower-cost inference setups. AMD's Ryzen AI 400 Series combined up to 60 TOPS of NPU compute with integrated Radeon 800M Series graphics, and the Ryzen AI Halo platform extended that model with stronger graphics capability and large unified memory pools. That progress made local inference more practical for professional notebooks, developer systems, and workstation-class devices that need lower cost and tighter power envelopes. Even so, the GPU industry still relies on discrete products for frontier training and high-throughput inference because unified memory platforms do not yet match the bandwidth of HBM-based accelerators. The graphics processing unit (GPU) market is therefore likely to continue to see integrated products gain relevance at the edge while discrete products hold the performance frontier and most of the profit pool.

Complete Report Scope:

- By Integration Type

- Integrated GPUs (iGPU)

- Discrete GPUs (dGPU)

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive and ADAS

- Other Embedded and Edge Devices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific

- South America

- Middle East and Africa

- North America

Geography Analysis

Asia-Pacific held 43.16% of global revenue in 2025, and the regional GPU market is projected to expand at a 15.37% CAGR through 2031. The region led because it combined major end demand with critical supply chain positions in memory, packaging, and system manufacturing. China remained central to the GPU market as domestic vendors accelerated commercialization under a stronger local procurement push. Biren and Iluvatar CoreX both reported triple-digit revenue growth in 2025, reflecting the growing support of Chinese demand for local suppliers amid a tighter export environment. South Korea remained vital because Samsung and SK Hynix supply the HBM stacks that underpin leading-edge accelerator performance, while Japan added demand through hyperscale data centers and industrial digital twin adoption.

North America remained the second-largest center of the GPU market because it houses the largest hyperscale buyers and the primary purchasing authority for global AI cluster deployments. Amazon, Google, Meta, and Microsoft together planned USD 725 billion in 2026 capital expenditure, and that spending profile kept the United States at the center of accelerator procurement. North America also shaped the global market through policy, since the US export control framework directly affected which overseas markets advanced GPU vendors could serve. Canada's addition of sovereign compute initiatives widened the region's demand profile beyond private hyperscalers and supported the view that public sector procurement would matter more over time. The region, therefore, influenced both the demand and the supply sides of the GPU market more than any other geography.

Europe's GPU market advanced as compliance, digital sovereignty, and regulated-sector AI adoption pushed local compute investment into a more structured phase. The Middle East and Africa became more important because Gulf sovereign programs started ordering high-end clusters at a scale that exceeded what population size alone would suggest. South America remained earlier in its development cycle, with Brazil serving as the primary base for colocation growth and AI demand in financial services. Across Europe, the Middle East and Africa, and South America, the GPU market expanded more through strategic need and policy alignment than through pure consumer demand, making regional growth patterns more diverse than in earlier cycles.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Arm Holdings plc

- Apple Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- Imagination Technologies Group Limited

- Huawei Technologies Co., Ltd.

- Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- Biren Technology Co., Ltd.

- VeriSilicon Co., Ltd.

- Zhaoxin Semiconductor Co., Ltd.

- VIA Technologies, Inc.

- UNISOC Technologies Co., Ltd.

- Renesas Electronics Corporation

- Rockchip Electronics Co., Ltd.

- Loongson Technology Corporation Limited

- Bolt Graphics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Hyperscale AI Training and Inference Cluster Expansion

- 4.3.2 Enterprise AI Factory and Sovereign Compute Procurement

- 4.3.3 Edge AI Upgrade Cycle in PCs and Mobile Devices

- 4.3.4 Rising ADAS and In-Cabin Compute Content per Vehicle

- 4.3.5 Chiplet-Based GPU Road Maps Improving Yield and Product Scaling

- 4.3.6 GPU-as-a-Service Broadening Access Beyond Hyperscalers

- 4.4 Market Restraints

- 4.4.1 Export Controls and Tariff Volatility

- 4.4.2 Elevated GPU and Memory ASPs Slowing Mainstream Adoption

- 4.4.3 HBM and CoWoS Allocation Bias Toward AI Racks

- 4.4.4 Grid Interconnection Delays for High-Density GPU Campuses

- 4.5 Industry Value Chain Analysis

- 4.6 Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive and ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 India

- 5.3.3.5 Southeast Asia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Arm Holdings plc

- 6.4.6 Apple Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 MediaTek Inc.

- 6.4.9 Imagination Technologies Group Limited

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- 6.4.12 Biren Technology Co., Ltd.

- 6.4.13 VeriSilicon Co., Ltd.

- 6.4.14 Zhaoxin Semiconductor Co., Ltd.

- 6.4.15 VIA Technologies, Inc.

- 6.4.16 UNISOC Technologies Co., Ltd.

- 6.4.17 Renesas Electronics Corporation

- 6.4.18 Rockchip Electronics Co., Ltd.

- 6.4.19 Loongson Technology Corporation Limited

- 6.4.20 Bolt Graphics, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment